Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Foreign remittances continue to contribute to the socio-economic growth of Vietnam as more investment opportunities present themselves to the overseas Vietnamese community.

Overview

Remittances have been growing rapidly in the past few years to become one of the potential resources for global socio-economic development, especially in the context of high capital demand for economic recovery. The overseas Vietnamese community grew stronger with about 5.3 million people in 2020 in more than 130 countries and territories, with economic, technological, and management potential, so there is a great opportunity for Vietnam to utilize this resource. Along with foreign direct investment (FDI), remittances account for the largest proportion of foreign capital into Vietnam and have tended to increase over the years.

Remittances received in Vietnam during 2000-2019 ($ million, percentage of GDP). Source: WDI

Compared to official development assistance (ODA) and foreign portfolio investment (FPI), remittances to Vietnam are always of great value and have higher stability.

For a long time, the Vietnamese government has provided guidelines and issued policies that are beneficial to and attractive to the overseas Vietnamese community. The effort to attract investments and talents, and increase remittances from the Vietnamese community living abroad began to be concentrated at the turn of the twenty-first century, as Vietnam started its reform process with ground-breaking policies to gradually open up and integrate with the world.

With Decision 170/1999/QD-TTg supplemented by Decision 78/2002/QĐ-TTg, the Government of Vietnam began to issue instructions on the work of encouraging and creating conditions for overseas Vietnamese to transfer foreign currency back to Vietnam on their demand in accordance with the laws of Vietnam and the laws of the countries where they currently reside.

Through other documents, such as Resolution No. 36-NQ/TW (2004), Directive 45/CT-TW (2015), Conclusion 12-KL/TW (2021), and Resolution 169/NQ-CP (2021), more instructions were made by the Government to expand and further facilitate the policy of remittances and investment attraction of overseas Vietnamese.

In accordance with Decision No. 170/1999/QD-TTg approved by the Prime Minister, the Vietnamese government encourages the expatriate community to send remittances through channels like credit institutions recognized by the State, money transfers through international postal financial services providers, or by bringing remittances in person into Vietnam.

Current Situation

Although the Covid-19 epidemic has had a strong impact on overseas Vietnamese for the past few years, the State Bank of Vietnam's (SBV) data shows that in 2021, foreign remittances reached $12.5 billion, an increase of about 10% compared to 2020.

However, the World Bank claimed that due to the numerous other channels through which remittances enter the country, the actual number was actually higher. It was estimated that Vietnam ranked eighth in the world for foreign remittance inflows, bringing in $18.1 billion, up from $17.2 billion in 2020.

Vietnam ranked eighth for foreign remittance inflows in 2021.

According to data from the Ministry of Finance, from 2000 to 2020, remittance inflows into Vietnam accounted for 3-8% of GDP annually, higher than those of developed countries (1-2% of GDP on average).

Most of the remittances came from North America (USA and Canada), Asia, Australia, and Europe. The United States - where many overseas Vietnamese live and work - accounts for 50% of the total remittances to Vietnam, followed by Japan, China, and Australia.

The United States accounted for 50% of the total remittances to Vietnam.

The major economies in the world were predicted to recover and grow in 2022, allowing overseas Vietnamese to earn and send more money back to support family members or invest in business and production. Recently, worrying indications have emerged, proving that the growth in remittances to Vietnam will be a lagging indicator. According to the SBV Ho Chi Minh City Branch, the total amount of remittances transferred to Ho Chi Minh City through credit institutions and economic organizations in the first 6 months of 2022 only reached 3.16 billion USD, down 13% compared to the same period last year. However, this unexpected outcome is seen as a temporary setback resulting from the conflict in Russia and Ukraine and high inflation brought on by high food and oil prices. Remittances to Vietnam are still expected to recover and maintain a growth momentum of 5-7% by the end of 2022.

Remittances for Investment

Previously, remittances transferred to Vietnam were mainly used for personal savings. However, in recent years, the investment of remittances in securities, real estate, business establishments, or investments in production, business, and services has increased sharply.

By the end of 2021, overseas Vietnamese from 29 countries and territories had invested in 376 investment projects in Vietnam, in 42/63 provinces and cities across the country, focusing primarily on the processing and manufacturing industries, with a total capital of approximately $1.72 billion, not including the investment capital of overseas Vietnamese through other indirect forms or by investing in the form of domestic investment. In addition to the direct investment capital flow, there are also connections from overseas Vietnamese, bringing international businesses and corporations to invest and build projects in Vietnam.

Mr. Johnathan Hanh Nguyen, in addition to being known as the chairman and founder of Imex Pan Pacific Group (IPPG), is also an overseas Vietnamese known for his love of and desire to contribute to the development of Vietnam. In addition to the 10 billion USD that US investors committed in writing, there are more than 68 documents and letters exchanged between the IPPG and the US Congress and leaders of the two countries about the establishment of an international financial center to be located in Ho Chi Minh City and a regional financial center to be located in Da Nang.

Investors who are Vietnamese citizens but also have a foreign nationality may choose whether to apply market access conditions and investment procedures applied to domestic investors or foreign investors., according to Decree 31/2021/ND-CP, which details and governs the Law on Investment. Because they are exempt from many rules and binding legal obligations when investing as a domestic investor, overseas Vietnamese have invested in many projects in the nation without having their investments counted as FDI.

Vietnam currently has 6 airlines, but no airline specializes in freight transport. This will soon change with the arrival of IPP Air Cargo, invested by businessman Jonathan Hanh Nguyen and other businesses with 100% Vietnamese capital.

According to a recent report by the Ministry of Transport, IPP Air Cargo was granted the first business registration certificate by the Department of Planning and Investment of Ho Chi Minh City with a charter capital of 300 billion VND. If IPP Air Cargo is granted a flight license in November of this year, its domestic route network will begin in production hubs like Can Tho, Da Nang, Khanh Hoa, the Central Highlands, Hai Phong, and Quang Ninh. Hanoi and Ho Chi Minh City will serve as a hub for transshipment and provide connections to international destinations in Northeast Asia, Southeast Asia, South Asia, and Europe.

Since about 30% of remittances currently go to real estate, many analysts have noted that this large source of capital will be a crucial tool in restoring purchasing power in the real estate market. The current policy of allowing overseas Vietnamese to own and buy houses in Vietnam has also stimulated cash flow in real estate. Not to mention that housing prices in Vietnam remain low in comparison to those in developed countries. As the State Bank's policy places a greater emphasis on capital flows to business and production while restricting credit to potentially risky sectors like securities or real estate, remittances into Vietnam's real estate are likely to continue to rise.

Many overseas Vietnamese investors prefer projects in areas with good traffic connections and that can be managed and monitored remotely. Expensive products, such as beach villas and golf resort villas, remain relatively inexpensive in Vietnam when compared to the countries where many overseas Vietnamese reside.

In 2020, the government revised laws on investment and enterprise, in addition to passing the Law on Public-Private Partnership Investment, to further the goals of this Resolution. The revisions encourage high-quality investments, advanced technology use and development, and environmental protection mechanisms. On June 2, 2022, the Prime Minister issued Decision No. 667/QD-TTg on "Approval of the Strategy for Foreign Investment Cooperation in the 2021 - 2030 period", setting out enhanced goals and solutions for efficient foreign investment cooperation. The strategy calls for shifting foreign investments to high-tech industries and requiring those investments to include environmental protection provisions. In the long term, this could lead to an investment trend from foreign investors in general, and overseas Vietnamese in particular.

Foreign remittances, along with foreign direct investment, will continue to become integral parts of Vietnamese socio-economic growth. As more favorable conditions are created by the Vietnamese government in the future, more opportunities will present themselves for overseas Vietnamese to come back, invest in, and contribute to the development of the country as a whole. Contact Viettonkin for more insights and investment tips.

According to Investopedia, bad debt is a term referring to an amount of money that a creditor deems to be uncollectible and must write off as a result of a default on the part of the debtor. When businesses make use of credit from banks or other lenders, both parties are always aware of the risk that these credit lines become bad debts, despite low probabilities and naturally the best efforts of both parties to avoid such situations from occurring.

However, in such rare occurrences, investors and business managers should have a comprehensive understanding of the local regulations and practices regarding debts to make the best decisions moving forward. Often, when a debt becomes unpayable, businesses opt for either filing for bankruptcy or working with advisors to restructure the debt and revise their cash flow management, in order to improve business operations and feasibility of repayment.

