Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

The global geopolitical panorama has never been more uncertain. Political upheaval, social unrest, and economic instability can spell disaster for the unwary business that isn’t prepared for what lies ahead. This is no time to find your way in the dark. If you’re operating in one of the world’s most volatile regions, you owe it to yourself and your people to be informed. Not the garden variety of information that offers a general view of political events, but a condensed and in-depth analysis based on a unique understanding of the regions you’re working in, and your place in it.

What is Geopolitical & Policy Risk?

When considering investment opportunities in emerging or volatile foreign markets, whether through acquisition, merger, or organic expansion, it is crucial for investors to be aware of the potential impact that geopolitical events may have on their business operations.

Source: Internet. Geopolitical and Investment Risks

In general, geopolitical risk is defined as a wide array of risks associated with any sort of conflict or tension between countries that affect the normal and peaceful course of international relations. It typically arises at the intersection of geographical factors, policy decisions (e.g. restrictions on FDI, tolerance of corrupt elites), local cultural climates and has a clear impact on global trade, security, and political relations.

Geopolitical risks are always present in all economies and markets, and could always potentially disrupt economic narratives and reshape market expectations without prior notice. Their impact can be pernicious, filtering through the economy in erratic ways.

For those reasons, acquiring a thorough understanding of overseas markets with the help of geopolitical and policy risk analysis plays a pivotal role in the success of any investment deal.

Why is Studying Geopolitical Risks Important?

Investors study geopolitical risk because it has a tangible impact on investment outcomes.

On a macroeconomic level, these risks impact capital markets conditions, including economic growth, interest rates, and market volatility. Changes in capital markets conditions can, in turn, have an important influence on asset allocation decisions, including an investor’s choice of geographic exposure.

On a portfolio level, geopolitical risk can influence the appropriateness of an investment security or strategy for an investor’s goals, risk tolerance, and time horizon. A higher likelihood of geopolitical risk can raise or lower an asset class’s expected return or impact a sector or company’s operating environment, affecting its attractiveness for an investment strategy.

Geopolitical Risks’ Impact on Corporate Innovation

How Geopolitical Risks Derail Innovations

Geopolitical risk does not just affect security, global trade, and political relations, it also hampers private sector innovation.

Research published in Harvard Business Review by a trio of researchers from the United States and Australia has shown that in years with higher GPR, a smaller proportion of companies’ products were in the early stages of development, suggesting that geopolitical risk leads companies to launch fewer new, innovative product development projects. In other words, companies became more risk-averse and less likely to pursue multidisciplinary, highly impactful innovation.

Geopolitical risk has a greater impact on companies with larger exposure to foreign markets

In the same analysis published in Harvard Business Review, researchers looked at two metrics to measure the impacts of geopolitical risks on companies with more foreign customers, which are: the proportion of a company’s major customers that were foreign (versus domestic), and the proportion of a company’s revenue that came from those foreign customers.

Researchers found that with 1% increase in the foreign proportion of a company’s customers and revenue corresponding to 0.63% and 0.78% decreases respectively in the average number of patents filed. This suggests that companies who sell to customers in foreign countries likely experience greater uncertainty and will thus be more risk-averse in times of higher geopolitical risk.

The Impact of Geopolitical Risk on Innovation is Long Lasting.

Despite the short-lived nature of many geopolitical conflicts and risks, the effect on private sector innovation is long-term. In general, the negative impact of geopolitical risk on innovation typically persists for three to five years, on average reaching its peak a full two years after the initial rise in GPR. While a conflict may be short-lived, its repercussions are likely to be felt for years to come.

Top Geopolitical Risks Affecting Vietnam’s Investment Landscape

Most foreign investors, after investing in Vietnam, share the common opinion that although Vietnam possesses many strengths, especially in economic potential, there remain several geopolitics-related limitations that hinder their investment decision. Domestic investors also report the same inadequacies and difficulties that hamper their business potential.

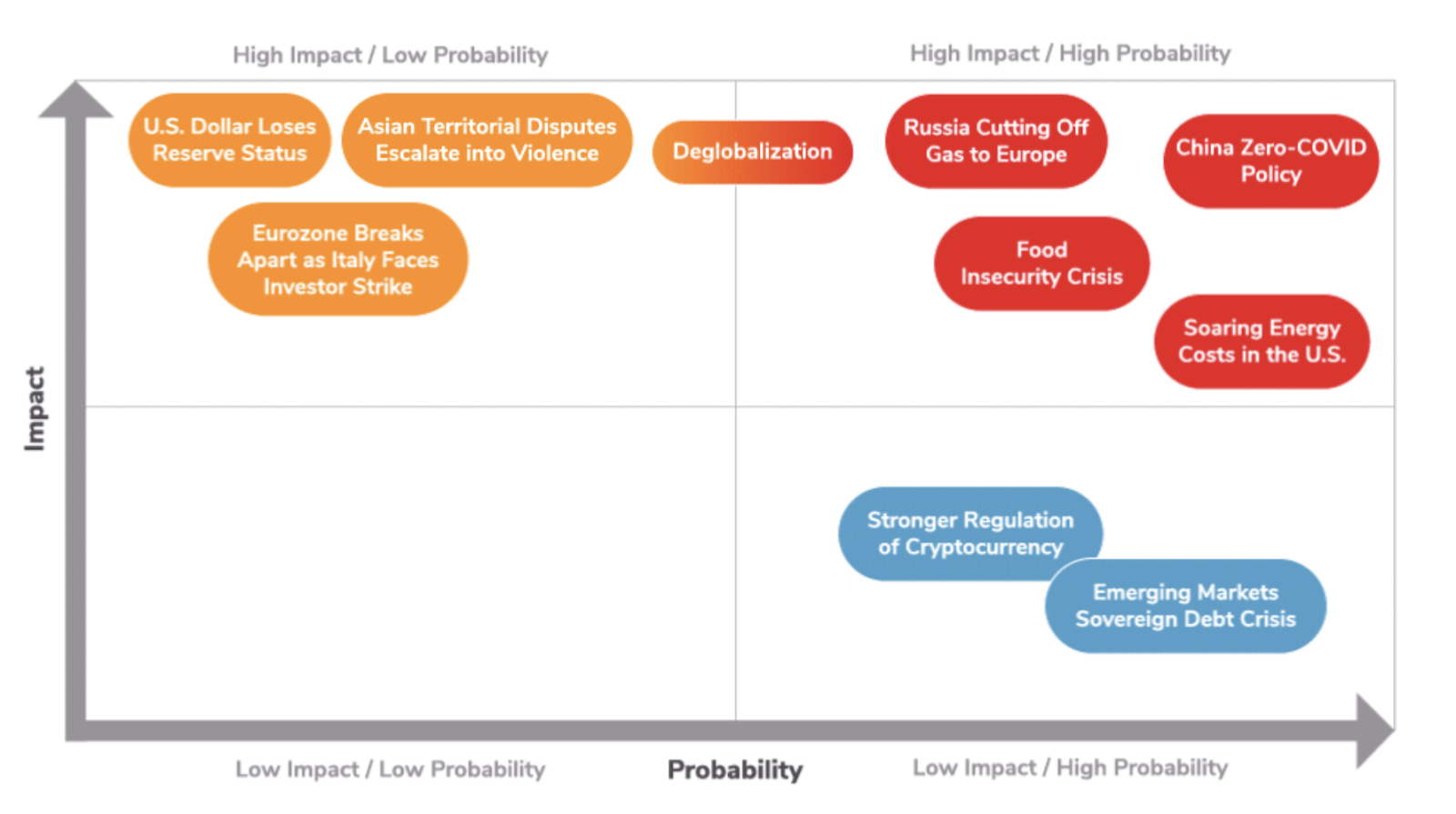

Source: Internet. 10 Biggest Geopolitical Risks by Likelihood and Impact in 2022.

Specifically, the most recent report by Kroll identified the 10 biggest geopolitical risks for 2022, with high inflation risks resulting from unceasing political conflict between Russia & Ukraine and China’s Zero Covid policy presenting the biggest impact on Vietnam’s investment panorama.

High Inflation pressure

Inflation risks still exist as the Russia-Ukraine conflict continues to be prolonged, which causes severe disruptions to global supply chains. It poses a stealth threat to investors since it chips away at real savings and investment returns. Higher-than-expected inflation could hamper economic growth and lead to tighter monetary policy. In such a case, the State Bank of Vietnam (SBV) will have less room to maintain a loose monetary policy to support the economy.

