Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

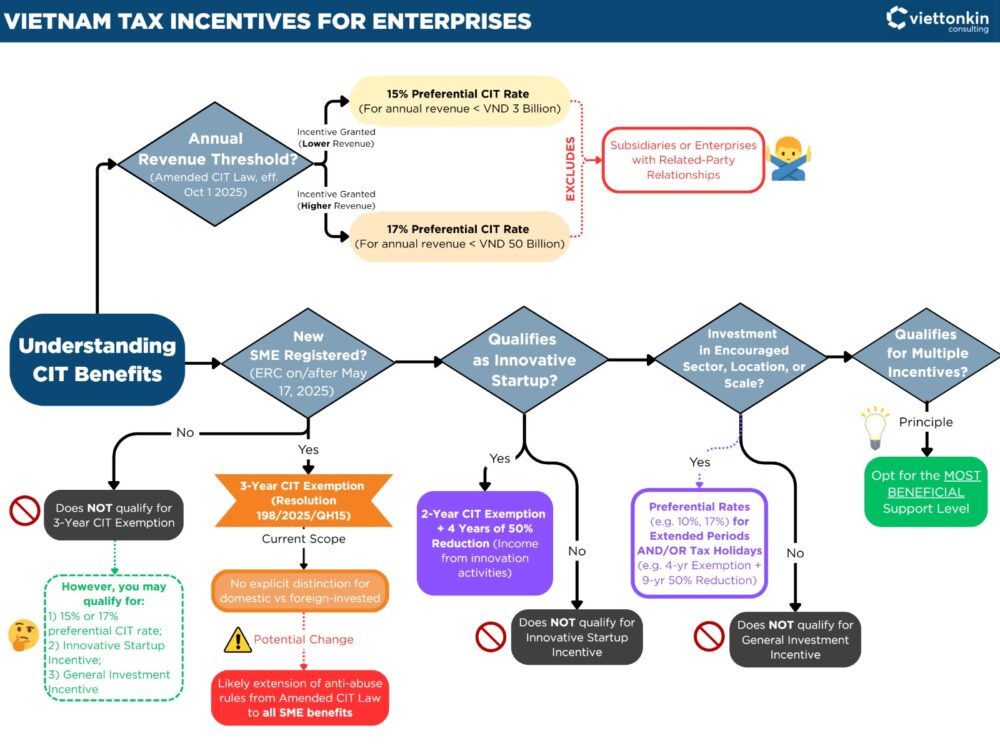

I. Executive Summary: Unlocking Vietnam's 3-Year Corporate Income Tax Exemption for New SMEs

Resolution No. 198/2025/QH15, a landmark legislative act by Vietnam's National Assembly, introduces a significant 3-year Corporate Income Tax (CIT) exemption for newly established Small and Medium-sized Enterprises (SMEs). This pivotal policy is strategically designed to stimulate new business formation and foster robust growth within Vietnam's burgeoning private sector, offering a substantial incentive for both domestic and foreign direct investors eyeing the Vietnamese market.

To qualify for this valuable tax holiday, new enterprises must meet two primary conditions:

Their first Enterprise Registration Certificate (ERC) must be granted on or after May 17, 2025.

They must satisfy the prescribed SME classification criteria as defined by Vietnamese law.

This measure is a direct and impactful component of a broader governmental strategy aimed at bolstering entrepreneurial activity, reducing regulatory burdens, and cultivating a more dynamic and investor-friendly economic landscape in Vietnam. Viettonkin Consulting helps foreign investors navigate these opportunities, ensuring clarity from complex regulations.

II. Vietnam's Private Sector Growth & New SME Support Framework 2025

Context of Resolution No. 198/2025/QH15: Driving Private Sector as Key Economy Driver

On May 17, 2025, the National Assembly of Vietnam officially enacted Resolution No. 198/2025/QH15, a comprehensive legal framework outlining special mechanisms and policies for the advancement of the private sector. This resolution is not an isolated initiative but a concrete and direct implementation of the Politburo's Resolution 68-NQ/TW, which fundamentally redefines the private sector as the primary driver of the national economy. This legislative shift marks a historic departure from previous regulatory approaches, signaling a transition from a restrictive mindset to a proactive, development-oriented strategy aimed at unleashing the private sector's full potential.