Bad Debts in Vietnam

In Vietnam, according to the regulations of the State Bank of Vietnam (SBV), debts can be classified into 5 groups as follows:

Group 1: Qualified debts;

Group 2: Debts requiring special attention;

Group 3: Sub-standard debts;

Group 4: Doubtful debts; and

Group 5: Potentially irrecoverable debts.

Bad debts, also known as non-performing loans (NPLs), fall into the above-mentioned Groups 3, 4, and 5.

When a business has been confirmed to be in a situation of bad debt, it will be extremely difficult for them to continue borrowing from banks or other credit providers.

Even in the case of successful full repayment of both interest and principal, all information about the borrower, including past loans, current loans, overdue debt periods, the borrower's full name, and the borrower's full address, will continue to be stored and monitored at the Credit Information Center (CIC) for another 03 to 05 years after the final payment is made..

Thus, we strongly advise business owners, especially foreign owners, to avoid getting into bad debts.

Legal Update on Conditions for Offshore Loans

The SBV is working on a draft circular to replace Circular 12/2014/TT-NHNN, which was published in 2014 and regulated the terms for foreign loans applied to businesses that were not government-guaranteed. The new circular would tighten controls on credit institutions' and businesses' foreign borrowing activities, which have been rising quickly in recent years.

3 notable new points about conditions for foreign loans:

A ceiling on foreign borrowing costs;

Performing foreign currency derivative transactions to hedge exchange rate risk;

Requesting the borrower to select a representative organization to manage the collateral, which may be a credit institution, a foreign bank branch, or a legal organization established in Vietnam in the case of a foreign loan with collateral on Vietnamese soil.

In terms of the impact on FDI enterprises, the draft circular is expected to partially solve the problem of "thin capital" of FDI enterprises in Vietnam, which is deeply related to transfer pricing.

In a survey conducted in 2019 by the Ministry of Finance, among 140 businesses examined, all had loans that were more than four times their equity, and all of them were FDI businesses. Mr. Do Thien Anh Tuan (Fulbright University Vietnam) provides an example of a parent company that provides financial services with higher interest rates on the market and allows its subsidiaries and associates to borrow loans. Businesses can use this "trick" to repatriate profits since interest expense is an expense that can be deducted.

According to the draft circular, for short-term foreign loans, the draft stipulates that enterprises are only allowed to take short-term loans to pay debts arising within 12 months from the time of signing the loan agreement, but does not include debts arising from loan contracts with residents, payables arising from buying trading securities, contributing capital to purchase shares, buying investment properties, and receiving project transfers.

The SBV is rumored to have tightened regulations in order to promote economic growth while ensuring that enterprises with strong credit are supported in obtaining the capital they require for both production and operations. Good businesses can still raise capital from credit institutions in their home country or from credit institutions with whom they have a history of mutually beneficial relationships and connections. At the same time, systemic risks from speculative loans and high-risk foreign loans will be avoided thanks to the new regulations.

The regulations also seek to make the domestic financial sector of Vietnam more competitive.

Experience Outstanding Debt Financing Services with Viettonkin

Viettonkin provides a range of cross-border debt financing services, with the goal of assisting and advising our clients in debt restructuring so that their future cash flows and financial situations achieve sustainability. The following is a list of our detailed scope of work

Examine Client's cash flows and financial situation to make suitable recommendations for effective debt restructuring plans.

Prepare a restructuring plan and submit it to the lenders after reviewing internally with Client

Pitching the restructuring plans to lenders, then negotiate and close the deal.

Complete and organize all related documents for all parties to sign.

Advise on solutions to meet and maintain investor/lender requirements following loan disbursement.

Viettonkin is confident that with our team of professional specialists, we will be able to assist our clients in successfully completing all of the above steps. For further information, please fill the Contact Us form here and our team will reach out to you at the earliest.

Vietnam is believed to be the next booming market for BNPL enterprises in the imminent future by many investors. With its tremendous market potential and a young, smart, and tech-savvy generation of consumers who want to take control of their spending, Vietnam BNPL is expected to take a great leap in its development process. However, given the bumpy road ahead, there still remain many doubts around whether investors can truly find their way to success in this lucrative sector considering all the risks involved.

Top 3 reasons why BNPL is blooming in the upcoming time

Market potential

The Vietnamese BNPL market is displaying great potential for enterprises to jump in and take the initiative.

Statistics from the Payment Department of the State Bank of Vietnam (SBV) showed that by the end of the second quarter of 2022, the number of domestic credit cards in circulation in Vietnam was roughly 543,000, equivalent to only 7% of the number of international credit cards and 0.5% of the total number of cards in the whole market.

Mr. Ho Minh Tam - CEO of VietCredit Finance JSC, Kredivo’s strategic partner in Vietnam commented: "BNPL is gradually becoming a popular form of shopping in Southeast Asia. Considering the domestic market size, low credit card ownership rate will open up many opportunities for us when entering this market”.

Besides, Vietnam’s middle class is growing fast, spending more aggressively, and by doing so, contributing to a change in consumer behavior towards the retail and e-commerce ecosystem. Since BNPL is primarily fueled by e-commerce, the rise of this affluent class in society will help foster a more favorable environment for the growth of the BNPL industry.

Not only that, a report conducted by Statista in 2021 indicates that the number of Internet users in Vietnam is estimated at around 72.53 million people, accounting for 77.4% of the population. Such high Internet and mobile accessibility will allow better and easier access for shoppers approaching this type of monetary solution.

Roaring Gen Z population

This payment method is targeted toward those who do not have a credit card as approval for a loan is nearly instant, with a soft check on a consumer’s credit history. Thus, BNPL is particularly popular among millennial and Gen Z consumers.

Arvin Singh - Co-founder of the “Hoola” BNPL service, pointed out that Millennials and Gen Z shoppers - those born between the late 1990s and early 2010s - are strongly receptive to this type of monetary solution since these generations highly value the flexibility in payment and cash flow management.

The thriving of E-commerce

In an interview with Brandsvietnam, Vlad Savin- Head of Business Development of Acclime Vietnam expressed his great expectation towards the country’s BNPL development after seeing its remarkable growth in both the domestic market and the SEA region.

In 2021, the total value of gross merchandise in Vietnam's e-commerce sector was estimated at around 13.7 billion USD, indicating a surge over $5 billion compared to 2020. Therefore, it is not surprising that Vietnam is expected to have an increase in gross merchandise value from $13 billion in 2021 to $39 billion in 2025.

Not only that, there is the remaining 29.3% of the population in Vietnam who has yet to participate in the digital economy. When comparing this figure with other countries in the area such as Thailand with only 10.1%, we can see a huge expansion prospect for Vietnam's e-commerce industry in the coming years. Even the country’s e-commerce market is predicted to surpass Malaysia and Thailand by 2025 (according to a report by Google, Temasek, and Bain & Company).

Forecast of gross merchandise value (GMV) of BNPL services in Vietnam in 2022 and 2028 (in million US dollars)

Given all the potential, BNPL payments in Vietnam are expected to grow by 126% on an annual basis to reach $1.12 billion in 2022. The BNPL payment adoption is expected to grow steadily over the forecast period, recording a compound annual growth rate of 45% during 2022-2028. BNPL's gross merchandise value in the country will increase from $496 million in 2021 to reach over $1 billion by 2028.

Challenges ahead the road

Cybersecurity attacks

Increased e-commerce sales over the last few years have opened new doors for fraudsters looking to exploit burgeoning payment methods.

However, on the condition that organizations are prepared to put in the initial work of accommodating a new payment method in their fraud prevention systems, they can reap big financial gains and contribute to a more flexible consumer landscape. Overall, it all comes down to building a collaborative and proactive anti-fraud approach for BNPL transactions.

Cash is still taking the lead

Despite the rise of BNPL in recent years, cash is still the overall preferred payment method for Vietnamese consumers with 73%; e-wallets take second place at 37%; followed by Domestic ATM cards and credit cards with 27% and 24% respectively.

Most popular payment methods for online shopping in Vietnam in 2021. Source: Statista

In a recent survey conducted by PwC Singapore and the Singapore FinTech Association, when asked about preferred pay-later methods, 51% of survey respondents expressed greater interest in credit card installment plans and upfront payment (39%) over BNPL (24%) for future purchases.