Zero Covid-19 Policy

The closure of factories in China due to the Zero COVID-19 policy can create a negative impact on Vietnam’s manufacturing sector as Vietnam is highly dependent on input materials such as textiles, metallurgy, chemical, and electronics from China. Therefore, if the supply from this market continues to be interrupted, enterprises are forced to import from Japan and Korea at 15-20% higher prices. With this input material price, investors are at risk of not being profitable, making their products difficult to compete in the global market.

Turning geopolitical & policy risk into strategic advantage

The volatile economy has taught businesses one thing that it’ll never be enough just simply to acknowledge the existence and likelihood of political risks. What’s more important is that they must take a further step in mapping out the impact of political risks across their company’s activities to better anticipate and prepare for potential disruptions, mitigate their impact, and even turn them into advantages.

That the presence of a “risk” does not automatically mean that the worst case will happen or that the resulting events will even be negative at all. The potential consequences of geopolitical risk can be either positive or negative.

On the one hand, a risk can potentially lead to economic and political instability, which can, in turn, lead to violence and conflict. On the other hand, they can also spur innovation and creativity as countries attempt to mitigate the risks. But that’s just the theory. Bringing it to reality is a totally different story. But with Viettokin, we can make it happen. Our GPR analysis solution can help decision-makers stay ahead of potential issues and get clarity on how the region may respond.

With a team of highly competent experts, we’re confident to deliver risk consulting and advisory solutions that are timely, market-relevant, and forward-looking. We help organizations understand these geopolitical risks and their interrelationships, to quantify and model their impact, and to design risk mitigation strategies that will result in better market acquisition. We also identify political drivers that move markets and forecast outcomes and scenarios. This way, Viettokin assists clients in incorporating political futures into their business and investment strategies.

Final Thoughts

In today’s era where business and transnational political events are increasingly intertwined, geopolitical and policy risk analysis has better be done timely, accurately, and ultimately produce actionable guidance. That is why leading companies and organizations, from domestic to foreign agencies, have come to rely on Viettokin for analysis they can directly link to vital decision-making.

Geopolitical & Policy risk analysis based on data insights provided by Viettokin’s team of experts can be a really powerful edge to take over your competition. Our comprehensive advisory service platform enables a holistic approach to help both domestic and foreign investors address these issues within the context of their own unique operations.

Activities of businesses in Vietnam in the first half of 2022 brought an optimistic outlook to the economy of the whole country due to the strong post-pandemic recovery. However, the situation has slightly changed in the second half of the year in which new difficulties have emerged and the business results of the fourth quarter of 2022 are differentiated. Beside the negative impacts of the world economy, businesses in Vietnam in 2022 must face capital depletion, although the business opportunities in Vietnam are expected to be positive in 2023.

According to a recently issued global research report by Standard Chartered Bank in January, Vietnam’s economy is forecasted to grow 7.2% in 2023 and 6.7% in 2024, following a solid recovery to 8.0% in 2022.

“We still have a conviction on Vietnam’s high growth potential over the medium term,” said Tim Leelahaphan, Economist for Thailand and Vietnam, Standard Chartered. “While macro indicators moderated somewhat in Quarter 4 2022, they remain largely robust. Retail sales posted solid growth in the second half of 2022, implying improved domestic activity.”

The forecast shows that Vietnam is emerging as one of the top go-to destinations for foreign investors in Southeast Asia. This also means businesses in Vietnam will have big opportunities and a favorable economic environment to capitalize on. To optimize these advantages, businesses in Vietnam should make concerted efforts and Vietnam in general should find appropriate solutions to overcome existing challenges.

Highlights of businesses in Vietnam in 2022

According to a report by the General Statistic Office, in 2022, Vietnam had more than 208 thousand enterprises to register for new establishment and return to operation, an increase of 30.3% compared to the previous year. On average, there are more than 17 thousand businesses per month that decide to establish and return to operation.

By economic sector, in 2022 there were 1,959 newly established enterprises in the agriculture, forestry and fishery sectors, a fall of 2.0% compared to 2021; 36.3 thousand enterprises in industry and construction, a raise of 16.1% and 110.3 thousand enterprises were in the service sector, a raise of 31.9%.

These numbers show the prospects in production and business in the last months, after a long period of stagnant due to the global pandemic. However, businesses in Vietnam still had to face numerous difficulties and challenges.

Capital depletion and the turbulence of bonds, credit and securities

The report of the General Statistics Office also shows that in December 2022 alone, 11,384 businesses withdrew from the market, of which 3,776 enterprises registered to suspend business for a definite time; 5,847 enterprises halted their operation while dissolution procedures are pending; 1,761 enterprises completed their dissolution procedures.

These figures are the result of many disadvantages that businesses in Vietnam are facing. In the context that the world economy is fluctuating due to geopolitical factors, Vietnam’s demand for imported goods is directly affected, causing aggregate demand to decline. Moreover, countries around the world will continue to tighten their fiscal and monetary policies to combat inflation, which means that external interest rates will increase. Meanwhile, domestic consumption, which is the foundation for growth this year, is facing the risk of a sharp decline due to disruptions in the financial market and real estate market.

Nevertheless, the most concerning problem that most businesses in Vietnam are struggling with in 2022 is capital depletion. A survey by the Private Economic Development Research Board under the Prime Minister's Advisory Council for Administrative Procedure Reform shows that, from the second half of October 2022, private enterprises are in urgent situations because of lack of capital, no cash flow to maintain production and prepare raw materials for next year's production periods. This difficulty occurs not only with industries directly related to real estate, but also with many other industries such as supporting industries, agriculture, etc.

This precarious situation due to depleted capital can stem from the fact that all three pillars of the capital market - bonds, credits and securities - were suddenly congested at the same time, leaving businesses in Vietnam unable to respond accordingly.

Since the Tan Hoang Minh event occurred in April 2022, Vietnam’s corporate bond market has been facing continuous difficulties, leading to the risk of cross default. Over the past month, the wave of bond run took place on a large scale, businesses have had to buy back nearly VND 160,000 billion of bonds ahead of time (an increase of more than 50% compared to the same period last year), while the issuance of new bonds decreased by 54%. The wave of bond run also led to fund run (shunning from bond investment funds), causing some bond investment funds to face liquidity risk.

The turbulence in Vietnam’s corporate bond market has spread to the stock market as a crisis of confidence escalates. Compared to the end of last year, the stock market capitalization has decreased by 50%, or about USD 160 billion has evaporated.

Meanwhile, under pressure of inflation, interest rates, exchange rates and liquidity, bank credit was also tightened. If in the first 6 months of the year, credit increased by an average of 1.56%/month, then in the last 4 months, credit increased by an average of 0.5%/month.

As a result, the VN-Index saw the strongest drop in the world in many sessions, and the stock price fell deeply beyond the expectations of many investors.

Positive business environment in Vietnam in 2023

On the bright side, some businesses are finding ways to save themselves and businesses in Vietnam in 2023. The hope for a favorable business environment in Vietnam is coming from two indicator stocks, NVL and PDR. In particular, with NVL, NovaGroup has announced that it will sell 150 million shares of NVL to have more money to deal with bond issues. Similarly, Phat Dat has recently announced the early settlement of the 9th bond issue in 2021 with a total value of VND 150 billion, bringing the outstanding bond balance down to 2,698 billion VND, while the value of the collateral assets was about VND 7,000 billion.

Despite all the hindrances, the outlook of business opportunities in Vietnam in 2023 is quite a positive one. The results of a survey on business trends of enterprises in the processing and manufacturing industry in the fourth quarter of 2022 by the General Statistics Office showed that: 32.6% of enterprises rated better than in the third quarter of 2022; 33.7% of enterprises said that the production and business situation was stable and 33.7% of enterprises rated it as having difficulties.

It is expected that in the first quarter of 2023, 31.5% of enterprises assessed the trend would be better compared to the fourth quarter of 2022; 37.3% of enterprises think that the production and business situation will be stable and 31.2% of enterprises forecast more difficulties.

In conclusion

After a strong rebound from the pandemic, businesses in Vietnam in 2022 still had to encounter several difficulties both from the world geopolitical situation and domestic turbulence. One notable problem faced by businesses in Vietnam is capital depletion as a result of the instability of the capital market's three primary pillars - bonds, credits, and securities. Vietnam’s corporate bond market has slowed down in 2022 due to liquidity risks and declining investor confidence. However, it is believed that this is a necessary step back to reflect, transform and develop more sustainably for businesses in Vietnam in 2023 as numerous experts are optimistic about the business environment in Vietnam in the next year.