Beyond CIT Exemption: Comprehensive SME Support in Vietnam

The 3-year CIT exemption, while substantial, is part of a multi-faceted and comprehensive support system established by Resolution 198/2025/QH15. This broader framework is designed to address various challenges faced by SMEs and to create a more conducive business environment:

Reduced Regulatory Burdens: To alleviate administrative pressure and foster a less intrusive regulatory climate, the resolution limits inspections and audits for business entities to no more than once per year, unless there is clear evidence of legal violations. This measure is intended to curtail regulatory overreach and enhance business autonomy.

Financial and Credit Support: Recognizing the importance of accessible capital, the resolution introduces a 2% annual interest rate subsidy for loans specifically designated for green, circular economy initiatives, or projects adhering to Environmental, Social, and Governance (ESG) standards. This aims to channel investment towards sustainable development.

Land Access Support: To ensure that SMEs, high-tech firms, and innovative startups have adequate physical space for operations, the resolution mandates provincial-level People's Committees to reserve a minimum of 20 hectares or 5% of the total developed land area within industrial parks and cottage industry zones for lease to these entities. Furthermore, these eligible businesses will benefit from at least a 30% reduction in land rental fees for the first five years of their lease contracts.

Support for Research, Development, Innovation, and Digital Transformation: The government encourages innovation by allowing enterprises to allocate up to 20% of their enterprise income taxable income to establish internal funds for science and technology development, innovation, and digital transformation. Additionally, businesses may deduct 200% of their actual research and development (R&D) expenses when calculating corporate income tax. To further support micro and small businesses, the State will provide free digital platforms and shared-use accounting software.

Abolition of Business License Tax: A significant administrative burden is set to be removed with the planned cessation of business license tax collection and payment starting January 1, 2026. This aims to simplify compliance for new and existing businesses.

The extensive nature of the measures outlined in Resolution 198/2025/QH15, encompassing regulatory streamlining, financial assistance, land access, and innovation promotion, indicates that the 3-year CIT exemption is not an isolated policy. This multifaceted approach suggests a foundational element of a comprehensive, strategic overhaul aimed at fostering a more robust, transparent, and competitive business environment for the private sector. This reflects a long-term commitment by the Vietnamese government to reduce systemic barriers and actively nurture entrepreneurial growth, rather than merely providing temporary relief. The emphasis on "removing barriers" and ensuring a business environment that is "open, transparent, clear, consistent, stable in the long term, easy to comply with, and low in cost" reinforces this deeper, systemic intent.

III. Key Eligibility for Vietnam's 3-Year Corporate Income Tax Exemption

The 3-year Corporate Income Tax (CIT) exemption is a significant incentive specifically designed to support newly established Small and Medium-sized Enterprises (SMEs) during their critical startup phase. To qualify for this exemption, enterprises must satisfy two crucial conditions.

Condition 1: First Enterprise Registration Certificate (ERC) Requirements

The primary requirement for the 3-year CIT exemption is that the enterprise must be granted its first Enterprise Registration Certificate (ERC) with an issue date on or after May 17, 2025.

The "Enterprise Registration Certificate" (ERC), often known as a Business Registration Certificate (BRC), is the official document legally authorizing a business to operate in Vietnam, confirming its legal status and functioning as its tax identification number. For Foreign-Invested Enterprises (FIEs), obtaining the ERC is a mandatory step that follows the issuance of the Investment Registration Certificate (IRC).