Pay-later methods Vietnamese consumers have used or intend to use. Source: FinTech in ASEAN 2021 Research

When non-BNPL users were asked why they did not use that payment scheme, 25% said they were already satisfied with their credit card. 32% of respondents cited difficulty in keeping track of outstanding bills owed across different BNPL providers as a key point of resistance.

As of now, despite the low ownership rate, credit cards may stay Vietnam’s preferred pay-later method for some time to come. Therefore, it would be a challenge for any BNPL developers to come up with new strategies to compete and carve their names in this competitive industry.

The absence of specific BNPL regulations

Despite the opportunity, BNPL in Vietnam remains slow-moving. This is partly due to the fact that Vietnam does not yet have a clear legal framework regulating the method. Even the sandbox scheme for fintech activities still remains in the legislative pipeline.

What are the risks involved?

Lack of Transparency

Up to this point, the majority of BNPL’s contracts are quite arbitrarily drafted without the appearance of much necessary legal information. Consumers may not know who the real lender is, who they are actually paying to, what grounds to stand on in case they want to make a complaint or take legal action against the providers.

Bad debt & Overspending

Since using BNPL can trigger impulsive purchases in young people, and if they fail to pay the loan in time, it's a high possibility that they have to pay late penalties. That said, these penalties have raised concerns over future repayments being declined by BNPL service providers and thus, pose a negative impact on the safety and stability of the traditional credit market in the long run

Under-developed customer service system

The rapid growth of BNPL business models and the rapid expansion of this market sector may pose additional risks to consumers. One of the most typical problems is the misuse of customer data and the lack of support mechanisms for consumers who are in financial trouble.

How does it affect investors?

The lack of specific regulations could be seen as a good thing as it keeps an open door for investors to enter the market without worrying about legal barriers. However, a set of underdeveloped legitimate regulations might slow down the process of market management and business quality improvement. It now calls for competent authorities to establish a complete and unified legal framework to better protect the benefit of both users and investors, as well as foster a more healthy and sustainable environment for businesses to thrive.

What’s coming next?

Close up to 3 years after Vietnam’s first move into the pay-later industry, it is still in the early stage of development. The thriving e-commerce ecosystem, young population, and low credit card rate are offering countless opportunities for investors to jump in and spice up the game. However, the lack of legal regulations, cyber insecurity, and high COD rate still present themselves as the biggest obstacles that require companies to make constant effort to break through.

The journey to win consumers’ faith is never easy, especially when Vietnam’s BNPL system is not yet fully developed and still has many unsolved problems. Thus, in order to succeed in this fierce competition, BNPL entrepreneurs should consider adopting the strategy of “Think Global, Act Local” and continuously invest in Brand Building to create sustainable development. Keeping deploying extensive promotions to win over customers and gain market share in this era is no longer a good strategy since customer loyalty, organic growth, and consistency are the key factors leading one business to the mount of victory.

Thus, if you’re still looking for a safe set of hands to assist you with your first steps into Vietnam’s BNPL market, connect with Viettonkin for more in-depth, up-to-date, and personal investment advice. Here, we gather a community of reputable consultants, with highly developed communication channels along with a network of diverse connections of domestic and international businesses. Contact us now to enhance your chance of business success!

The buy now, pay later (BNPL) deferred payment method is growing in great popularity among shoppers in Vietnam over the last few years. The growth of the industry across the country has been primarily driven by the rising adoption of BNPL payment options by millennials and Gen Z shoppers.

Moreover, the Covid-19 pandemic has changed consumers' behavior toward payment methods, subsequently reshaping the payment sector in Vietnam. It is expected that the increased market attractiveness is likely to motivate the rise of both domestic and global BNPL players to jump into the Vietnamese BNPL market in the next three to four years.

What is BNPL in Vietnam

What is BNPL?

Buy Now Pay Later (BNPL) is now no longer new to Vietnamese consumers, especially young shoppers who are tech-savvy and financially proactive. This payment solution allows buyers to purchase goods first and pay later in installments that can be divided over several months depending on the product’s value and the buyer’s personal financial situation.

As of now, with millions of users, Klarna, Afterpay, and Affirm are the biggest companies dominating BNPL’s global market as cited in the latest report conducted by Research and Markets. All three work with thousands of retailers and are responsible for millions of transactions yearly. Up until this point, Klarna - the Sweden BNPL company is leading the industry with a reported $53 billion in GMV, roughly 5 times the world’s second biggest American player Afterpay.

Top Buy Now, Pay Later players in the world by region

Despite the rapid emergence of BNPL startups, many people still mistake BNPL for credit service since both types of payment solutions let you pay over time, sometimes even without any interest. However, BNPL doesn't require good credit and has a pre-set payment schedule. Therefore, this payment solution is specifically targeted toward those who do not have a credit card as approval for a loan is nearly instant.

Yet, BNPL is not just about credit, it is about shopping convenience.

Unlike other traditional installment payment schemes that require customers to provide a bewildering array of documentation, BNPL providers offer a much more simple and fast registration option that maximizes the advantages of digital technology.

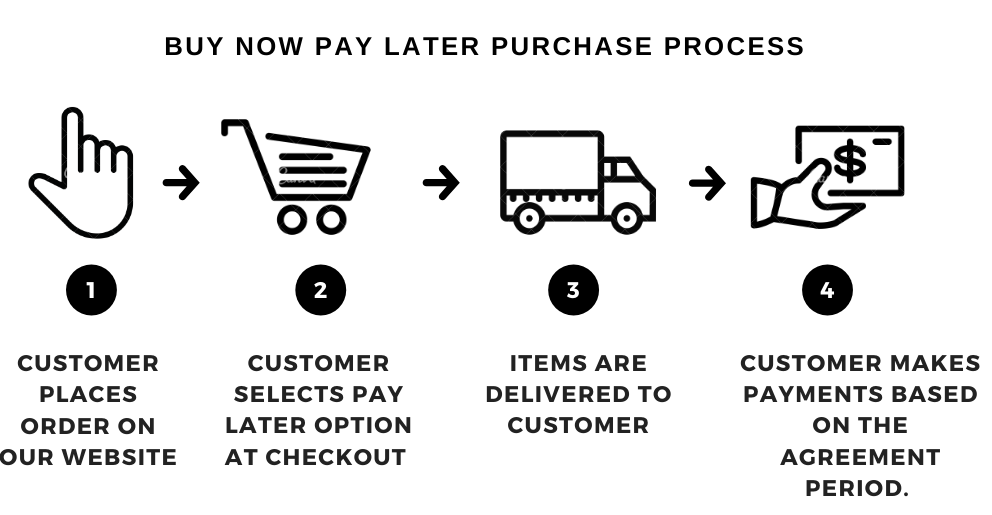

How BNPL works

Breakdown of spending patterns

In Vietnam, motorcycles, smartphones, expensive home appliances, personal care,and other consumer goods account for the majority of BNPL purchases. As BNPL is purely digital and fueled by e-commerce, it’s key for BNPL entrepreneurs to stay up to date with top commodity categories that are leading the market in order to make timely adjustments that fit with consumers’ spending habits.

Most popular shopping categories according to online shoppers in Vietnam in 2021. Source: Statista

A report by Statista released in September 2022 revealed that last year, Vietnam’s most popular online shopping categories were Clothing, footwear, and cosmetics at 69%; followed by home appliances at 64%. Technological and electronic devices accounted for 51%, whereas stationary and gifts were at 50%. Food lands 5th in the list with 44%, 8% lower than the same period of 2020. In the travel sector, ticketing represented 27%, with hotel bookings at 25%. These elevated amounts indicate a very robust eCommerce industry in the country.

In addition to traditional transactions paid in installments such as electronics, education, and motorbikes, many financial companies also open up new schemes for air tickets, travel, cosmetics, and more. This creates opportunities not only to help retailers access modern financial solutions to increase sales but also to give consumers diverse options to balance their spending and personal finances.

The state of development of BNPL in Vietnam

BNPL’s first move into Vietnam’s market

The concept of BNPL has long been popular in the world. Installment plans have been around for years. But why has it become such a bomb lately?

One word: Coronavirus.