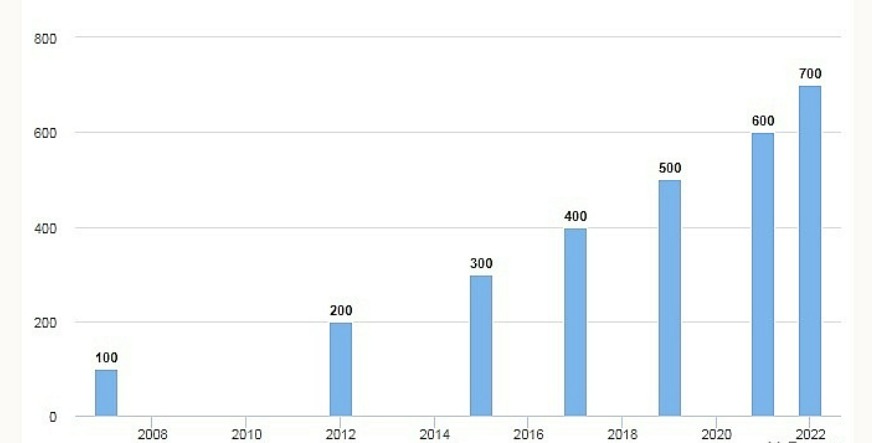

According to the Ministry of Industry and Trade (MIT), the number of Vietnamese export orders in November, 2022 has decreased due to the global turbulence. Yet, regarding the 11 months, Vietnam recorded an estimate of USD$ 673.82 billion in the total export volume, up 11.8% over the same period last year. With the export value and growth being impressive, the total trade volume of Vietnam has reached a new peak of USD$ 700 billion in the middle of December 2022. This figure exceeded 2021’s value (USD$ 668.5 billion), signaling new potentials for both Vietnam and partners.

Behind USD$ 700 billion

Compared to 15 years ago when Vietnam was an official member of the World Trade Organization (WTO), the total value of import and export has now increased by 7 times.

As of the first 11 months of 2022, estimated export turnover was USD $ 342.21 billion, rising by 13.4% over the same period last year. The foreign-invested sectors increased by 14.6% to reach USD$ 254.75 billion, while the domestic economic ones recorded USD$ 87.5 billion, up 10.1%.

On the other hand, import of goods was estimated at USD$ 331.61 billion turnover, growing by 10.1% over the same period in 2021, of which the domestic economic sectors gained USD$ 115.4 billion (up 11.2%) compared to USD$ 216.18 billion of the foreign-invested sectors (up 9.6%).

In 2022, Vietnam’s total import-export turnover is projected to exceed USD$ 730 billion, and the trade surplus may land at over USD$ 10 billion. This marks a milestone of 7 consecutive years Vietnam maintaining a trade surplus. Thus, with remarkable achievement in international trade this year, Vietnam’s import-export ranking will be improved on a global scale.

As to the ranking of WTO, Vietnam continuously secures its name in the top 30 nations with the largest import and export value globally. In 2021, albeit the impact of Covid-19 pandemic, Vietnam still placed 23rd and 20th as the biggest exporter and importer in the world. In the ASEAN region, Vietnam came second only to Singapore.

Diverse trade partnerships and free trade agreements have contributed to great achievements of Vietnam's import and export

Vietnam has extensive trade relations with various countries around the world, with special partnerships with China, the United States, Korea, Japan, EU, ASEAN, among others.

In particular, the United States (US) has always been Vietnam’s biggest importer while China has been the most major exporter of Vietnam for years. In the first 11 months of 2022, the export volume of Vietnam to the US market achieved USD$ 101.5 billion, increasing by 18% over the same period last year and accounting for nearly 30% of the national trade turnover. Meanwhile, Vietnam’s import of Chinese products and services in 11 months was USD$ 109.46 billion, up 10.12%.

Vietnam’s export value in several large markets namely the EU, Korea, and Japan also achieved high export growth thanks to diverse FTAs in effect, thereby helping to facilitate trade and preferential tariffs. Particularly, Vietnam’s exports to the EU market in 11 months achieved USD$ 43.5 billion, witnessing a 21% increase, while the value of exports to Korea and Japan landed at USD$ 22.5 billion and USD$ 22 billion, respectively.

The MIT assessed that enterprises in Vietnam have been accustomed to FTAs, effectively applying the agreements. For example, after the 3 year implementation of the CPTPP, the export turnover to members in the bloc increased by 75-100%. Notably, telephones and components, electronics and computers, machinery, spareparts, textiles, leather and footwear, among others are the main export items to this region. In addition, with the advantages of EVFTA, numerous products exported to the EU market have experienced high growth, namely iron and steel (200%), coffee (over 75%).

Vietnam's role in the global supply chain is becoming increasingly significant.

Mr. Alex Tatsis - Head of the Economic Department of the US Consulate General in Ho Chi Minh City emphasized the important role of Vietnam in the global supply chain, especially for the US at the recent Export Forum 2022.

“Vietnam is the 10th largest trading partner of the US in the world and has become an indispensable node in the US essential goods supply chain. Vietnam has exported to the US hundreds of billions of dollars worth commodities, namely phones, computers, textiles and garments, and imported from this country computer chips, wood, cotton, and animal feed.”

This can be said that the links between Vietnam and the US in the supply chain are tense and interdependent.

As to Mr. Brian Lee Shun Rong, Vietnam’s industry has been developing strongly. The data of Maybank indicates that both FDI inflow and export turnover of Vietnam in the past 10 years have always outdone those of other counterparts in Southeast Asia. Remarkably, electronics and telephone industries have surpassed the textile and garment industry regarding the fields contributing to highest export turnover. This proves that Vietnam has enhanced its position in the global value chain.

For China, Vietnam is a significant strategic partner in various aspects. In international trade with China, despite being affected by Covid-19, Vietnam has successfully exported nearly USD$ 53 billion worth of goods after 11 months, mainly adding to the overall growth figure of 13.4%. In the context of China's zero-Covid anti-epidemic policy, trade with China was tightened. Yet, thanks to the mutual agreements between the two countries in the recent visit of the General Secretary Mr. Nguyen Phu Trong to China, the Chinese market is open to a wide range of agriculture products such as durian, passion fruit, bird’s nest, sweet potato, among others from Vietnam.

In addition, Vietnamese-produced phones and components have played a vital part in the total export value of Vietnam with USD$ 55.4 billion, up 6.6% over the same period in 2021. Plus, Vietnam recorded 8 items with export turnover of over USD$ 10 billion, which made up for 70% of the total export value after 11 months.

Challenges ahead the road

In spite of achieving impressive results, the MIT acknowledged that with the current global demand growing at a slow-moving rate, especially in the top Vietnamese’s leading markets - the US and EU, Vietnamese export and import face several perceived challenges.

To be specific, the export market is slowly narrowing down due to the decreasing global consumption demand. As a result, some of Vietnam's key export products to these markets are encountering strict investigation on trade remedy and origin fraud. At the same time, the European market is accelerating technical barriers related to the environment, sustainable development, green transformation, among others, putting many enterprises in a passive position with various limitations in market access.

Additionally, China has eased its monetary policies, leading to the depreciation of the Yuan, the price of Chinese-exported commodities gradually reduced. Consequently, Vietnamese goods have been in fierce competition with China export products in the US, EU Japan, and East Asia markets.

Vietnam are promoting international trade and expanding the market

Under such situations, the MIT suggested diversifying import and export markets, opening new opportunities for foreign investors, exporters and importers.

In particular, taking advantage of new-generation FTAs will help enterprises to reach out to new markets and reduce their reliance on the traditional ones. The MIT will also vigorously carry out tremendous initiatives to boost trade promotion, match supply and demand via different international trade routes and e-commerce platforms, and assist companies in gaining access to new policies of each market. This will lower barriers to market diversification and export promotion.

Furthermore, Decision No. 2615/QD-BCT has recently been issued to approve the list of "reputable exporters" to encourage import-export enterprises. Thus, 281 businesses were chosen, based on the recommendations of 54 agencies and selection organizations (including ministries, branches, industry associations, provincial, and municipal departments of industry and trade).

