Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Expanding your business into Indonesia only to get tangled in its employment laws and Indonesia employment laws? You’re not alone. For foreign investors, a misstep in contracts, benefits or terminations can quickly lead to legal exposure, financial penalties and reputational damage.

I’ve helped many clients overcome this challenge. As an FDI specialist with extensive experience in ASEAN markets, Navigating Indonesia’s employment laws can be challenging. Experienced advisors in Jakarta can provide clarity to ensure compliance and growth. This guide is designed to give you the clarity and confidence to hire, manage and protect your workforce in this dynamic market.

This is more than a legal summary; it’s a playbook. We will break down what you, as an employer, absolutely need to know about Indonesian labor law to turn compliance into an asset for your company’s growth.

Key Points

Know the Core Laws: The primary legal framework for employment in Indonesia is established under Law No. 13 of 2003 on Manpower and Law No. 11 of 2020 on Job Creation, together with their implementing government regulations. These laws form the foundation for all employment regulations in the country.

Contracts Matter: Understand the difference between fixed-term (PKWT) and permanent (PKWTT) contracts (permanent employment contract), misclassification can be risky.

Compliance is Non-Negotiable: Employer obligations for minimum wage, social security (BPJS) and mandatory reporting are strictly enforced.

Termination Requires Process: The Omnibus Law has changed the landscape for terminations; employers must follow the procedures and calculations for severance to avoid disputes.

Foreign Worker Rules are Specific: Hiring expats involves a separate process for work permits (RPTKA & KITAS) and rules on which positions they can hold.

Understand the Core Legal Framework and Employment Contracts in Indonesia

To operate effectively you need to have a clear view of the legal landscape. Indonesian employment is governed by a few core laws and their implementing regulations, collectively known as labor law.

The Core Laws: The main law is Law No. 13/2003 on Manpower, which is the foundation.

But the Omnibus Law on Job Creation (Law No. 11/2020) and its regulations have introduced significant changes, especially on contracts, terminations and severance. Think of the Manpower Law as the foundation and the Omnibus Law as the new extension built on top of it.

Employment Contracts: Under Indonesian labor law, there are two main types of employment contracts: 1.PKWT (Fixed-Term Employment Agreement): Which is permitted for temporary, seasonal, or project-based work and must be in writing, with a maximum duration of five years. 2. PKWTT (Indefinite-Term Employment Agreement): Typically used for permanent positions and preferably in written form for clarity and compliance.

Defining the Employment Relationship: It is crucial to correctly classify your workers. The lines between an employee, an independent contractor and an outsourced worker are defined by the level of control and supervision you exercise. Misclassifying an employee as a contractor to avoid BPJS (social security) obligations is a major red flag for auditors. Worker misclassification is a frequent compliance risk in multinational HR audits, often cited in industry reports.

A collective bargaining agreement, negotiated between employers and labor unions, also plays a role in defining employment terms, rights and obligations under Indonesian labor law.

Drafting Legally Sound Employment Contracts and Agreements

Drafting an employment agreement is one of the most important steps for employers and employees in Indonesia. Under the Manpower Law and the Job Creation Law, every employment contract must clearly define the terms of the employment relationship to comply with Indonesian employment law. A well-structured employment contract should specify the job description, employee’s salary, working hours, overtime pay, leave entitlements and the procedures for employment termination.

While Indonesian employment laws recognize both written and verbal employment agreements, a written employment contract is recommended. Written agreements provide clear evidence of the agreed terms and prevent misunderstandings or disputes between employers and employees. Employment contracts should also outline the rights and obligations of both parties to ensure transparency and fairness in the employment relationship.

Employers should review and update their employment agreements regularly to reflect changes in laws and regulations, such as those introduced by the job creation law. By prioritizing clear, compliant and comprehensive employment contracts, businesses can protect themselves from legal risks and build a positive workplace culture.

Key Employer Obligations You Must Not Ignore

Compliance is enforceable. Ignoring these core duties puts your business at immediate financial and legal risk.

Wages, Hours and Leave: Every province has Provincial Minimum Wages (UMP) and some regencies or cities have their own higher minimums (UMK). Employers must pay at least the applicable minimum wages. Standard working hours are 40 hours per week; normal work hours are typically 7 hours per day for 6 days a week or 8 hours per day for 5 days a week. Overtime regulations apply when these daily or weekly limits are exceeded and overtime or part-time work is often calculated based on the applicable hourly wage. All employees are entitled to paid annual leave and public holidays including religious holidays like Eid al-Fitr for which a mandatory religious holiday allowance (THR) must be paid. Paid leave is a statutory right under Indonesian labor law.