The pandemic resulted in many brick-and-mortar retailers being forced to temporarily shut down and saw consumers spend much more of their time at home. Although BNPL plans had already been growing in popularity prior to the pandemic, a shift in consumer spending habits and surging e-commerce adoption during that time really gave the market a significant lift.

According to a report by Worldpay, BNPL accounted for 2.1% - or about $97 billion - of all global e-commerce transactions in 2020. This number is expected to double to 4.2% and rank 5th in the top most popular eCommerce payment methods by 2024.

Back in Vietnam, BNPL first entered the market in early 2019; however, we can only see the thriving of this zero-interest payment since the eruption of the Covid pandemic in late 2019. Covid-19 has dramatically changed consumer behavior, from predominantly offline to online shopping, and thus, made BNPL one of the most appealing monetary solution models to the population.

Mr. Le Tran Bao Duy, CEO of Kaypay said: " Vietnam got into the game quite late when compared to other competitors in the world, but it will go very quickly once it catches up with the trend. Within the next three years, I believe that BNPL will become one of the most popular payment solutions among Vietnamese shoppers."

Which stage are we in right now?

In general, the BNPL market in Vietnam is still in its early stage of development.

Country-wise BNPL penetration. Source: Twimbit

A research conducted by Twimbit in 2021 indicated that even though Vietnam’s total e-commerce revenue amounted to approximately $13.7 billion, BNPL only accounted for 2% of the market share across payment methods, which brought in roughly $260 million in transaction volume last year.

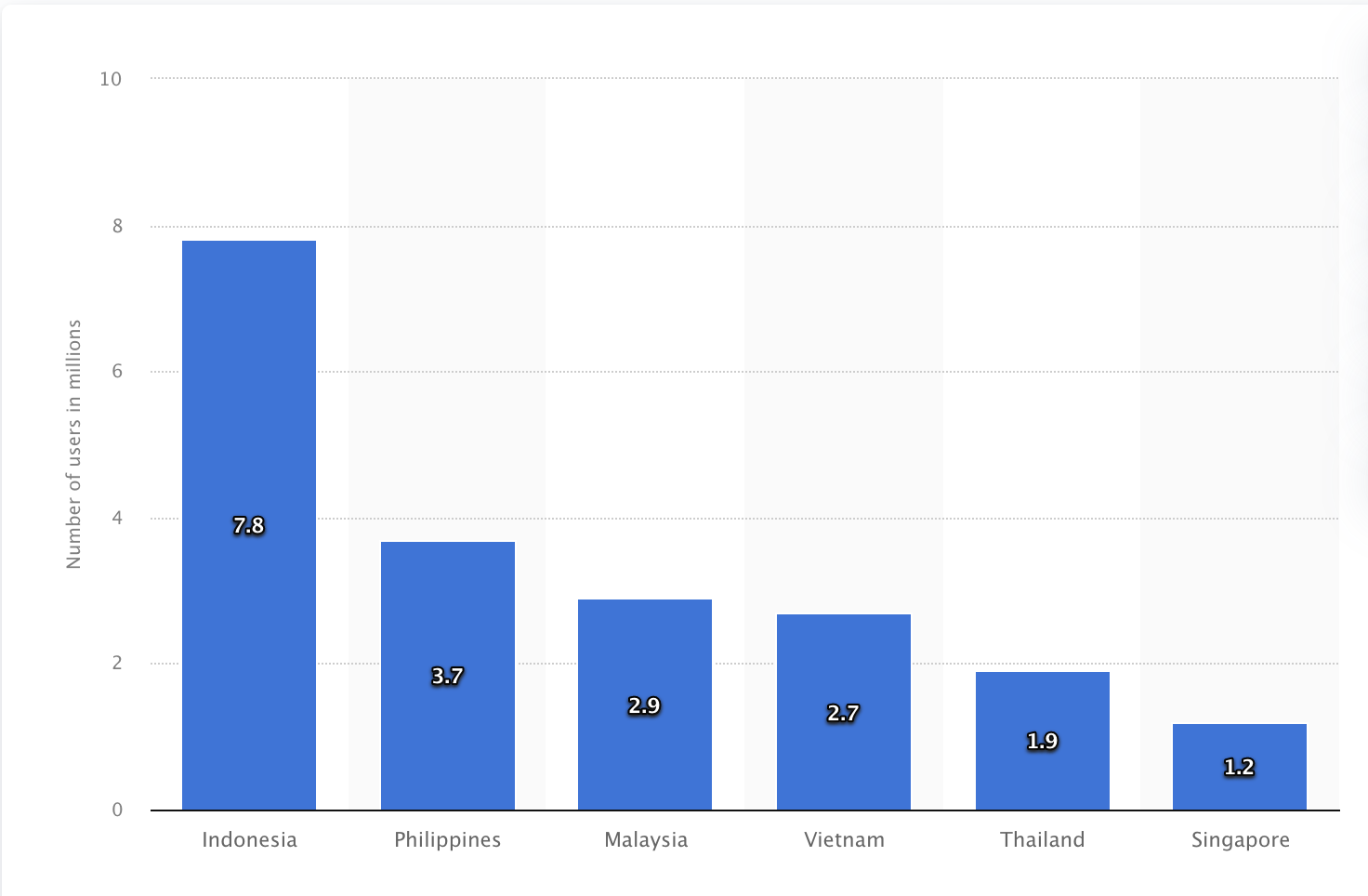

As of 2020, Vietnam has a total population of more than 97 million, out of that number, only approximately 6 million have reported owning personal credit cards and 2.7 million are BNPL users. This number is still quite modest when compared to other countries in SEA, particularly Indonesia and the Philippines with 7.8 million and 3.7 million BNPL users respectively.

Number of BNPL users in Southeast Asia in 2020, selected by country (in millions). Source: Statista.

Given the extreme growth prospects, homegrown BNPL startups are constantly looking to raise funds actively for funding their market expansion strategies and take the first-movers advantage in the market, which is expected to grow significantly over the next few years.

Key players dominating Vietnam’s BNPL market

BNPL products are gaining increasing traction among consumers in Vietnam as both startups as well as established corporations bet big on it. As of now, there’re 2 main types of enterprises that offer BNPL payment solutions to customers: (1) Companies where BNPL is developed as part of the payment option and (2) BNPL startups with BNPL as the core product.

Companies with BNPL as a side product

The majority of BNPL companies of this type are usually built up as a branch or subsidiaries in the whole business system of big finance corporations as well as established banking institutions.

For example, Home Pay Later, Grab Pay Later and Way4 payment services are developed by Home Credit, GRAB Finance Vietnam (GFG), and Lotte Finance Vietnam respectively. These are among the top finance companies that have the most considerable impact on the BNPL market at present.

And to give you a better picture on how they’re doing lately, in July this year, Home Credit signed a strategic cooperation agreement with the Tiki e-commerce platform to launch Home PayLater, a BNPL scheme. Home PayLater – a digital financial product with a VND200 billion ($8.7 million) investment – is set to enhance the convenience of consumers’ online shopping experiences.

Together with finance companies in this category are banking institutions. Up till now, Sacombank is still among the top domestic banking institutions offering the most efficient and trustworthy BNPL service.

BNPL Startups

In Vietnam, many startups and digital payment providers have also jumped on the BNPL bandwagon, such as Ree-Pay, Fundiin, Kredivo, LitNow, Movi, and Atome.

Among the biggest names in the market, Fundiin and Ree-Pay can be listed as the most formidable opponents dominating the game.

To be more specific, in October 2022, Fundiin has raised over $5 million in the Series A funding round co-led by Trihill Capital and Thinkzone Ventures. This round follows the company’s $1.8 million investment in the Seed round led by Japanese funds Genesia Ventures and JAFCO Asia in September last year. Up till present, the company has cooperated with more than 300 partners, having more than 4000 physical stores across Vietnam’s big cities, including top retailers such as Mobile World, Dien May Xanh, Unilever, Galaxy Play, and Reebok.

Another well-worth-mentioning female-led startup in this field calls for the name of CEO Olivia Anh Nguyen with her EasyGop. After 2 years of operation, in early 2022, the company was announced to enter a strategic partnership with the top local Payment Gateway. The collaboration boasts 15M+ users and marks its ambition to extend seamless BNPL services to both Vietnamese offline and online retailers in the upcoming years.

Why now?