At the same time, the MIT's export turnover criteria are used to select and suggest the exporters to include in the list of reputable exporters, which is then put out for public consumption. This is a support activity for Vietnamese businesses to export and expand markets, and assist enterprises' participation in numerous bilateral and international free trade agreements.

In conclusion

Vietnam import and export are presenting various potentials to enterprises, yet how to seize the chance and harvest on the turnover? Thus, to capture the benefits, advice should be sought from top-notch experts with the right local expertise. Viettonkin is one of the leading professional firms with more than 13-year experience in diverse industries and majors. Our team of well-informed professionals in Vietnamese markets and legal systems are capable of assisting you navigate through the process of establishing a new business in Vietnam. With us by your sides, you can focus on what really matters to you. Let us be your trustworthy partner!

What is known as core technology - semiconductors - hold a vital position in global economic development. Thus, the manufacturing and producing this component is not an easy task, and without doubt, not any country has the capacity to do so. Yet, as the importance of the semiconductors is increasingly widely recognized, nations worldwide have made great attempts to independently produce the chips.

The burgeoning demand for semiconductors with perceived challenges in production capability

Semiconductor chips are the brain of any electronic appliances and advanced technologies, from television, smartphones, and computers to AI, 5G, and blockchain. This means they enable machines and appliances to perform key functions, namely data processing, storage, input and output management, among others.

Pat Gelsinger - CEO of Intel Corporation - assessed “We have seen the growing demand for semiconductors from the world's growing digital trends. This process has been fueled during the pandemic and it spurred demand for semiconductors.” With demand on the rise, countries with capacity in semiconductor production are dominating the market and becoming the main global supply.

However, manufacturing this core component is challenging!

This can be attributed to the sophistication in the making process of a semiconductor chip, which requires a diverse number of high-tech and advanced machines in the production chain. Along with that, a semiconductor is combined by rare and special input material. Thus, setting up a semiconductor production plant is a huge investment.

At the same time, the pandemic and most recently, the conflict between Russia and Ukraine have disrupted the global supply chain, severely affecting the production and distribution of the semiconductors. Meanwhile, major players in the market are now moving towards advanced chips due to the high profit margin. As a result, the supply of the semiconductors for daily electronic devices is in dire shortage.

In short, semiconductor production turns out to be the battle game of big fish and superpowers.

The current runners-up in the fierce competition of producing semiconductors.

The USA - the birthplace of semiconductors

The USA used to dominate over 50% of the semiconductor market thanks to the advantages of the first-mover. Yet, Taiwan and Korea soon took the lead, reducing the USA’s market share to 12%.

With the slogan “the American invented Semiconductor, the American will bring Semiconductor back home”, the USA has been attempting to regain its power in the market. Accordingly, the government has passed new policies on high-technology production, which stipulated the $USD 52 billion investment in initiatives, designs and manufacturing of semiconductors.

In addition, through the Science and Chips Act, the US also officially competed with China. The country offers diverse incentives, along with laying the restrictions on countries that cooperate with China, while calling for setting up manufacturing plants in the US.

Just behind Taiwan, Korea is the homeland of the largest world manufacturers, Samsung and SK Hynix Inc., to name a few. In Quarter II, 2021, Korea invested $USD 6,62 billion, up 48% over the same period in 2020 and ranking second globally. Besides, the Korean government planned to finance 950 billion won (approximately USD$ 700 thousand) to research and develop electrical and automotive chips from 2024 to 2030. Additionally, 1,25 trillion won (equal to over USD$ 875 million) will be spent on artificial intelligence chip development by 2029.

China - Big investor in semiconductors production

A report by the global industry association SEMI shows that in the second quarter of 2021, China invested USD$ 8.22 billion in chip-making equipment, up 79% year-on-year and up 38% over the first quarter of 2021.

The heavy investment in semiconductor manufacturing is part of China's strategy to become a technology powerhouse. The country has been trying to find a way out of dependence on foreign manufacturers in the semiconductor sector for decades.

According to the National Bureau of Statistics of China (NBS), China's production of integrated circuits (ICs) and industrial robots increased by 16.2% year-on-year in 2020. However, China is still not able to be self-sufficient in chip sources. In just 2020, China spent USD$ 350 billion importing chips for other manufacturing industries. Mainland China's manufacturing industry is still dependent on advanced chips of Intel (USA), Samsung (Korea) or TSMC (Taiwan).

The challenges remain for China as the country is under the US Law - restricting countries from cooperating with China - and its own zero-Covid policy. This will have a certain impact on the supply chain of several nations on relationships with China.

ASEAN - the rising player in the semiconductors production game

When semiconductor manufacturing was halted by a hard strike of Covid-19 pandemic and its global supply chain was once seriously disrupted, the world semiconductor makers recognized the risk of over-depending on China. Thus, they are moving towards new promising destinations. ASEAN is the most potential one!

ASEAN is uniquely positioned as a neutral region with a well-established and diverse semiconductor ecosystem. Since the 1970s, ASEAN knows semiconductors, and its governments continue to support investments in this sector

Amarjeet Singh - EY Asean Tax Leader; Partner, Ernst & Young Tax Consultants Sdn. Bhd.

In recent years, the ASEAN semiconductor industry has received a boost from FDI, increasing exports and integration into global value chains. According to the UN Comtrade, in 2019, US$200 billion semiconductor export volume came from ASEAN region, with 5 out of 11 ASEAN members being the top 15 global semiconductor exporters. Plus, ASEAN was also the second-largest semiconductor exporting region globally, accounting for 22.5% share of the world semiconductor export.

The astonishing figures in the semiconductor industry in ASEAN can be explained by the joint contribution of its members to the industry. In particular, Malaysia, Singapore, Vietnam, the Philippines and Thailand are at the forefront of R&D and IC design. At the same time, Malaysia and Singapore are regional leaders in wafer manufacturing, and equipment manufacturing. Malaysia, the Philippines, Thailand, Vietnam and Indonesia excel at ancillary manufacturing, while Singapore and Thailand lead in engineering software. In this way, the whole region is creating a great value on the global semiconductor value chain.

Figure 1: The spread of semiconductor specializations across the region (Source: EY)

Moreover, the government in each country is encouraging the development of high technologies and emphasizing on the production of semiconductors. For instance, under the Making Indonesia 4.0 roadmap of the Indonesian government, the electronics sector is one of Indonesia’s five targeted essential sectors. This sector attracted FDI inflow in excess of USD$ 3,3 billion from 2010 to 2020.

In addition, major semiconductor manufacturers and ASEAN members have cooperated to set up their manufacturing plants and R&D centers. Particularly, foreign chipmakers have been establishing manufacturing operations in Malaysia since the 1970s, and the country has developed a position in the global supply chain as a major semiconductor assembly, testing and packaging location. At the same time, Samsung has also been constructing a new USD$ 220 million R&D center in Vietnam to develop products as well as in new technologies such as artificial intelligence, the internet of things (IoT) and big data. Meanwhile, Intel has invested USD$ 1.5 billion USD since its establishment in Vietnam. At the national level, the US and Malaysia have signed a memorandum of understanding (MoU) on collaborating to strengthen semiconductor supply chain resilience and promote sustainable growth.

Conclusion

The context of semiconductor competition is changing as the world manufacturers in the industry are finding their ways to dominate the game. With the unprecedented appearance of Covid-19 pandemic, key players have sought solutions to diversify their semiconductor supply chain, which give rise to ASEAN.

Yet, despite offering tremendous favorable conditions for the top semiconductor makers, the region still presents several challenges. The questions have been raised by various manufacturers “Which destination should I choose to settle down my business?” “How can I navigate myself through the local environment?”.... With 12-year practice in diverse industries and majors and a team of well-informed professionals in local markets and legal systems, Viettonkin can help you find out the answers in this article. Stay tuned and Let us be your trustworthy partner!

Over the past decades, agricultural digitalization is growing in popularity thanks to its potential in boosting productivity and providing consumers with greater transparency in the production process.

Many experts believe that rapid digital transformation is the best way for Vietnamese agriculture to recover and develop in the post-pandemic period, affirming its role as one of the key pillars of the country’s economic growth. Amid challenges from climate change, market fluctuations, and changes in consumption trends, digitalization is expected to open up a new era for the sustainable development of Vietnam’s agriculture industry.