The explicit wording "first Enterprise Registration Certificate" is a critical aspect, designed as a safeguard against abuse and to ensure the incentive is directed towards truly new market entrants. This implies:

No Re-registration for Existing Entities: An ERC issued due to an amendment or re-registration of an existing entity generally will not be considered a "first" ERC for this exemption.

Mergers & Acquisitions (M&A): A business formed through a merger would typically inherit the rights and obligations of the acquired entity, including existing tax incentives and losses, and would generally not be treated as a "new" entity eligible for this "first ERC" exemption.

Household Business Conversions: While converting household businesses to legal entities is encouraged for broader support, such conversions are also unlikely to qualify for the "first ERC" exemption under the spirit of Resolution 198/2025/QH15, which aims to incentivize genuine new business formation.

This stringent interpretation ensures that the incentive aligns with the broader governmental objective of stimulating fresh economic activity rather than merely allowing existing businesses to restructure for tax relief. For foreign investors setting up new operations in Vietnam, understanding this specific condition is paramount.

Condition 2: Vietnam SME Classification Criteria (Decree 80/2021/NĐ-CP)

The second condition mandates that the enterprise must qualify as a small or medium enterprise (SME) as defined by Article 4 of the Law on Support for Small and Medium-sized Enterprises 2017 (Law No. 04/2017/QH14) and, more specifically, by Article 5 of Decree 80/2021/NĐ-CP.

SME status is determined by specific thresholds related to the average annual number of employees paying social insurance, maximum annual total revenue, or maximum total capital. These thresholds are differentiated by sector (agriculture, forestry, fisheries; industry and construction; trade and services) and by size category (micro, small, medium). It is important to note that these criteria apply uniformly to all enterprises, irrespective of their ownership structure, meaning both domestic and foreign-invested companies can qualify for SME status.

SME Classification Criteria per Article 5 of Decree 80/2021/NĐ-CP

Enterprise Size

Sector

Avg. Number of Employees (Social Insurance)

Maximum Annual Total Revenue (VND)

OR Maximum Total Capital (VND)

Micro

Agriculture, Forestry, Fisheries; Industry and Construction

≤ 10 people

≤ 3 billion

≤ 3 billion

Trade and Services

≤ 10 people

≤ 10 billion

≤ 3 billion

Small

Agriculture, Forestry, Fisheries; Industry and Construction

≤ 100 people

≤ 50 billion

≤ 20 billion

Trade and Services

≤ 50 people

≤ 100 billion

≤ 50 billion

Medium

Agriculture, Forestry, Fisheries; Industry and Construction

≤ 200 people

≤ 200 billion

≤ 100 billion

Trade and Services

≤ 100 people

≤ 300 billion

≤ 100 billion

A notable aspect of this classification system is the self-declaration mechanism. SMEs are required to determine and declare their size (micro, small, or medium) using a prescribed form and submit it to the agencies or organizations providing support for SMEs.Enterprises bear full legal responsibility for the accuracy of their declarations. Should an enterprise discover an inaccuracy in its declared size, it is obligated to modify and re-declare before receiving any support. Intentional untruthful declarations made for the purpose of receiving benefits will result in legal responsibility and the requirement to refund the entire support amount received.

This provision for self-declaration of SME status is a clear governmental effort to streamline the process for accessing incentives, thereby reducing bureaucratic hurdles and empowering businesses to quickly benefit from support. This aligns with the broader governmental agenda of administrative reform and reducing compliance costs. However, the simultaneous imposition of "legal responsibility" for accurate declarations and the threat of requiring refunds for untruthful declarations places a significant onus on enterprises. This indicates a shift in the regulatory burden from extensive pre-approval checks by authorities to rigorous post-audit verification. Consequently, businesses must invest in robust internal accounting and human resource systems to accurately track employee numbers (specifically those contributing to social insurance), revenue, and capital, and to maintain comprehensive supporting documentation. This mechanism, while fostering a more efficient system, demands a higher degree of internal diligence and accountability from enterprises.