It is no surprise that economic drivers that were observed in Europe, Asia Pacific, and North America now find salience in Vietnam. With a growing digital economy, an increasingly affluent consumer population, and low credit card usage, many credit-hungry borrowers may find BNPL as a strong and convenient alternative to satisfy their financial needs.

However, despite these promising developments, BNPL may still present many challenges in Vietnam that entrepreneurs who are about to dive into this potential but risky market should take into serious consideration. For more detailed information on what makes BNPL such a lucrative sector as well as potential obstacles and challenges for investors to watch out for, check out. A promising future holds for newcomers in Vietnam’s BNPL market to gain better insights before jumping into the competition.

In 2021, Vietnam successfully managed the increase in the inflation rate, which drove the economy to grow substantially compared to previous Covid-19 years. This year, as the Covid-19 is not yet under control in various places around the world, along with the escalation tension between Russia-Ukraine conflict, the inflation rate is going to spike. Currently, the high inflation rate in many countries has signaled a gloomy outlook of the globe economy. Vietnam is going to experience a rising inflation rate. This in turn has put great pressure on Vietnam economy.

The positive picture in the economic growth of Vietnam in the beginning months of 2022

In terms of investment, the total investment capital in the first quarter of 2022 increased by 8.9%, in which the investment in state and non-state sectors rose by over 9%. This figure has reflected a healthy and stable macroeconomic performance. Additionally, realized FDI in the first 4 months is expected to reach more than 5.92 billion USD, standing at the highest in the past 5 years. Thus, the increasing number of FDI into Vietnam has confirmed the confidence of foreign investors in this country.

Meanwhile, international trade has shown a promising future. The total export and import turnover in the beginning of this year was secured at 242,19 billion USD, of which 22 products achieved export turnover of over 1 billion USD. The trade balance of goods is estimated to have a trade surplus of 2,53 billion USD.

Potential challenges for Vietnam economy in the beginning of 2022

Under the context of a new normal, the world economy is bouncing back. The demand for raw materials, fuel and materials for manufacturing is burgeoning. Yet, the disruption of the global supply chain caused by Covid-19 has been even exacerbated by the Russia-Ukraine crisis, furthering the inflation rate to escalate in various countries in the world.

In Vietnam, the inflation is still under fine management. The average CPI growth rate in the first 4 months of 2022 was at 2.1% over the same period last year. Similarly, petrol price jumped by 48.84% compared to 2021, while domestic gas price fluctuated according to world petrol price and gas price, averaging 24.6% increase in every 4 months. In contrast, the average price of foodstuffs in the beginning of 2022 decreased by 0.94% as Vietnam is proactive in food supply, fully meeting the consumption demand.

Contrary to the high inflation trend of many major economies in the world, Vietnam successfully controlled inflation in the first quarter of this year. The reason lies in the aggressive directions from the Government. In particular, ministries, branches and localities synchronize price stabilization solutions, thereby limiting negative impacts on socio-economic development.

Source: VectorMine / Shutterstock

In addition, the Government issued supporting policies in a timely manner, significantly reducing pressure on the price level. Notably, VAT reduction from 10% to 8% on some groups of goods and services from February 1, 2022., the reduction of 37 fees and charges in the first 6 months of 2022, or 50% reduction of environmental protection tax on gasoline from April 1, 2022.

The pressure of high rate inflation on Vietnam economy in 2022

Though the inflation is under control, the pressure of a rocketing inflation rate is present in 2022 and 2023. Economic experts have blamed the cost-push phenomenon for placing such pressure on the Vietnam economy in the upcoming time. Further, Mr Nguyen Bich Lam - former director of the General Statistics Office - has also identified 3 major reasons causing strain on inflation.

Supply chain disruption

Firstly, supply chain inflation is the main factor creating the biggest pressure on Vietnam inflation. With large openness, production in Vietnam depends heavily on imported raw materials, costing 37% of total raw materials spending of the whole economy. This figure amounted to 50,98% in the processing and manufacturing industry.

Moreover, the disruption of the global supply chain due to Covid-19 and the Russia-Ukraine conflict, along with the US and Western sanctions against Russia have presented the most obvious and severe risks to many countries. In addition, China is adopting a zero Covid policy, further disrupting the commercial activities between Vietnam and China. As a result, the situation caused a dire shortage in global supply, being the culprit of increasing world goods prices. Therefore, Vietnam will suffer from a perceived inflation in the near future, thereby worsening the economic growth.

Secondly, the Covid-19 pandemic and the Russia-Ukraine conflict has pushed up the prices of gas and oil. In the first four months of 2022, the price of Brent oil increased by about 60% over the same period last year. In March 2022, ING Financial Group forecasted the average price of Brent oil in 2022 at 96 USD/barrel. Bloomberg forecasted 92 USD per barrel in 2022 and 86 USD per barrel in 2023.

For Vietnam, petroleum is a strategic and important commodity, accounting for 3.52% of the total production costs of the entire economy and 1.5% of total household consumption. Therefore, when domestic gasoline prices increase by 10%, inflation will increase by 0.36%. Fluctuations in gasoline prices will have a strong impact on production and consumption prices.

The spiking of aggregate demand due to monetary and fiscal policies

Lastly, aggregate demand spiked in the context of supply chain disruptions. The Vietnamese Government is directing to urgently implement the socio-economic recovery and development program with a scale of 350 trillion VND in the two years 2022 - 2023. In the 350 trillion VND support package, the fiscal policy accounts for 83%, worth 291 trillion VND, while the monetary package only consists of 14%. The remaining 3% belongs to other support packages.

In the monetary package, the government reduced the value-added tax from 10% to 8%, costing 49.4 trillion VND without pumping money into circulation. Additionally, the government did not directly transfer the interest rate compensation package worth 40 trillion VND to businesses, thereby not injecting money into the market. Other packages for job support and Covid-19 support totalling 84.4 trillion VND did not generate money in the market. Therefore, monetary support packages do not put pressure on inflation.

However, the infrastructure development investment package valued at 113,550 billion VND is likely to put strains on inflation. This can be explained by the rising investment causing the increase in demand for raw materials, fuel and construction materials. Especially in the current global context, the disruption in the world supply has caused the prices of commodities to rocket. As a result, disbursing investment capital for infrastructure construction in this situation will create more inflationary pressure on the whole economy.

Besides 3 main factors leading to the pressure on inflation, many economic experts have had a gloomy outlook on the economy. As new forecasts recently updated, the world economy is falling into another “Great Depression” when high inflation, yet economic stagnation both cause stagflation. This presents a not so good scenario for investors to seize an investment opportunity.

The estimation of inflation rate in 2022

2021 is considered to be successful in recovering world economic growth, but inflation in the upcoming time is high.

In a recent statement, the International Monetary Fund (IMF) in Asia-Pacific emphasized that the continent is facing the risk of stagflation. It forecasted a 3.2% inflation in Asia in 2022, much higher than previously estimation, and downgraded Asia's growth projection to 4.9%.

Additionally, the IMF forecasts Vietnam's inflation in 2022 will increase by 3.9%, close to the target threshold of 4% set forth by the Vietnamese Government. On the other hand, Standard Chartered Bank predicts that Vietnam's inflation in 2022 will exceed the target of 4% and may rise to 5.5% in 2023. Meanwhile, Vietnam Investment and Development Bank Securities Company (BSC) estimates if the average oil price in 2022 is at 80 USD/barrel, Vietnam's inflation in 2022 can reach 4.5%; however, if oil prices peak above 100 USD/barrel, inflation could rise to 5.1%.

This rate can be challenging to the economic growth of Vietnam in 2022, directly affecting the investment flow into the country. Yet, the Vietnamese Government is trying its best to maintain and manage the inflation, ensuring the most favorable investment environment for foreign and domestic investors.

Despite challenges, this is still an ideal time for foreign investors to seek investment opportunities in Vietnam. All foreign investors need is to have an expert by their side, helping them with the process of setting up a new business in this dynamic country. Viettonkin is one of the leading consulting firms with deep insights in the Vietnam market and legal system that can assist investors the best. Our strength in professional human resources and well-informed top-notch experts in diverse industries can support you in every step of the way. Let us be your right hand man!

The World Bank describes Vietnam as one of the most dynamic and emerging countries in the entire East Asia region. Thereby, Business Times also identifies that Vietnam completely deserves the title of "the new Asian Tiger".