Current market performance

GDP Contribution of the Agriculture, forestry, and fishing sector in Vietnam from 2011 to 2021. Source: Statista

The latest report released by Statista in October 2022 reveals that agriculture accounted for 12.56% of the country’s GDP in 2021. The sector also provides 39.45% of the total employment in the country. With the growing digitalization trends, the invention of more innovative tools by agritech startups to sustain food security in Vietnam is no longer far-fetched.

Scope of digital implementation

At present, Vietnam’s agritech industry is still lagging behind other countries in spite of its status as an agricultural nation. Even with its large number of small to medium-scale farming households, the number of agritech companies and projects is still limited.

Up to this point, the country has 12 areas certified for hi-tech agriculture. The three most prominent zones include Hau Giang, Phu Yen, and Bac Lieu.

In addition, more than 20 enterprises in the Central Highlands of Vietnam have already applied agrotechnology in their operation and farming, which is linked with computers, smartphones, and electronic traceability systems.

Together with domestic investors, foreign agricultural companies also play a crucial role in shaping the agritech sector in Vietnam. The German corporation Bayer Global and Thai-based conglomerate Charoen Pokphand are currently setting their name as one of the top strategic investors to local enterprises.

Key market players

Vietnamese agricultural enterprises are constantly promoting the application of high digital technologies in production and processing to contribute to restructuring the agricultural sector.

As of now, Demeter, MimosaTEK, Sero.ai, and Naturally Vietnam are considered to be among the leading enterprises in the market.

Demeter was founded in 2017 by Pham Ngoc Anh Tung after executing a $4.4 million USD agriculture project in Ho Chi Minh City. The company initially developed an IoT-driven system at Cau Dat Farms, with support from several international farms. The system enables farmers to automate their operations and effectively manage their farm sites through cloud data storage that provides necessary information about weather, soil quality, etc.

Known as the only company in Viet Nam listed by CBInsight in a group of 100+ global technology companies that are contributing to a better future of agriculture, since its inception, MimosaTEK has been focusing on utilizing precision agriculture to enhance existing farming practices in Vietnam, most of which are experience-based and manual.

In recognition of its innovative solution, in 2017, MimosaTEK was rated as 1 of 10 companies globally to receive the Securing Water for Food Award granted by USAID.

Sero.ai is an AI-driven agritech startup that helps farmers tackle the challenges of erratic crop production by creating a platform that connects farmers and experts together. Farmers are encouraged to take photos of their sick plants and upload them to the platform. Computer vision technology helps users identify the disease and give recommendations on suitable solutions.

“Naturally Vietnam” is a Hanoi-based agritech startup working towards the mission of bringing more transparency to the food market. The company provides an online grocery platform where consumers can purchase traceable food products sourced from six farms in the Soc Son district of Hanoi.

The company also offered seed capital of over $2,000 USD to help individuals build farms from scratch to ultimately be able to bring their produce to the e-commerce platforms.

Needless to say, existing agritech startups in Vietnam are paving the way by using their current innovations to transform farming practices. And in an effort to stay ahead of their Southeast Asian competitors, many of these companies are constantly looking to expand their business scope even beyond the country’s borderline. Indeed, the future ahead for these Vietnamese agritech startups is one that is promising.

Vietnam’s agriculture future roadmap

Government-backed incentives and policy

Prior to the pandemic, there already existed regulatory frameworks that support the digitization of agriculture in Vietnam, despite being quite fragmented.

When the COVID-19 pandemic broke out in Vietnam in early 2020, it placed several burdens on agriculture, particularly weakening the purchasing power and causing serious disruptions in supply chains.

6 months later in June 2020, the Vietnamese Prime Minister signed off Decision No. 749/QD-TTG issuing “Vietnam’s National Digital Transformation Program towards 2025, with a vision to 2030” which defines agriculture as one of eight priority sectors for digital transformation in the country. Accordingly, the Government aims toward:

Developing hi-tech agriculture with a focus on smart agriculture and precision agriculture, increasing the proportion of digital agriculture in the economy.

Conducting digital transformation in agriculture based on data, focusing on the development of large information systems such as those of land, crops, livestock, and aquatic products.

Establishing a network of integrated aerial and ground observation along with promoting the provision of timely information on the environment, weather, and soil quality to the farmers; supporting the sharing of agricultural equipment through digital platforms.

Applying digital technology to automate production and business processes; managing and supervising product supply chains and origin, ensuring timeliness, transparency, accuracy, and food hygiene and safety.

Testing the idea of “every farmer is a trader, every cooperative is a digital enterprise” with the aim of encouraging farmers to apply digital technology to agricultural production, provision, distribution, and prediction; providing training in such application and promoting the development of e-commerce in agriculture.

Robustly digitizing management activities to promptly adopt agricultural development policies and guidelines.

In addition to that, in February 2021, the Prime Minister approved Vietnam’s plan to restructure the agricultural sector for the 2021- 2025 period (Decision No.255/QD-TTG). The plan acts as a supporting foundation to foster smart, modern, clean, and sustainable agriculture through the application of high technology, digital technology, and information technology in all stages of the value chain.

Besides, Vietnam’s accession to various free trade agreements (especially CPTPP, EVFTA, and, RCEP) and the government’s tax incentives are also opening up countless opportunities for local exporters of agricultural produce to participate in global value chains, attracting more investment, and advance the local farmers’ technological knowledge and skills.

Emerging investment trends

Recent years have seen an increasing trend of Vietnam cooperating with other developed countries in the process of transforming agriculture through digital applications.

Some of the most promising opportunities include the IoTs (Internet of things), smart farming, machinery and software, genetic and breeding, and pest management. Low cost, simplicity, and efficiency will enable companies to succeed in the agritech sector in Vietnam.

IoT (Internet of Things)

Both foreign and domestic firms are interested in investing in IoT and blockchain because the entry barrier and investment is relatively low.

Since Vietnamese farmers are predominantly operating in small to medium-farming households, affordable and adaptable solutions to increase production efficiency without significant investment are the top priority.

Several local startups in agritech have already been applying IoT in the production process.

For example, MimosaTEK, one of the most successful startup agritech companies, has offered IoT-based management services to develop an information platform to enhance the livelihoods of farmers through the transformation of experience-based farming activities into information-driven activities.

Foreign investors eyeing this subsector may face fierce competition with local companies since most agritech startup firms are operating within this field. Apparently, domestic firms seem to have more advantages in terms of proximity to the customers and understanding of the local market.

Smart farming

At the moment, some foreign investors that are eyeing this sector in Vietnam include Enzootic (Israel and Hong Kong), GoodHout BV, SmartFarm Co Ltd, FairAgora Asia (Thailand), GAGO (China), Intello Labs (India), Pycno Industries (Australia), Gintel (Taiwan), and Fluence corporation-NIROBOX (Israel).

Since smart farming requires a comprehensive approach from the most basic step of seed planting to post-harvest and product distribution, it may take foreign companies longer to enter a new market. However, they can totally navigate this challenge by collaborating with local companies, who know the market well enough like the palm of their hands. This way, investors can take full advantage of their cutting-edge technology without worrying too much about being off-track with what’s happening in the local market.

Challenges ahead the road

However, even when the Vietnamese government did introduce numerous policies and regulations to promote the application of high tech in agriculture, many domestic and foreign companies still face hindrances.

The first problem has to do with the lengthy procedures to import supply chains and equipment to Vietnam.

The second is the lack of transparency in incentives, weak physical and legal structure, as well as poor management of agricultural input and output.

This results in challenges for foreign firms that have to navigate their strategies when expanding to Vietnam.

Mr. Le Vu Minh, Strategic Consulting Director of FPT Corporation pointed out that many Vietnamese agricultural products ranked top in terms of output, such as rice and coffee, but fall behind in terms of value per volume and productivity per production unit.

“With that being said, it is now the right time to develop the growth and value of the agricultural industry, making them no longer rely on output, but rather on production with digital transformation as a supporting position for the economy,” he added.

Creating the future of investment

Without a glimpse of doubt, Vietnam’s agriculture is at a turning point. The industry remains an important part of the country’s economic development due to its rising significance in global food security questions. Sustainable agriculture and value chain development are thus, strategic priorities in the years to come and it is anticipated that the private sector will play an important role in fastening the process.

With that being said, if you’re still looking for a safe set of hands to help you take a step further into Vietnam’s agriculture market, connect with Viettonkin for more in-depth, up-to-date, and personal investment advice. Here, we gather a community of reputable consultants, with highly developed communication channels along with a network of diverse connections of domestic and international businesses. Contact us now to enhance your chance of business success!