IV. Applying for & Complying with Vietnam's SME CIT Exemption

The process for claiming the 3-year CIT exemption for SMEs under Resolution 198/2025/QH15 is designed to be largely automatic, based on the information provided during business registration.

Automatic Application Process for CIT Exemption

The CIT exemption for eligible SMEs is applied automatically based on the business registration data submitted by the company. This means that, unlike some other tax incentives, no separate, formal application specifically for this 3-year exemption is explicitly required.

Importance of Accurate Declaration at Registration

Given the automatic nature of the exemption, the accuracy of the information declared at the time of initial business registration is paramount. Companies are required to declare key data points such as their employee count (specifically those participating in social insurance), projected annual revenue, and charter capital. These figures are subsequently utilized by the business registration authorities and tax authorities to determine the enterprise's eligibility for SME status and, consequently, for the CIT exemption.

Required Documentation for Verification and Potential Audits

While a formal application for the exemption itself is not mandated, businesses are under a strict obligation to retain comprehensive supporting documentation. This includes, but is not limited to, financial statements, detailed payroll records (especially those pertaining to social insurance contributions), and records of total capital. Such documentation is crucial for substantiating the enterprise's SME classification and eligibility in the event of an inspection or audit by tax authorities. Tax authorities explicitly reserve the right to audit this information for verification purposes.

Annual CIT Filing Procedures for Exempt Entities

Even though an enterprise may be exempt from CIT for the first three years, it is still required to comply with annual CIT filing procedures. During the annual CIT finalization process, companies must declare their tax-exempt status based on their SME classification. General CIT filing obligations in Vietnam include preparing financial statements, accurately determining taxable income (even if it is zero due to the exemption), making quarterly provisional CIT payments (if applicable, though the exemption would likely negate this for the exempt period), and submitting the annual finalization return. Adherence to these procedural requirements for reporting income and formally claiming the exemption is essential for maintaining compliance.

The policy of automatic application of the CIT exemption, based on self-declared registration data, represents a strategic move by the Vietnamese government to reduce administrative friction and expedite the process for new businesses to access incentives. This approach marks a clear departure from more cumbersome pre-approval processes that often characterized previous incentive schemes. However, the accompanying emphasis on the enterprise's legal responsibility for accurate declarations and the explicit mention of potential audits, along with the necessity to retain supporting documentation, reveals a fundamental shift in the regulatory enforcement paradigm. Instead of rigorous upfront vetting, the system relies on post-compliance verification. This implies that while initial access to the exemption is straightforward, businesses must maintain impeccable records and be prepared to justify their SME status and eligibility at any time. This effectively transforms the administrative burden from a complex application process to one of ongoing, diligent compliance management.

V. Understanding Exclusions & Overlapping Vietnam Tax Incentives

Understanding the specific scope of the 3-year CIT exemption under Resolution 198/2025/QH15 requires distinguishing it from other tax incentives and recognizing potential limitations.

Distinguishing from Other Vietnam CIT Rates & Anti-Abuse Rules

Resolution 198/2025/QH15 specifically grants a 3-year CIT exemption for newly registered SMEs. This is distinct from other preferential CIT rates introduced by the Amended Law on Corporate Income Tax, which was passed on June 14, 2025, and is scheduled to take effect on October 1, 2025. This amended law introduces preferential rates of 15% and 17% for enterprises with annual revenues not exceeding VND 3 billion and VND 50 billion, respectively.

A crucial distinction lies in the anti-abuse safeguards. The preferential rates (15% and 17%) explicitly exclude subsidiaries or enterprises with related-party relationships to larger entities. This exclusion is a direct anti-abuse safeguard, designed to prevent the artificial fragmentation of businesses solely for the purpose of accessing SME-focused tax relief.