Currently, Korea, Singapore, Hong Kong and Taiwan (China) are known as the Four Asian Tigers in the economic development. Vietnam is showing the similar signs when looking at the process of turning into the Asian Tigers of these countries.

According to Bloomberg, from 1960 to 1990, the average growth of the Four Asian Tigers is about 6%/year, and a long-term sustainable growth rate is maintained. This sustained growth rate is the basis for each economy to develop into industrialized economies and comprehensively developed regions.

Since 1986, Vietnam's growth has been in the group of countries with the leading growth rate in the world. During the period 1986 - 2019, the average growth rate gains 6.55%/year.

During the period 2020 - 2021, notwithstanding the Covid-19 pandemic, Vietnam’s growth rate is still equal to many countries’ growth around the world is negative. Specifically, in 2020 and 2021, Vietnam's growth will gain 2.9% and 2.58%, respectively.

Not only the outstanding economic growth, but Vietnam is also successful in improving its GDP. According to the World Bank (WB), Vietnam is a successful country in economic reform.

From 2002 to 2021, GDP is ranked 160/195 (USD 547 in 2002), raised up 3.7 times to nearly USD 3,743. Thereby, the poverty rate dropped sharply from more than 32% in 2011 to less than 2.23% in 2021.

Based on Vietnam's post-pandemic economic recovery efforts, Business Times magazine used to affirm that, thanks to the strong recovery rate after the impact of the Covid-19 pandemic and accelerating in 2022, Vietnam fully deserves the title of "new Asian Tiger".

Especially, Business Times said Vietnam gradually becomes the new Asian Tiger thanks to the explosion of the wealthy class. Everything from gilded hotels to luxury apartments to flashy sports cars shows that the rise of the super-rich class in Vietnam has been stronger than ever.

When Vietnam's economy has just been developed, people changed from bicycles to motorbikes. And in recent years, cars have been appearing more on the streets of Vietnam. Vietnam has even started to manufacture their own cars with the VinFast brand, a subsidiary of the country's biggest conglomerate Vingroup.

Vietnam is funding the startup more and more. Vietnam has been known as a Southeast Asian software outsourcing center, where high-skilled workers and high wages are attractive spots for technology companies to use as a platform for development.

Especially, the renewable energy boom is also a factor that helps Vietnam develop on the way to becoming the new Asian Tiger. Vietnam is the country with the highest solar power capacity in Southeast Asia with 16.6 gigawatts in 2020.

Currently, the Government’s incentives are the main motivation for this renewable energy transition, with the FIT tariff playing an important role in promoting the solar industry in Vietnam.

In addition to the growth signs, the Four Asian Tigers also clearly represent the rapid industrialization of economic development. According to Investopedia, import-substituting industrialization was the primary factor leading to the economic success of the Four Asian Tigers.

Industrialization took place after the four economies invested heavily in improving labor productivity. Since then, these economies have contributed to poverty reduction and laid the foundation for rapid industrialization.

Currently, Vietnam has risen up to become one of the countries with a globally competitive industry (CIP) at a relatively high level, belonging to the group of countries with a high average industrial competitiveness. In 2018, Vietnam is ranked at the 44th position in the world according to UNIDO's assessment.

The industry is the sector with the highest growth rate among the national economic sectors. It contributes about 30% of GDP and becomes the national main export industry. In particular, the industry also contributes to bringing Vietnam to the 22nd position as the world's biggest exporting country in 2018.

With the strategic orientation in a few priority industries, key industries, and with the leadership of a few biggest industrial enterprises, they are electronics, textiles, footwear, leather, etc.

According to Investopedia, the Asian Tigers used to form a market with many favorable conditions for exports and mainly free trade. This is referred to as export-oriented industrialization. Thereby, the economy of the Four Asian Tigers has achieved the current outstanding development.

In fact, Vietnam also focused on exports. Specifically, in 2021, Vietnam overcame difficulties and finished spectacularly in the field of import and export, reaching a record number of USD 668.54 billion, raised up 22.6% compared to 2020.

According to the latest report of market research company IHS Markit (UK), in January 2022, Vietnam's manufacturing industry recorded a global sharp increase in output and orders.

Moreover, the world's leading credit rating unit, Fitch Ratings forecasts that Vietnam's export sector will continue to overgrow in the region, thanks to benefiting from cost competitiveness and several major trade agreements.

In March 2021, the Government launched a pilot program to deploy mobile money service in the Vietnam market. They targeted the underprivileged population who live in the countryside, islands, and mountainous areas to aim for an inclusive digital society.

After six months of launching, there have been over 1.1 million mobile money users. This is still a low number given that there are 123 million phone subscriptions in the country. The total number of transactions via mobile money has surpassed 8.5 million, yet their value remains modest at about $16 million. Positive results have been seen; however, mobile money has not gained much popularity as major challenges still remain.

Little spare space for mobile money in the market full of “giant players”

Speaking at a banking conference, Nguyen Manh Hung, Minister of Information and Communication said that Vietnam once had the opportunity to become the leading country adopting mobile money in payment. However, Vietnam didn’t seize that opportunity. Mobile money is the most suitable for the period when digital financial services were still limited, 3G and 4G networks were not ubiquitous, and people only owned a basic phone. Vietnam has been behind the world for 20 years. The golden time for introducing and promoting mobile money has long passed.

These days, according to the State Bank of Vietnam, over 70% of adults in Vietnam have bank accounts. This is the major difficulty to make mobile money popular nationwide. The government opted for remote areas to launch a mobile money pilot. However, alternative financial technologies have also penetrated the rural markets.

QR codes, e-wallet and internet banking have already taken the majority of market share. The number of E-wallets in Vietnam has grown to more than 40 options, compared to only five E-wallets just six years ago. This makes E-wallets one of Vietnamese consumers’ most favorite payment methods for making online transactions. Digital wallet use is 42% among the banked and 17% among the unbanked. Therefore, it is hard to provide a lucrative landscape for mobile money to flourish.

Since the beginning of the pilot program, telecom providers have had major difficulties in identifying customer information. The information they had was collected a long time ago and they have not been able to access the national population database for identity verification purposes. As a result, according to Ms Pham Minh Tu, Deputy Director of Mobifone Digital Services Center, three leading telecom providers missed 50% of their target customers due to the misinformation of customers’ identification.

In order to collect the latest information, mobile money requires people to subscribe to a new version of state-issued ID cards. However, many citizens in remote areas still use the old ones. They also face the inconvenience of going in-store to update details because online updating is still unavailable.

Therefore, a great effort should be put into developing a customer identification database based on the national population statistics in order to mitigate the potential risks regarding information security.

Lack of strategic cooperations

The Vietnam Government is aiming for a national digital ecosystem which mobile money is a crucial member of. To achieve that goal, it is such a long journey to go. There has been no collaboration among telecom providers. This makes users unable to transfer money to another account of a different telecom provider from their own.

An obstacle to mobile money’s nationwide adoption is how it is not linked to a bank account just like e-wallets despite performing similar functions. This presents inconvenience to those who are used to making payments via bank accounts, then consequently leads to users’ dissatisfaction.

In fact, there has been little priority given to the collaboration among telecom providers particularly and between telecom providers and banks generally. Telecom providers consider mobile money as a value-added service, similar to creating a mobile internet site, and want it to seamlessly integrate with their existing operations. Meanwhile, banks assume it is simply another type of mobile banking service, intimately related to their core business and easily fit into their current infrastructure. As a result, they have made little progress to form a strategic cooperation, which can increase users’ convenience and satisfaction, and gain benefits for both businesses.

Low transaction limit

The monthly limit for transactions via mobile money account is 10 million VND (US$438) per user. VNPT Deputy Director Nguyen Son Hai stressed that this transaction limit “did not provide enough elbow room for bills and daily expenses.” Meanwhile, in 2019, instead of a daily transaction limit, Vietnam's central bank set up a monthly limit of 100 million VND (US$4284) for e-wallet users.

There are differences between expenses of urban and rural populations. However, as consumers’ demand is growing rapidly even in remote areas, the transaction limit of 10 million VND seems relatively unappealing to a large number of users.

Insufficient effort into educating target customers about mobile money

Though populations in remote areas are the most potential ones to adopt mobile money, they are still mainly cash-based communities. This makes it hard for the Government and telecom providers to change their belief and behavior, then nourish trust in them.