Huge boost to exports

2017 was a year of great significance for both the Vietnamese economy and Samsung Vietnam. Vietnam's export turnover for the first time in history reached more than 214 billion USD, and Samsung Vietnam's export turnover also achieved a breakthrough with more than 54 billion USD for the first time ever.

Samsung Vietnam contributes more than 25% to the total export turnover of Vietnam. This miraculous figure is 150 times higher than Samsung Vietnam's total export turnover in 2009 ($350 million), when SEV began production.

As of June 2018, Samsung has reached the milestone of 1 billion high-tech smart products manufactured in Vietnam. The 1 billion products figure include smartphones, tablets, smart watches, and other basic mobile phone products.

Among those, Samsung Bac Ninh factory produced more than 625 million products, and Samsung Thai Nguyen produced more than 431 million products. Vietnam is currently the second largest smartphone export in the world after China, and Samsung plays a significant role in this acheivement.

Job creation and social development

Along with great economic contributions, Samsung Vietnam has made a positive impact on the social environment. The enterprise is employing more than 160,000 employees, all of whom enjoy a stable income and special benefits.

Samsung has come a long way since 2008, when SEV was first established. At the time, there were only 200 working employees, which grew to 2000 employees in 2009. With the growth of investment and export, the number of staff at Samsung Vietnam has been steadily increasing ever since.

Throughout its history in Vietnam, Samsung has organized many volunteer programs. The most notable of them is the Smart Library program. Up to now, Smart Library has helped to renovate more than 50 school libraries, donate 200,000 book titles, 300 computers, tablets, TVs, DVD players...to serve 50,000 high school students across Vietnam.

The program has created a knowledge exchange space named “S.hub” to be implemented at the General Science Library of Ho Chi Minh City, as well as the National Library of Vietnam. Another example is the "Contributing to build a bright day" program to repair the old schools, give gifts to more than 1,000 students and sponsor a "mobile library" to help them read books for free.

Major infrastructure contribution

In terms of infrastructure, Samsung has built four manufacturing centers in Vietnam and a newly developed R&D center. Other entities under Samsung group have also invested heavily in their manufacturing facilities in the country. These manufacturing centers contain housing, schools, medical centers, gyms…to serve their employees.

Samsung has also invested in infrastructure such as roads, electricity and water networks…in the areas near their manufacturing centers. These infrastructures not only serve Samsung’s facilities, but they have a positive impact on the host city and its citizens as well.

Opportunities and challenges for domestic suppliers

The operation of large electronics corporations like Samsung entails a huge ecosystem to support its production and business activities. Other foreign vendors are flocking to Vietnam to open factories to shorten the supply chain gap, as well as taking advantage of cheap human resources, potential markets and incentives that the Government offers.

The number of level 1 vendors located in Vietnam has increased over the years, increasing 10 times over the years.

As of 2019, Samsung Vietnam has about 210 suppliers (both international and domestic). These suppliers provide plastic components for phone cases, charging cases, molds, packaging, meals, security, hygiene... This number is continuing to rise as the company looks for new partners in the field of equipment and electronic components.

This is a great opportunity for Vietnamese enterprises but is also a big challenge. It is vital that domestic suppliers be competitive in price, technology and quality. If Vietnamese businesses can offer competitive products compared to existing businesses in Samsung’s supply chain, there is no reason why Samsung would not choose domestic suppliers. This is because with the same product (assuming with the same quality), domestically suppliers will be faster, have cheaper prices, and more favorable shipping conditions.

Hanoi is one of the biggest, and fastest growing investment destinations in Vietnam. In recent years, the city has taken a holistic approach in improving its business environment. The city is rapidly developing its logistics infrastructure, industrial infrastructure and satellite areas. From the perspective of an investor, these changes bring unprecedented opportunities due to improvements in the flow of goods, services and highly skilled domestic workers.

Logistics infrastructure

In the upcoming years, transport and logistic infrastructure are expected to continue to be prioritized. Authorities propose that land area for transport projects will make up between 12-15 percent of total land for all construction projects by 2025, up nearly 50 percent compared to 2020.

Transportation

In 2015, The Capital Transportation Plan was approved by the Prime Minister. The road infrastructure network of Hanoi includes 11 routes of belt roads and radial roads (the whole Northern region will have 14 high-speed routes), with a total length of over 287km, and all are 4-6 lanes. Currently, 8 out of 11 routes have been invested and formed.

The 14 high-speed routes in Northern Vietnam

With 11 belt roads and radial roads passing through the area, forming 4 important economic corridors of the Northern region, Hanoi will become the nucleus of the Northern economic region, solidifying its position as one of the economic locomotives of Vietnam.

Most recently in June 2022, Nguyen Chi Dung - Minister of Planning and Investment Ministry - presented an investment proposal on the Ring Road 4 project to the government. Ring Road 4 is expected to be completed in 2027 with the expectation of increasing connectivity between provinces in the region, helping to expand development space, reduce population density in urban areas and its pressure on existing traffic routes.

Other important transportation infrastructure in Hanoi include a $866 million metro line connecting Ha Dong - Cat Linh spanning 13.1km, another metro line connecting Nhon - Ga Ha Noi to be completed in 2027, 5 railway lines connecting with localities, 9 river ports with warehouse systems and auxiliary structures, and Noi Bai International Airport with an increasingly developed logistical support system.

Ports, warehouses and Inland Container Depot (ICD)

Although there have been many positive developments, logistics enterprises in Hanoi still experience many bottlenecks. The first bottleneck is the system of warehouses and yards in Hanoi still lacking in number of locations, connectivity, specialization (cold storage, special goods storage,...). The second bottleneck is the difficulties in getting land clearance to build more logistics centers.

There are still very few ICDs in Hanoi. Regarding their connection to different transport modes, they are currently only connected to roads, and not yet connected with railways and riverways. In addition, major obstacles to the development of logistics services are traffic jams, narrow roads, vehicle load limits…which have increased the costs for enterprises.

Mr. Tran Duc Nghia, director of Delta International, shares that Hanoi needs more logistics centers, more warehouses and yards. But the most important thing is the linkage along the logistics chain, the connection between modes of transport to reduce logistics costs and help the industry become more professional and efficient.

To solve these problems, Hanoi has issued the project “Management and development of logistics activities in the area until 2025”. Accordingly, Hanoi will build a Grade I logistics center (in the North) and a Grade II logistics center (in the South), with sizes between 20ha and 50ha.

These centers connect inland ports, seaports (such as Hai Phong, Hon Gai, Cai Lan) and airports, bus stations, railway stations, industrial zones...The city will also build a specialized aviation logistics center at Noi Bai International Airport or with roads connecting directly to the airport.

In the logistics service development plan in 2022, Hanoi has set its goals to build 2 ICDs within the year (in Gia Lam district and Hoai Duc district). Other agendas include the planning for 2 new logistics centers (in Phu Xuyen and Soc Son districts) and the approval of an international container port (in Co Bi commune, Gia Lam district). The plan also encourages and advocates for continued investment in logistics service infrastructure projects

Industrial infrastructure

Current situation

According to the Ministry of Industry and Trade, currently, the city has 10 operating industrial zones with an area of 1,347.42 ha. Specifically, 9 out of 10 industrial zones with an area of 1,270,5 ha have been consistently put into operation at near 100% utilization rate.

In these industrial zones, a strong emphasis is put on attracting high tech FDI projects. A prime example is developing Hoa Lac industrial zone, which serves as the technology hub of Hanoi. In Hoa Lac, high tech FDI projects are given the largest land reserve, as well as the biggest incentives. High tech enterprises are eligible for exemption in corporate income tax and land rentals for the construction of scientific research facilities. Some cases are entitled to the preferential tax rate of 10% within 15 years. Older, more established industrial zones like Noi Bai industrial zone and Thang Long industrial zone have also had success in attracting high tech enterprises in biotech, high precision manufacturing…

As of early December 2021, Hanoi's industrial zones have attracted over 700 projects. Among them, 303 are FDI projects with a total registered investment capital of nearly $6.1 billion (average of over $18 million/project). The remaining 399 are domestic investment projects with a total registered investment capital of nearly 18 trillion VND.

In Hanoi, there are about 165,000 employees working in industrial zones, including 1,100 foreign workers.