Regarding the 3-year CIT exemption under Resolution 198/2025/QH15, the available information indicates that the resolution "does not distinguish between domestic and foreign-invested businesses when applying the CIT exemption". This statement, when considered in isolation, might suggest that related-party exclusions do not apply to this specific 3-year exemption. However, the subsequent Amended CIT Law, which comes into effect later in 2025, introduces clear anti-abuse provisions by excluding subsidiaries and related parties from other preferential CIT rates. Given the government's stated intent to enhance the "integrity and effectiveness of tax incentives while supporting key developmental sectors" and to prevent "artificial fragmentation", it is highly probable that future implementing regulations will clarify or extend these anti-abuse provisions to encompass all SME-related CIT benefits, including the 3-year exemption. Businesses with complex ownership structures or those involved in related-party transactions should proactively monitor these forthcoming developments and seek professional advice to mitigate potential future compliance risks.

Distinction from Other Tax Incentives

Vietnam's tax incentive landscape is multifaceted, and the 3-year SME exemption should be understood in relation to other available benefits:

Innovative Startups: Innovative startups and organizations supporting innovation are eligible for a distinct incentive package. This includes a 2-year CIT exemption followed by a 50% reduction for the subsequent 4 years, specifically applicable to income derived from innovative startup activities. While an innovative startup may also qualify as an SME, these are separate incentive schemes with different eligibility criteria and durations.

General Investment Incentives: Beyond SME-specific benefits, Vietnam offers various other CIT incentives tied to encouraged sectors (e.g. high-tech industries, renewable energy, software development), encouraged locations (e.g. economically disadvantaged areas, high-tech zones), and project scale. These typically involve preferential tax rates (e.g. 10%, 17%) applied for extended periods, and/or tax holidays (e.g. 4 years of exemption followed by 9 years of 50% reduction). The 3-year SME exemption is a specific, broad-based incentive for new SMEs and should be considered alongside, but distinct from, these other targeted incentives. In instances where an SME qualifies for multiple incentives, the prevailing principle generally allows the enterprise to opt for the most beneficial support level.

VI. Strategic Advice for Foreign Investors: Maximizing Vietnam Tax Incentives

To effectively leverage the 3-year Corporate Income Tax (CIT) exemption under Resolution No. 198/2025/QH15 and navigate Vietnam's evolving tax landscape, businesses should adopt a strategic and proactive approach.

Maximizing Benefits and Ensuring Long-Term Compliance

Accurate Initial Registration: Given that the exemption is automatically applied based on business registration data, it is paramount to ensure that the initial Enterprise Registration Certificate (ERC) accurately reflects the enterprise's SME status in accordance with the detailed criteria outlined in Decree 80/2021/NĐ-CP. Any discrepancies at this stage could jeopardize eligibility.

Robust Record-Keeping: While a formal application for the exemption is not required, businesses must maintain meticulous financial statements, comprehensive payroll records (especially those detailing social insurance contributions), and accurate capital records. These documents are essential for substantiating the SME classification and eligibility in the event of an audit by tax authorities.

Monitoring SME Status: Enterprises should continuously monitor their employee count, revenue, and capital against the SME criteria. Although the initial 3-year exemption is fixed from the registration date, changes in business size in subsequent years could impact eligibility for other ongoing SME support policies.

Understanding Overlapping Incentives: If an enterprise also qualifies as an innovative startup or for other sector-specific or location-based incentives, a careful analysis should be conducted. The principle of allowing the enterprise to choose the "most beneficial" support level means that a strategic decision may be required to maximize overall tax advantages.

Importance of Expert Legal & Financial Consulting in Vietnam

Engaging with experienced legal and tax advisors early in the business setup process is crucial. This ensures full compliance with all conditions for the exemption and allows for strategic positioning of the enterprise to maximize available incentives. This guidance is particularly vital for foreign-invested enterprises navigating the complexities of Vietnamese regulations.

Businesses should develop a comprehensive long-term financial plan that extends beyond the initial 3-year tax break. The exemption provides significant short-term relief, but it is a limited-period incentive, and sustainable growth requires a strategy that accounts for future tax obligations.