Lack of information is a real challenge facing the users of mobile money, especially the rural communities. Most of the rural populations lack the information that mobile phone money can be used as well to buy goods through the use of till numbers and payment of utility bills as long as there is a business number. This shows a clear indication that inadequate information posed a challenge to embracing the wide range of services their mobile phone money technology could offer to them.

A large number of target customers, especially the mountainous communities, are utterly unfamiliar with the concept of cashless payment let alone mobile money. Therefore, mobile money also requires significant marketing effort to educate its target customers on what mobile money is and how it can help them better than cash. Launching mobile money must be an expensive business.

The Government has discussed a strategic plan and taken immediate action to address these above challenges. Popularizing mobile money nationwide is not a “mission impossible” because they view challenges as opportunities for innovation and further development. There is a promising future for mobile money to compete in Vietnam's competitive market.

In the early 2000s, the evolution of digital technology alongside the development of computers and the Internet have put forward challenges for traditional credit institutions. As digital transformation has emerged as a global movement, credit institutions and fintech companies have become pioneers in these digital trends. However, due to the Global Financial Crisis, these adoptions have ceased until recently.

COVID-19 pandemic has forced a rapid shift of customer transactions and interactions to digital. In 2021 H1, 134.8M banking customers in APAC were willing to switch to neo-banks or new digital challengers, jumping by 113.2% from the previous year. APAC banks rushed to meet an average of at least 50% growth in digital transactions. Specifically, 44% of the top 250 banks across APAC will complete their “connected core” transformation — working on platform-based and componentized modernization, and API-enablement.

Following the survey by Cloud banking platform Mambu and The Financial Times Focus (FT Focus), 67% of banks believe that they will lose their market share without digital transformation in the next 2 years. In addition, another report by FT Focus surveyed more than 500 global banking executives to investigate their perspectives on the banking industry in the present and future context in depth. The results show digitalization of financial services to be of the essence, with 58% of banking executives predicting the disappearance of the traditional banking models in 5 to 10 years. The report also indicates the Asia-Pacific region had the slowest pace of digital transformation compared to other parts of the world. Notwithstanding, banks in this region are gradually catching up with the world, with an increasing number of investment projects in big data, machine learning and blockchain.

Personal Financial Services Survey in 2021 defines digital banking as the use of online or mobile channels to conduct banking operations. The survey also revealed that while the adoption of digital banking in developed markets such as Australia, Hong Kong and Singapore has stabilized at around 90% since 2017, emerging market, namely mainland China, Indonesia, Malaysia, the Philippines and Vietnam, have seen a rising penetration over the past few years, with an increase from just 55% in 2017 to 88% in 2021

Source: McKinsey

Also, in the Asia-Pacific PFS Survey from McKinsey, more than 80% of the respondents claimed that they would continue to use or will use more online banking services. In the emerging region including the Vietnam market, only 17% of participants will switch to using services from digital banks to traditional banks.

Customers in the APAC region quickly adapt to the change and easily adopt new methods of financial services. In this way, to survive and develop, banks have no choice but to implement digital transformation

Of 249 digital banks worldwide, APAC is home to about 50 digital banks (approximately 20% of the total digital banks in the world), of which more than 70% were established during the years from 2016 to 2020.

ASEAN - potential market

Southeast Asia and India are now emerging as these leaders’ next expansion markets in APAC. In Southeast Asia, Malaysia, the Philippines, Indonesia, Vietnam, and Thailand are showing encouraging signs for digital banks, including positive market liberalization and attractive market demographics. However, most digital banks in South-East Asia have only recently started or are about to commence operations (Fitch Ratings, 2021). The reason is that Southeast Asian users are still mostly concerned about trust and privacy issues when adopting digital services, hindering the digital transformation process in Southeast Asia banks.

However, the adoption rate of digital services has recently increased remarkably. As 40 million new internet users came online in 2021, ASEAN now has a total of 440M users, increasing by 10% in 2020, bringing the Internet penetration rate in ASEAN to 75%. Smartphone penetration has also been central to digital growth, with more than 90% of the region’s 400+ million internet users connecting via mobile phones. Besides, expanding 4G penetration, alongside emerging 5G opportunities, unlocks further potential for connected digital banking customers.

With the advantage of a digitally-savvy population, and despite high banking penetration, there is still room for significant growth in Malaysia’s digital banking, particularly in the area of underserved individuals and SMEs. Moreover, Malaysia recently opened up applications for digital banking licenses. Additionally, being Southeast Asia’s most populous nation where half the population is aged 30 or younger, Indonesia offers a huge market opportunity. With a growing appetite for digital financial services solutions, as well as supporting regulations for digital-only banks being under revision, this country ranks the second-highest e-payment penetration in Southeast Asia, next to Singapore. Similarly, the Philippines has encouraging demographics around the potential for digital banking adoption, including a young and digitally-engaged population. So far, the central bank has awarded three digital banking licenses to Tonik Digital Bank, UNObank, and state-backed Overseas Filipino Bank.

Meanwhile, Vietnam has one of the fastest-growing economies and a rapidly expanding banking sector. More than 40% of the population is now banked and bank cards are seeing accelerating penetration as well. Although many banks are digitizing, no clear dominant winner in the digital banking space has emerged yet. On the other hand, Thailand offers a steady and more mature economy, with relatively high banking penetration. It’s also one of Southeast Asia’s most receptive markets to digital challenger banks.

In Vietnam

The current situation in implementing digital banking in Vietnam

Theoretically, digital banking can be divided into 4 stages: the first stage focuses on multi-channel banks providing various services such as internet banking or mobile banking; the second stage is the multiplexing period, integrating all services into one application, which creates convenience for the users; the third stage is when customers can use all financial services without the existence of a physical bank, and the last stage emphasizes banks improving user experience and personalization. Currently, the process of digital transformation in Vietnamese banks is in the early stages with the most active field in electronic payment and e-wallet. This appealing piece has seduced commercial banks as well as big technology companies to gradually penetrate the market. Up to now, a number of banks have developed electronic payment systems. Typically, Bank Plus e-wallet with a collaboration between Viettel and MBBank, and VPBank with Timo (later sold to Vietcapital Bank), and Maritime Bank with MEED, LienVietPostbank with Vi Viet. In December 2018, Sacombank launched Sacombank Pay which is fully integrated with modern banking features and utilities.

According to the survey results of the State Bank (SBV), as of the first quarter of 2021, about 95% of banks have been developing strategies and implementing digital transformation; Of which, 88% plan to digitize all products and services from customer communication channels to internal business administration. Most banks have applied new technical solutions and technologies in operation and service provision, of which 9 out of 19 operations have been completely digitized by some banks.

As core banking services (payment, credit, savings), and payment on mobile devices experienced a dramatically annual growth with 90% in quantity and 150% in value, and many banks had over 90% of transactions on digital channels, Vietnamese banks are considered to have the largest digital banking adoption rate in the region (McKinsey). Furthermore, Vietnamese users are considered to have the highest acceptance rate of digital banking and digital payments in the region, reaching 82% in 2021, two times higher than in 2017 (McKinsey). This increase is largely due to GenZ and Millennials - a potential customer segment for digital banks and challengers. According to a Morgan Stanley review, 80% of Gen Z use digital banking on smartphones. Thus, Gen Z will become the next big potential customer between the ages of 25 and 40, considered the established generation for the future development of digital banking.

The SBV forecast Vietnam digital banks will have at least a 10% revenue growth, and 58.1% of credit institutions are expected to attract more than 60% of customers in digital transaction channels with an expectation of customer growth rate to reach over 50% in the next 3-5 years.

“BCG assesses digital banking as a promising market in Southeast Asia, especially in Vietnam as the revenue of Vietnam's banking industry can reach $27 billion by 2024, equivalent to a growth rate of 13% per year from 2019, which is the highest growth in Southeast Asia.

Mr. Nirukt Sapru - Global Advisor of Timo Digital Bank considered Vietnam as a potential foreign direct investment (FDI) market for the digital banking sector and highly commented on the potential growth of this sector in Vietnam.

On the other hand, Economist Le Xuan Nghia had a critical viewpoint on the speed of digital banking development in Vietnam as Vietnamese banks are still struggling at the starting point of the digital transformation race while major banks worldwide have developed advanced applications of reading the customer’s mind through their eyes.”