BPJS (Social Security): Enrollment in the national social security programs is mandatory.

BPJS Ketenagakerjaan: Work accidents, death benefits, old-age savings and pensions.

Employers must register their employees, co-contribute to the premiums and update the system with any workforce changes. The deadlines are strict and penalties for non-compliance are enforced.

Mandatory Reporting and Record-Keeping: You must report new hires to the Ministry of Manpower. All employment contracts, payroll data and proof of BPJS payments must be retained and be accessible for inspection.

Terminating Employees Legally and Strategically

This is one of the most high-risk areas of Indonesian employment law. A “fire and fix later” approach is a recipe for disaster when it comes to termination of employment. Wrongful termination disputes have risen since the Omnibus Law’s introduction, with labor courts reporting increased caseloads

This is a clear sign that employers must move from reactive to proactive, building a process that is legally sound and strategically smart.

Justifiable Reasons for Termination: An employer cannot terminate a permanent employee or terminate employment without a valid legal reason. Justifiable reasons are serious misconduct, redundancy, resignation or reaching retirement age. All reasons for termination must comply with company regulations and prevailing laws. Attempting a “unilateral termination” without a justified cause will be challenged and likely overturned in industrial court. If an employee rejects termination, the employer must provide written notice and enter into negotiations. If no agreement is reached, the matter may escalate to industrial relations disputes, requiring industrial relations dispute settlement and potentially legal proceedings before the relevant industrial relations court.

Dispute Resolution and Documentation: Both employer and employee are involved in negotiations and must follow proper procedures. If industrial relations disputes arise, the process includes bipartite negotiations, mediation and if unresolved, legal proceedings in the relevant industrial relations court. Valid evidence is required to support any decision to terminate employment especially in cases of alleged misconduct or disputes.

Severance Pay Calculation: The Omnibus Law updated the formula for termination payments. The final amount depends on the reason for termination and the employee’s length of service. It typically consists of several components which may include:

Pesangon (Severance Pay)

Separation Pay

UPMK (Reward for Service Pay or Service Appreciation Pay)

UPH (Compensation of Rights or Compensation Pay), which includes unused leave, pay compensation and other negotiated benefits.

Long Service Pay may also apply depending on the employee’s length of service and the circumstances of termination.

Settlement and Mutual Agreement: Termination of employment can also occur through mutual agreement, formalized in a mutual employment termination agreement. This process ensures that both parties’ rights are protected and all entitlements including the employee’s salary and any outstanding compensation are settled according to prevailing laws.

Infographic: Severance Pay Components by Termination Reason

Resignation: Employee receives UPH only.

Serious Misconduct (after court ruling): Employee receives UPH and potentially Separation Money (separation pay) as defined in the company agreement. Employees terminated for gross misconduct are not entitled to service appreciation pay (UPMK).

Redundancy (due to efficiency): Employee receives 0.5x the standard formula for severance, UPMK (service appreciation pay) and UPH.

Redundancy (due to closure/losses): Employee receives 1x the standard formula for severance, UPMK (service appreciation pay) and UPH. (Note: These are simplified examples; specific calculations must follow the latest government regulations. Depending on the circumstances, long service pay may also be a component of termination benefits.

The Termination Process: For most terminations, the law requires employers to first seek a mutual settlement through bipartite negotiations. If no agreement is reached, the dispute moves to mediation and then to the Industrial Relations Court. Proper documentation of this entire process is your best defense against future lawsuits.

Hiring Foreign Employees—The Rules of the Game

Indonesia welcomes foreign expertise but within a regulated framework designed to prioritize the local workforce. In addition to these general rules, there are specific regulations and restrictions that apply to foreign workers in Indonesia, including registration requirements, permitted employment categories and work permit obligations.

Work Permits (RPTKA & KITAS): Before you can hire a foreign employee, your company must obtain an Expatriate Placement Plan (RPTKA) approval from the Ministry of Manpower. Once the RPTKA is approved, the employee can apply for a Limited Stay Permit (KITAS).

Restrictions on Positions: Certain positions, particularly in human resources, are closed to foreigners. The Ministry of Manpower maintains and periodically updates a list of positions open to expatriates. The game-changer here is structuring your teams intelligently, pairing foreign experts with local talent for knowledge transfer.

Tax and Social Security: Foreign employees working in Indonesia for more than 183 days in a 12-month period are considered tax residents and are subject to Indonesian income tax (PPh 21) on their worldwide income. They are also generally required to enroll in BPJS, although some exemptions exist under specific conditions, and labor union involvement may play a role in representing foreign workers' interests regarding these matters.