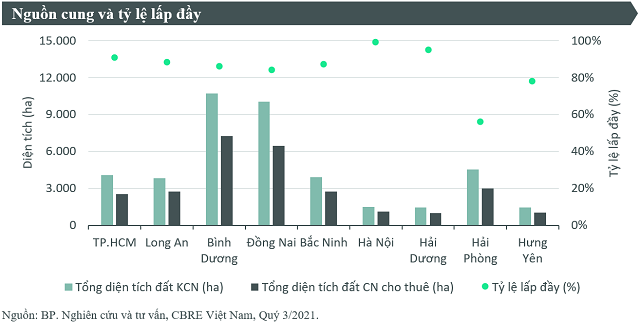

CBRE's report on the industrial zone real estate market in the third quarter of 2021 shows that because there’s not much land availability, the asking price for land in Hanoi is twice as high as in some neighboring localities. The highest rental price in Hanoi is 250 USD/m2, much higher than Hung Yen, Hai Duong at 100 USD/m2 or Hai Phong at 130 USD/m2.

The offer price of industrial land (Q3/2021)

The supply and occupation rate (2021)

Upcoming plans

On January 7, Hanoi People's Committee issued Decision No. 65/QD-UBND approving the project "Establishment of 2-5 new industrial zones, period 2021-2025". With this project, the city determines and strives to complete 5 new industrial zones in the period 2021-2025, specifically: Sach Soc Son Industrial Zone, Soc Son district with an area of 302.8ha; Dong Anh Industrial Zone, Dong Anh District with an area of 300ha; Bac Thuong Tin Industrial Zone, Thuong Tin district with an area of 112ha; Phu Nghia Industrial Zone, Chuong My district with an area of 389ha; Phung Hiep Industrial Zone, Thuong Tin district with an area of 174.88 ha.

Satellite urban development planning

Organizing urban space in Hanoi according to the urban cluster model is expected to be an important driving force for economic and urban development in the capital. The cluster consists of five urban areas: Hoa Lac, Soc Son, Son Tay, Xuan Mai, Phu Xuyen.

Of these five, Hoa Lac is the biggest, has received the most funding and attention to be a hub for scientific and high-technology research with universities and medical centers, among others. However, after 20 years, only the two core zones (out of 6 zones) in Hoa Lac are being developed: Hanoi University area, and the Hi-tech park area.

Tran Dac Trung - Deputy Head of the Management Board of Hoa Lac Hi-Tech Park - said that up to now, the total land area that investors are using in Hoa Lac Hi-Tech Park is about 240ha/1,000ha. Currently, there are 94 investment projects, with a total registered capital of about 91,250 billion VND, of which 55 projects are in operation.

More investment is needed in these satellite areas, and the government has made many incentives to attract investors including tax reduction, guarantee of accommodation for workers, ease of work and travel for foreign workers working in developmental projects, etc.

The General Statistics Office of Vietnam (GSO) has recently published the official GDP growth rate of Vietnam to be 13.67% in Quarter III. Notably, the first 9 months of 2022 has recorded an incredible 8.83% growth in GDP, highest since 2011.

The strong recovery of Vietnamese economy

This record-breaking pace of growth demonstrates that production and business activities are recapturing their growth momentum at a remarkable speed, and that the Government's policies of socio-economic recovery and development proved their effectiveness.

In particular, the agriculture, forestry and fishery industry increased by 2.99%, contributing over 4% to the overall economic growth. Among all sectors within the industry, agriculture contributed the most, with an increase of 2.43%.

Meanwhile, industry and construction experienced a 9.44% increase, comprising nearly 42% of the GDP structure. The manufacturing and processing sector is the primary economic driver, with a 10.69% growth rate.

Similarly, the service sectors also reached 10.57% upturn, accounting for over half of the total GDP growth. Noticeably, the top three sub-sectors devoting to growth of this sector are accommodation and food services, transportation and warehousing, and wholesale and retail with 41.7%, 14.2% and 10.24% increase respectively, compared to the same period last year.

According to Ms. Nguyen Thi Huong - General Director of the GSO, this 8.83% GDP growth is magnificent, especially in light of the current challenges of the global macro-economic atmosphere, with rising inflations, frozen supply chains, and rising energy costs, among others. Vietnam has also managed to keep its inflation rates at bay, helping maintain the stability of the consumer market and daily economic activities. These signals paint a picture of a bright economic outlook with promising growth opportunities for Vietnam in the last months of 2022.

The reasons behind this astounding GDP growth

The effective economic recovery policies of the Vietnamese Government post Covid-19

Vietnam’s policies in response to Covid-19 have proved their effectiveness at a high level, earning the appreciation and admiration from many international counterparts. More than 80% of the Vietnamese population has been vaccinated with a full dose of any Covid-19 vaccine, compared to the average 61.4% of the world population. Thus, the number Covid-19-related of infections and deaths in Vietnam has been declining drastically.

“The successful containment of the pandemic is the primary foundation of maintaining a stable society and reassuring people’s concerns. This will revive, stabilize and develop all economic activities”, stated the representative of the GSO.

In addition, support policies to production and social security have been issued in a timely manner and to the right receivers. In this way, the policies have helped to restore production, at the same time ensuring safety and well-being for all citizens. Specifically, since the beginning of 2022, the Government has issued Resolution No.11/NQ-CP on the Socio-economic Recovery and Development Program. It aims at recovering production and business activities while promoting growth activities, stabilizing the economy and ensuring social security for people.

At the same time, Resolution No. 43/ 2022/QH 15 on fiscal and monetary policies has been introduced to support the Program. The resolution ensures that enterprises and people will soon benefit from exemption, reduction of tax and charges policies, facilitating invoice issuance, tax declarations & submission and united implementation across the country.

Policies to support production through the Economic Recovery Support Program 2022- 2023 will create momentum for the economy to develop in the coming time. As a result of the support policies, business registration has achieved remarkable outcomes. In the first 9 months of 2022, 163 thousand enterprises registered for new establishments and resumed operation, an increase of 38.6% over the same period last year. On average, there are over 18,000 newly established and re-operated businesses on a monthly basis.

The promotion of private-public investment and foreign direct investment (FDI)

The Vietnamese Government determines focused investment projects in major and significant industries to enhance the effective use of public funding. In this way, Deputy Prime Minister Le Minh Khai has just signed Decision No. 1126/QD-TTg on adjusting and supplementing the estimates for the 2022 central budget in investment and development expenditure. In particular, VND 19,570,446 billion has been supplemented for 10 ministries, central agencies and 36 localities to perform tasks and projects under the medium-term public investment plan in the period 2021-2025.

On the other hand, several policies of the Vietnamese government, namely Resolution No. 105/NQ-CP, Resolution No. 128/NQ-CP, among others have reassured the FDI business community. This explains the considerable size of foreign investment flows into Vietnam.

As of September 20, 2022, total registered foreign investment capital in Vietnam reached nearly USD$18.75 billion, down 15.3% compared to the same period in 2021. Yet, the realized foreigin direct investment in Vietnam was estimated at USD$15.43 billion, up 16.3% over the same period last year. This is the highest amount of FDI capital realized in any 9-month period for the past 5 years.

Vietnam as an essential part in the global value chain

The global value chain has still fallen into severe disruption due to the destructive Covid-19 pandemic and the tension of Russia-Ukraine conflict. As an account of Ms. Do Thi Thuy Huong - Vice President of Vietnam Association of Supporting Companies (VASI), the turbulence in the global socio-economic scenario, along with strict Zero-Covid policy of Mainland China has pushed “giant” manufacturers out of China. At the same time, these eyed Vietnam as their next destination for basing middle - and long-term manufacturing plants.

Recently, Apple has moved 11 manufacturing plants in its global supply chain to Vietnam. Meanwhile, Foxcom, Luxshare, Pegatron and Wistron also expanded their existing production facilities in Vietnam. Samsung is building the largest regional Research and Development center worth USD$220 million in Hanoi, Vietnam. Early in this year, it plans to expand factories in Bac Ninh and Thai Nguyen, while still investing an additional USD$3.3 billion in Vietnam. This shift will benefit and move Vietnam up the global value chain.

The reason behind this trend not only lies on the external factors, but also in Vietnam itself. Vietnam has maintained its stability in the political environment while developing its economy. The successful containment of Covid-19 by the Vietnamese government has created tremendous favorable conditions for foreign investors to enter the market.