Additionally, Vietnam ranks second in the world with 69% of people not having access to financial services and no bank accounts (Merchant Machine, 2021). According to Viettonkin's assessment, with a combination of supporting policies with the improvement of the recent legal framework and the construction of digital infrastructure by the government, the potential of the digital banking market in Vietnam is still very large.

Policies and Legal framework for developing digital banking

Supporting policies

Mobile money services allow users to make payments when purchasing and selling goods and services without cash or bank accounts. However, the transaction limit does not exceed 10 million VND/month/mobile money account for total transactions: withdrawal, money transfer, and payment. With the implementation and development of mobile money through Decision 316/QD-TTg in 2021, users in rural, remote, and isolated areas will have access to financial services, hence promoting cashless payments. On the other hand, banks, fintech companies, and mobile network operators can collaborate to offer services, and exploit the networks of VNPT, MobiFone, Viettel as well as a customer base of 130 million mobile accounts.

Furthermore, on November 15, 2021, the Prime Minister issued Decision 1911/QD-TTg 2021 on connection and sharing between the National Population Database (NPD) and other national databases as well as specialized databases. Although the Decision stipulates that only state agencies are allowed to access and share NPD, it initially shows that Vietnam is converging to population data. In the future, it is possible to build a mechanism of information sharing from this database with a number of service industries such as banking, insurance, telecommunications, etc.

This Decision will build a unified national database system on personal identification towards open sharing and connection with service industries such as banking, telecommunications, insurance to help verify customers’ information and identity with ease and certainty. As a result, it will reduce the effort and costs for all subjects in society, promote digital transformation in the economy, and allow fast, safe, convenient, and low-cost digital service to a large number of people and businesses. Following this Decision, on the afternoon of June 20, 2021, the first 4 commercial banks together with the Ministry of Public Security signed an agreement to exploit citizen identification data. When there is a reference source from the national population database, the bank can provide almost comprehensive products to customers on the digital banking channel without limits stipulated in Circular 16/2020. /TT-NHNN

Moreover, in May 2021, the Governor of the State Bank of Vietnam issued Decision 810 on the Digital Transformation Plan of the Banking Sector to 2025, with a vision to 2030. ALSO, OTHER DOCUMENTS RELATED TO THE DIGITAL TRANSFORMATION OF THE BANKING INDUSTRY. The decision has designed strategies for the banking industry development in both the short and long term, which are built based on the current situation and issues of this industry in the context of Industry 4.0.

Focusing on developing a modern, advanced State Bank with a reasonable organizational model,

Promoting the role of operating, orienting, and managing the operation of the entire banking system,

Ensuring the banking industry operates synchronously, effectively, and efficiently in alignment with the market mechanism, and adapts to the technological advances of Industry 4.0.

The policy creates a legal framework for credit institutions to accelerate digital transformation, and establish a comprehensive digital banking ecosystem with the goal of developing digital banking models and increasing utility and customer experience

In addition, the State Bank also allows the opening of personal payment accounts in electronic methods (eKYC) according to Circular 16/2020/TT-NHNN, thus encouraging users to change their habits from physical transactions to online transactions in order to lead a cashless society. Under the viewpoints of the banks, eKYC application is also economical in investment in facilities and human resources compared to traditional paperwork, promoting the digital transformation of the banking industry.

Policies for legal framework improvement

Although there is a document on the national database, so far there are no specific regulations on the methods of the exploitation of the national database for credit institutions. This leads to the wastefulness of social resources as each credit institution builds a separate database system, not accessing and making use of the national databases, thus lacking transparency, and failing to promptly detect fraud through the banking system. Therefore, it is suggested that the Government should have documents of permissions for organizations namely banks, insurance. Along with this, SBV should request the Ministry of Public Security, the Ministry of Planning and Investment to allow credit institutions in exploiting and using national databases through a directly connected portal. At the same time, the SBV should propose supplementary regulations on Credit Institutions provision and sharing of national data on citizens, businesses and land, finance, property, taxes, etc to contribute to transparency and a healthy economy.

Even though eKYC is implemented and banks can now use identification measures such as taking a photo of an ID card on both sides, recording a person's face online, in Vietnam, there remains ID card counterfeiting. Accordingly, when implementing eKYC, banks have to access the national database of the Ministry of Public Security to ensure accurate information or exploit information that has already been identified by a 3rd party. Similarly, Viettonkin recommended that a mechanism should be developed to allow banks to identify customers based on the verified information of 3rd parties with equivalent standards, or the national database, and organizational databases.

Besides, Vietnam lacks legal testing mechanisms (sandboxes) to support the implementation of new technologies and new business models. Simultaneously, allowing banks in the digital transformation process to have certain exceptions in meeting safety and efficiency criteria as prescribed by the State Bank will help banks boldly research and test new things. As a result, the Vietnamese government should issue a DRAFT on Decree on Sandbox Regulatory for Fintech in the banking sector.

The impediment of digital transformation in banking is security infrastructure as data security is weak. Regarding the protection of data users, the enforcement of regulations is challenged despite the Law on Cyber Information Security devoting a whole section to regulating the protection of personal information on the internet. Consequently, the Vietnamese government should build regulations on user data protection, digital identity, and an eKYC alliance, along with completing regulations on transaction security, information security, and detailed regulations on electronic signatures, electronic certificates, and electronic transactions in accordance with international practices. Additionally, the Ministry of Public Security is submitting to the Government a proposal to develop a separate Decree on the protection of personal data. This Decree is expected to be a comprehensive legal framework on the protection of personal data in the current online environment.

Likewise, there is no unification in the definition of digital assets, and the definition of evidence in electronic contracts in the field of digital assets, or the definition of electronic transactions, digital transactions, and what is the integrity and originality of digital evidence. For this reason, when there is a dispute or an administrative or criminal violation, banks have to face many problems. Therefore, there should be a document to expand the understanding of Property which includes digital assets in the Civil Code.

When it comes to Intellectual Property Law, the concept of business secrets is still very general and abstract. This leads to controversies over whether data should be considered a trade secret and what protection mechanism should be in place. In fact, there has been a situation of data theft, but state agencies are still hesitant to consider data as a type of intellectual property that needs to be protected. However, the Intellectual Property Law is in the process of reviewing and amending and the recognition and protection of intellectual property in the digital economy need to be focused on. The Government should also

Amend the Law on Electronic Transactions in the direction of adding new contents of the digital economy in line with the development requirements of the field;

Formulate the Government's Decree on the management of the platform economy and business on the Internet;

Finalize and promulgate the Decree on electronic identification and authentication;

Finalize and submit for approval the Decree on personal data protection;

Promulgate legal documents on codes of conduct in the digital environment as well as regulations to create trust and assess credit in cyberspace.

Policies on the construction of digital infrastructure

The Strategy for Development of Vietnam's Banking Industry to 2025, Orientation to 2030, and the Strategy for IT Development of Vietnam's Banking Industry have identified technology as the leading solution for the development of the banking system, in which the objectives are to focus on developing banking products and services based on modern information technology; IT infrastructure development, safety, and security. Those strategies help to change public awareness, considering technology infrastructure as the key in digital transformation

The Strategy for Development of Vietnam's Banking Industry to 2025, Orientation to 2030, and the Strategy for IT Development of Vietnam's Banking Industry have identified technology as the leading solution for the development of the banking system, in which the objectives are to focus on developing banking products and services based on modern information technology; IT infrastructure development, safety, and security. Those strategies help to change public awareness, considering technology infrastructure as the key in digital transformation

In accordance with the strategies, the Payment Department's Branch Committee directs to prioritize the following specific tasks:

focus on building and developing technology infrastructure in the direction of being synchronous, centralized, unified, capable of integrating and connecting with other industries and fields to provide banking products and services on digital platforms, and improve service quality, convenience features, and experience for customers.

continue to build and perfect the technology infrastructure for the supply of digital products by upgrading and completing the Inter-bank Electronic Payment System, the Automatic Clearing House to serve the customers in retail transactions (ACH) with a 24/7 operation,

process payments instantly (real-time), and enhance integration, connectivity with other industries and fields.

at the same time, strengthen security and confidentiality in the provision of banking services.

Convert magnetic card to chip card.