Data Protection: Employee Privacy and ComplianceEmployee privacy and compliance with personal data protection laws is a big responsibility for employers in Indonesia.

The Electronic Information and Transactions Law (EIT Law) and Personal Data Protection Law requires employers to handle personal data with extreme care. This means getting explicit consent from employees before collecting, processing or sharing their personal data and ensuring all data handling practices comply with Indonesian labor laws and employment laws.

To meet these obligations, employers should implement robust data protection measures such as encryption, secure access controls and clear procedures for data breach response. Having comprehensive internal policies for personal data protection – including guidelines for data collection, storage and disposal – shows commitment to compliance and employee welfare.

Non-compliance with data protection laws and regulations can result in big penalties and reputational damage. By proactively safeguarding personal data and following Indonesian employment laws, employers and employees can build trust and have a secure compliant workplace.

Build a Compliant HR Framework with Long Term Value

True strategic advantage comes from embedding compliance into your company’s DNA.

Compliance is not just a checklist; it’s a governance culture that protects your business and enhances your reputation. This is how you go big and build to last.

Audits and Inspections: Ministry of Manpower inspections can be triggered by employee complaints, routine checks or industry wide reviews. A proactive internal audit can help you identify gaps in your contracts, payroll and BPJS payments before they become official violations.

Drafting Internal Policies: Beyond the employment contract, your company should have clear internal policies (often called a “Company Regulation” or “PP”) on anti-harassment, grievance procedures and codes of conduct. These policies must align with Indonesian law, not just replicate a global template. Internal policies should also address the role of collective bargaining, collective bargaining agreements, collective labor agreement and collective labor agreements as important tools for defining employment terms and conditions. Anti-harassment and grievance procedures must recognize employee representation, labor unions and the rights of female employees, male and female workers as well as protect against discrimination based on marital status and political orientation. Codes of conduct and workplace safety policies should emphasize occupational health as a key employer responsibility.

When to Get Help: While day-to-day HR can be managed internally, it’s best to get legal or advisory help for complex situations like corporate restructure, mass termination or cross-border hiring. Compliance with employee benefits and measures that improve employee welfare will further strengthen your HR framework.

Conclusion: Your Roadmap

Indonesian employment law is not just about avoiding penalties; it’s a strategic must for any serious investor. By understanding the rules and building a culture of compliance you create a stable and protected environment for your business to grow.

Indonesian employment law is a strategic opportunity for investors. By building a compliant HR framework, businesses can thrive in this dynamic market. Consult experienced legal and HR advisors familiar with ASEAN regulations to unlock growth potential.

Specialized legal advisors in Jakarta can help navigate these regulations that translates complex employment law into a practical strategy for foreign investors scaling across ASEAN. Our team has supported numerous FDI projects across ASEAN since 2007, turning regulatory challenges into growth opportunities. Partner with us to build a strong and prosperous Indonesia.

Vietnam's financial sector, particularly its burgeoning banking industry, represents a critical pillar of the national economy and a significant draw for foreign direct investors (FDI). As the market matures and integrates further into the global financial system, the regulatory framework evolves to ensure stability, transparency, and sustainable growth.

A pivotal recent development for foreign investors eyeing Vietnam's credit institutions is the issuance of Decree No. 69/2025/NĐ-CP by the Government of Vietnam. Effective from May 19, 2025, this amending decree updates key provisions of Decree No. 01/2014/NĐ-CP, directly impacting how foreign entities can acquire and hold shares in Vietnamese commercial banks and non-bank credit institutions.

At Viettonkin Consulting, our expertise lies in turning internal legal and financial complexities into external simplicity. This article aims to break down these new regulations, clarify their implications, and highlight the strategic opportunities they present for foreign direct investors navigating Vietnam's dynamic financial landscape.

I. Context: Evolving Regulations for Vietnam's Financial Stability

The Vietnamese government is committed to modernizing its financial sector, balancing the need for foreign capital and expertise with safeguarding national financial stability. Decree 01/2014/NĐ-CP previously established the foundational rules for foreign investment in credit institutions. However, with the ongoing development of Vietnam's capital markets and the banking system, and especially in light of the Law on Securities 2019 (effective January 1, 2021), certain adjustments became necessary.

Decree 69/2025/NĐ-CP, issued on March 20, 2025, represents a targeted update, addressing key areas to:

Enhance Financial System Safety: By tightening certain acquisition methods and providing mechanisms for the Prime Minister to intervene in special cases.

Improve Transparency: By codifying clearer conditions for share offerings.