Outlook on Future Policy Developments

The Vietnamese tax and business regulatory landscape is dynamic and subject to ongoing adjustments. Businesses should actively monitor the promulgation of detailed implementing regulations, especially concerning the interplay between Resolution 198/2025/QH15 and the recently Amended CIT Law. This is particularly relevant for potential clarifications regarding the application of related-party exclusions to the 3-year exemption. The broader trend indicates a governmental commitment to continuous reforms aimed at improving the business environment and attracting further investment. Staying informed about these developments will be key to long-term compliance and strategic advantage.

VII. Conclusion: Seizing Vietnam's SME Tax Opportunity

Resolution No. 198/2025/QH15 represents a significant and strategic initiative by the Vietnamese government to foster private sector growth through the provision of a 3-year Corporate Income Tax exemption for new Small and Medium-sized Enterprises. This policy, effective for enterprises granted their first Enterprise Registration Certificate on or after May 17, 2025, and meeting specific SME classification criteria, offers substantial financial relief during the critical startup phase.

Successful utilization of this incentive hinges on a clear understanding of the stringent "first Enterprise Registration Certificate" condition, which serves to target genuinely new business formations and prevent abuse through re-registrations or mergers. Equally important is a precise grasp of the detailed SME classification criteria outlined in Decree 80/2021/NĐ-CP, which vary by sector and size. While the exemption is automatically applied based on registration data, the emphasis on self-declaration places a significant responsibility on enterprises to maintain diligent compliance and robust record-keeping for potential post-registration audits.

The resolution underscores Vietnam's commitment to creating a more favorable and supportive ecosystem for new businesses, both domestic and foreign. It is part of a broader, multi-faceted governmental strategy that includes regulatory streamlining, financial support, land access, and innovation promotion. Navigating the intricacies of Vietnamese tax law and ensuring full compliance requires expert insight.

Contact Viettonkin Consulting today for a personalized consultation on how your new enterprise can maximize the 3-year Corporate Income Tax exemption and other strategic investment incentives in Vietnam.

Entering Vietnam's Banking Market: Get Your Essential 2025 eBook

Vietnam's dynamic banking sector is a top destination for foreign investment. To succeed, you need a deep understanding of the local landscape, from new regulations to market entry models.

Our eBook, "ESTABLISHING FOREIGN BANK PRESENCE IN VIETNAM" gives you the crucial insights you need, including:

2024–2025 Sector Overview: Key economic and banking industry analysis.

Step-by-Step Entry Guidance: A deep dive into all primary market entry modes.

The Latest Legal Updates: Critical regulatory changes taking effect in 2025.

Smart Investment Strategies: Insights on M&A, strategic equity, and Fintech.

Download now for the expert knowledge to invest with confidence.

Entering Vietnam's Banking Market: Get Your Essential 2025 eBook

Vietnam's dynamic banking sector is a top destination for foreign investment. To succeed, you need a deep understanding of the local landscape, from new regulations to market entry models.

Our eBook, "ESTABLISHING FOREIGN BANK PRESENCE IN VIETNAM" gives you the crucial insights you need, including:

2024–2025 Sector Overview: Key economic and banking industry analysis.

Step-by-Step Entry Guidance: A deep dive into all primary market entry modes.

The Latest Legal Updates: Critical regulatory changes taking effect in 2025.

Smart Investment Strategies: Insights on M&A, strategic equity, and Fintech.

Download now for the expert knowledge to invest with confidence.

Founded in 2009, Viettonkin Consulting is a multi-disciplinary group of consulting firms headquartered in Hanoi, Vietnam with offices in Ho Chi Minh City, Jakarta, Bangkok, Singapore, and Hong Kong and a strong presence through strategic alliances throughout Southeast Asia. Our firm’s guiding mission is aimed towards facilitating intra-ASEAN investments and connecting investors in Southeast Asia with the rest of the world, thus promoting international business relationships and strengthening inter-nation connections.

English

English