In addition, according to Ms. Nguyen Thi Huong, the government’s timely decisions to lift up restrictions and open borders have solved the backlogs of the economy. The commercial activities have flourished, while the service sectors recovered rapidly, and travel and transportation improved. She assessed that 2022 and the upcoming time will be the ideal time for opportunity seekers in diverse economic sectors. These factors have made the domestic supply chain resilient compared to the current disrupted global one.

Low and controlled inflation rate

As for the GSO, the domestic price level is generally under control although world inflation continues to rise. The consumer price index (CPI) in September, 2022 increased by 3.94% over the same period last year. Meanwhile, the average CPI in the third quarter and nine months rose by 3.32% and 2.73%, respectively. Inflation rate in Vietnam overall witnessed a slight 1.88% rise.

Last month, inflation in EU countries hiked to a record high of 9.1%, while inflation in the US reached 8.5%, forcing the US Federal Reserve (Fed) to raise interest rates for the 5th time. In Asia, Thailand's CPI in August climbed by 7.9% over the same period last year, whereas Korea’s surged by 5.7%, followed by Indonesia, Japan, and China with 4.7%, 3% and 2.5% increase respectively

Thus, Vietnam maintains to be in the group of countries with low inflation rate compared to the general level.

The GSO also identified several factors leading to the increasing global inflation rate. Most notably, the Russia-Ukraine conflict and supply chain disruption has driven the energy price and the commodity price worldwide.

The low inflation rate of Vietnam is attributed to the proactive response of the government through diverse policies. However, inflationary pressures in the coming months are still present.

The price movement of goods and raw materials in the world is on a downward trend due to the downturn in global economic growth. Yet, the risk of rebound is quite high because of the ongoing intense conflict between Russia - Ukraine

The General Statistics Office.

Accordingly, the government required functional agents to closely update the current situation, hence appropriately assessing and implementing policies. At the same time, they emphasized on the socio-economic recovery and development programs. Most importantly, it is necessary to improve disbursement capacity and effective use of investment capital and focus on investment in key industries and fields.

In short…

The GSO has mapped out two scenarios for economic growth for the year 2022. In the first scenario, annual GDP would grow by 7.5%, which means that Quarter IV’s growth will be 4.14% - the lowest rate for this year. In the second scenario, annual GDP would increase by 8%, equating to a 5.9% growth rate in Quarter IV, slightly higher than the first Quarter yet lower than Quarter II and III. If no sudden and significant upheaval occurs by year end, Vietnam’s economic growth will most likely achieve the latter scenario.

This growth also points at a promising picture for investors, yet also presents underlying risks. In such a context, advice should be sought from top-notch experts with the right local expertise. Viettonkin is one of the leading professional firms with more than 12 year experience in diverse industries and majors. Our team of well-informed professionals in Vietnamese markets and legal systems are capable of assisting you navigate through the process of establishing a new business in Vietnam. With us by your sides, you can focus on what really matters to you. Let us be your trustworthy partner!

Overview of the Logistics Industry in Vietnam

The current situation

Competitive status in service provision

Due to Vietnam's trade deficit, this is an appealing market for Vietnamese logistics businesses. However, because many international corporations invest directly in Vietnam and are also the major importers, a substantial portion of this market remains in the hands of foreign logistics firms. Furthermore, most Vietnamese businesses are still not fully aware of the need to invest in good supply chain management. This makes it difficult for Vietnamese logistics firms to provide value-added logistics services.

Infrastructure deficiencies

Among Southeast Asia's essential economies, Vietnam has the poorest freight infrastructure. Most of Vietnam's seaports are not suited for loading and unloading specialist ships. Domestic airports, on the other hand, lack adequate equipment for loading and unloading products. The country's present warehouse infrastructure is unsuitable for the quick loading and unloading of products, not to mention a lack of energy and information transmission support services (telecommunications).

High cost of logistics services

Vietnam's logistics costs are estimated to be over 25% of GDP, far more than in wealthy nations. This affected Vietnam's ambitions to the high-value chain and increase exports. The fundamental reason for this predicament is that Vietnam's transportation infrastructure is too old and overburdened, the administrative system is difficult, and Vietnamese manufacturers do not actively employ international leasing services 3 PL (third party logistics).

According to the General Statistics Office, Vietnam has more than 98.1% of SMEs, with 99% of these businesses experiencing capital constraints. Financial resources to engage in digital conversion and IT infrastructure development are also significant barriers for logistics organizations. With 90% of firms having less than 10 billion VND in capital and 5% having between 10 and 20 billion VND in the capital, it is difficult to implement expensive technological solutions.

State policies in applying technology in logistics

The Prime Minister issued Decision No. 221/QD-TTg on February 22, 2021, revising and supplementing Decision No. 200/QD-TTg dated February 14, 2017, authorizing the Action Plan to promote energy efficiency, competitiveness, and growth of Vietnam's logistics services by 2025. As a result, the Ministry of Industry and Trade has released an action plan to boost competitiveness and grow logistics services in Vietnam by 2025. In this regard, the Ministry identifies scientific research and technology transfer as forerunners in the integration trend.

The Department of Science and Technology designed and implemented the Project "Research, assess, and propose national standards for logistics" to enhance the standardization of the logistics industry in the context of Vietnam's international integration.

Benefits of Digital Transformation for the Logistics Industry

Automation conserves both money and time.

Automation simplifies overall goods transportation, ensuring that commodities are traceable and arrive on schedule while reducing other financial risks. When there is an issue that creates delays in the transportation process, technology applications are employed to maximize resources and develop backup alternatives.

The palletizing robot, for example, will verify that all items are packaged and ready to export. As a result, the time spent loading and unloading items is reduced, saving firms money on labor costs.

Improve the abilities to assure order progress.

Businesses can use technology apps to track the real travel time of commodities. Because parameters and data are shown in detail from start to end, firms may completely foresee any risks associated with order progress.

Furthermore, digital transformation in logistics assists logistics organizations in optimizing the time spent loading and unloading items, hence reducing the transit route. With this technology, the order progress is also optimized to the greatest extent possible.

Increase the transparency of shipping operations.

Transparency in the delivery process is a fundamental aim that business managers want to accomplish by incorporating IoT logistics solutions. The ability to trace items from the warehouse to the customer's door gives management assurance that all steps of the supply chain are running properly. It also increases client faith in the brand and saves support personnel a lot of time.

Key Trends in Applying Technology in Logistics in Vietnam

Blockchain technology is being used in logistics.

With the advent of Blockchain technology, logistics businesses can now complete digital contracts in the most secure manner possible. Using forthcoming technology will enable all logistics players to establish the most transparent and efficient system for documenting all transactions, tracking assets, and maintaining all papers relevant to the transport sector's activities.

The supply chain's digitalized logistics trend

Digitalization will touch practically all businesses internationally, including the logistics industry. Increasing consumer understanding of digital technology and use of all online channels will assist policymakers in making the best business decisions possible. The use of digitalization in the logistics sector is always anticipated to assist lower the cost of acquiring machinery as well as the cost of the whole supply chain in order to promote revenue development.

The door-to-door delivery of products is a logistics trend.

The field of distribution via information technology has grown in popularity, particularly in large cities. Customers may place orders anytime, anywhere, thanks to this easy application, which requires just smart devices such as phones or PCs with an Internet connection. Delivery work has become more flexible and speedier as a result of advances in information technology.

The trend of safe logistics has risen to the top of the priority list.

With the growth of the internet, there have been increasing worries regarding improved security in logistics firms. All assaults always target business websites such as Amazon, Walmart, and others, exposing cyber security problems. As a result, logistics service providers have been encouraged to focus even more on delivering safe transportation and freight solutions.

Trends in drone and robot delivery

This technology is now available in many nations worldwide. Delivery by delivery plane robots will overcome problems that traditional delivery frequently confronts, such as geography, weather, and so on. Delivery has gotten much easier and more convenient as a result of this technology.

In Vietnam, using technology in Logistics is still a relatively young industry. Viettonkin, as a prominent specialist in this industry, is willing to give consumers up-to-date information and sound financial recommendations. Contact us right away to improve your chances of success!

The Situation of Logistics Disruption

China's Zero Covid policy affects the global supply chain

Vietnam's export volume to China is substantial

The first reason is that China accounts for about 12% of world imports. When products enter there, there is a difficulty with customs clearance, generating congestion, which would damage import and export firms' account receivable turnover.