Facilitate Restructuring: By introducing new provisions that enable deeper foreign participation in the restructuring of weak credit institutions.

For foreign investors, understanding the specifics of this new decree is not just about compliance; it's about identifying strategic entry points and maximizing long-term investment efficiency in Vietnam's banking sector.

II. Tightening the Scope of Foreign Investor Share Purchase

Amended Scope: Foreign investors may now only acquire shares when a credit institution:

Offers new shares to increase charter capital. This remains a primary avenue for investment.

Sells treasury shares that it purchased before January 1, 2021.

The Rationale Behind the Change:

This amendment is a direct consequence of the Law on Securities 2019. This law fundamentally altered the treatment of treasury shares for public companies (which includes most credit institutions listed on Vietnam's stock exchanges). Under the 2019 law, companies are generally required to cancel treasury shares after repurchasing them. They can no longer be held for resale or used as bonus shares, except in specific, narrow circumstances. In contrast, the older 2006 Securities Law allowed companies more flexibility to hold and resell treasury shares.

Therefore, Decree 69/2025/NĐ-CP aligns the regulations on foreign investment in credit institutions with the prevailing securities law, preventing foreign investors from acquiring treasury shares that, by current law, should effectively be cancelled. This change underscores the importance of staying abreast of interconnected legal frameworks when investing in Vietnam.

III. Updated Foreign Ownership Caps in Credit Institutions

Decree 69/2025/NĐ-CP reiterates and clarifies the maximum shareholding limits for foreign investors, while also introducing a crucial exception mechanism.

A. Ownership Caps for Commercial Banks:

The total foreign shareholding in a Vietnamese commercial bank remains capped at 30% of its charter capital. This overarching limit applies to all foreign investors combined.

Exception for Systemic Safety: In special cases where it's deemed necessary to protect the stability and safety of the credit system, the Prime Minister may approve higher foreign ownership limits. This "systemic-safety exception" can apply to strategic investors or to support the restructuring of weak credit institutions.

B. Ownership Caps for Non-Bank Credit Institutions:

For non-bank credit institutions (such as finance companies or financial leasing companies), foreign investors may collectively hold up to 50% of the charter capital.

This limit is also subject to the same systemic-safety exception mechanism, allowing for higher limits in specific approved cases to ensure financial stability.

C. The 49% Breakthrough: Investing in Mandatory Transfer Banks

Mandatory Transfer Banks: Foreign investors can now own up to 49% of the charter capital in commercial banks undergoing mandatory transfer. This applies to banks that are part of an approved restructuring plan and are not more than 50% state-owned.

Strategic Opportunity: This is a major breakthrough for foreign direct investors. Previously, foreign participation in the restructuring of weak Vietnamese banks was limited by the general 30% cap. The new 49% allowance enables deeper foreign involvement in the recapitalization, governance, and operational improvement of these critical institutions. It opens doors for strategic investors to play a more active role in stabilizing and modernizing a vital segment of Vietnam's economy. This reflects the government's commitment to leveraging foreign expertise and capital for systemic financial health.

IV. New Obligations and Conditions for Foreign Investors & Vietnamese Credit Institutions

The new decree also introduces additional responsibilities and conditions for both foreign investors and the Vietnamese credit institutions offering shares.

A. Additional Obligations for Foreign Investors:

Foreign investors must adhere to new mandates designed to maintain regulatory compliance and prevent excessive foreign control:

Reducing Excess Ownership: If an additional share purchase causes a foreign investor (or a foreign investor and their related parties) to exceed the permissible ownership limit (e.g., 30% for commercial banks, 50% for non-bank CIs), they are now obligated to reduce their ownership to the compliant level within a maximum of six months. This introduces a clear timeframe for rectifying non-compliant holdings.

Ban on Further Acquisitions (General Limit Exceeded): If the total foreign ownership in a credit institution already exceeds the legal limit (e.g., 30% or 50%), no individual foreign investor is allowed to acquire additional shares until the total ownership level falls back into compliance.

Post-Mandatory Transfer Purchase Ban: After the conclusion of a mandatory transfer plan for a commercial bank, foreign investors in that bank are generally not permitted to acquire additional shares. Exceptions are narrow, such as purchasing shares from existing shareholders or other foreign investors, and further acquisitions are only allowed once the total foreign ownership in that commercial bank falls below the general 30% charter capital limit. This ensures that the temporary 49% allowance for restructuring does not lead to permanent circumvention of the general cap.

B. Changes to Terms for Vietnamese Credit Institutions Selling Shares:

Credit institutions seeking to attract foreign investment must also comply with updated procedures:

General Meeting of Shareholders (GSM) Approval: Joint-stock credit institutions are now explicitly required to have a capital increase plan and a treasury share sale plan (if applicable under the new rules) that includes a plan for offering and issuing shares to foreign investors. This plan must be approved by the General Meeting of Shareholders.

State-Owned Enterprise Compliance: For joint-stock credit institutions with more than 50% state ownership, additional procedures must be completed in accordance with laws on the financial management of state-owned enterprises before submitting their capital increase or treasury share sale plan for GSM approval. This adds another layer of governance for state-controlled entities.

V. Implications and Strategic Opportunities for Foreign Investors

Decree 69/2025/NĐ-CP represents a strategic move by the Vietnamese government to strengthen its financial system. For foreign direct investors, its implications are dual-edged: enhanced regulatory clarity coupled with significant strategic opportunities.

A. Enhanced Clarity and Confidence:

Clearer Guidelines: The decree codifies precise conditions and procedures for share offerings and capital increases, contributing to a more stable and predictable legal environment. This transparency is crucial for boosting investor confidence.

Systemic Safeguards: By tightening certain rules and providing mechanisms for intervention, the decree reinforces the stability of Vietnam's financial system, a critical factor for long-term investment.

B. Unprecedented Strategic Opportunities:

Deeper Participation in Banking Restructuring: The most impactful change is the allowance for up to 49% foreign ownership in commercial banks undergoing mandatory transfer. This opens an unprecedented window for strategic foreign investors to:

Inject Capital: Provide much-needed capital to strengthen weak institutions.

Transfer Technology & Expertise: Introduce advanced banking technologies, risk management practices, and operational efficiencies.

Influence Governance: Play a more substantial role in the strategic direction and corporate governance of these banks.

Gain Market Access: Secure a larger stake in the backbone of Vietnam's rapidly growing financial market, positioning themselves for long-term gains as these institutions recover and thrive.

This "major breakthrough" signifies Vietnam's pragmatic approach to leveraging foreign capital to address systemic issues and accelerate the modernization of its banking sector. For sophisticated investors with expertise in financial sector restructuring, this presents a unique and potentially highly lucrative avenue for entry or expansion in Vietnam.

VI. Navigating the New Landscape: Recommendations for FDI

To effectively capitalize on these new rules and ensure compliance, foreign investors in or considering Vietnam's credit institutions should adopt a proactive and informed approach.

Thorough Due Diligence: Before any acquisition, conduct comprehensive due diligence on the target credit institution, understanding not only its financial health but also its regulatory standing and any ongoing restructuring plans.

Understand Specific Definitions: Pay close attention to the precise definitions of "foreign investor," "related parties," "credit institution," and "mandatory transfer plan" as stipulated in the relevant Vietnamese laws and decrees.

Monitor for Implementing Guidance: While Decree 69/2025/NĐ-CP is effective, subsequent circulars or official letters from the State Bank of Vietnam or other regulatory bodies may provide further detailed guidance. Stay vigilant for these updates.

Strategic Planning for Ownership Limits: Investors must plan meticulously to ensure their ownership stakes remain within the prescribed limits, especially considering the new six-month reduction obligation.

Compliance with Vietnamese Credit Institutions: If you are a Vietnamese credit institution, ensure your capital increase and treasury share sale plans (if applicable) are fully compliant with the new GSM approval requirements and, for state-owned entities, the additional financial management laws.

VII. Conclusion: Seizing the Moment in Vietnam's Banking Sector

Decree No. 69/2025/NĐ-CP is a testament to Vietnam's ongoing commitment to developing a robust, transparent, and internationally integrated financial market. While it introduces tighter controls in some areas to ensure systemic stability, it simultaneously opens unprecedented strategic and long-term investment opportunities, particularly through the allowance for deeper foreign participation in the restructuring of commercial banks.

For foreign direct investors seeking to enter or expand their presence in Vietnam's high-potential financial market, this decree provides a clearer and more attractive legal foundation. It signals a new era of engagement, inviting strategic partners to contribute not just capital, but also invaluable technology and management expertise.

Navigating these intricate legal shifts requires profound local knowledge and seasoned advisory. At Viettonkin Consulting, we pride ourselves on turning internal expertise into external simplicity, providing you with the clarity and strategic foresight necessary for successful investment in Vietnam's dynamic banking sector.

Ready to explore the strategic opportunities in Vietnam's financial sector or ensure your existing investments are fully compliant?

Connect with Viettonkin Consulting today. Let our team of legal and financial experts simplify the complexities, allowing you to invest with confidence and optimize your presence in this promising market.

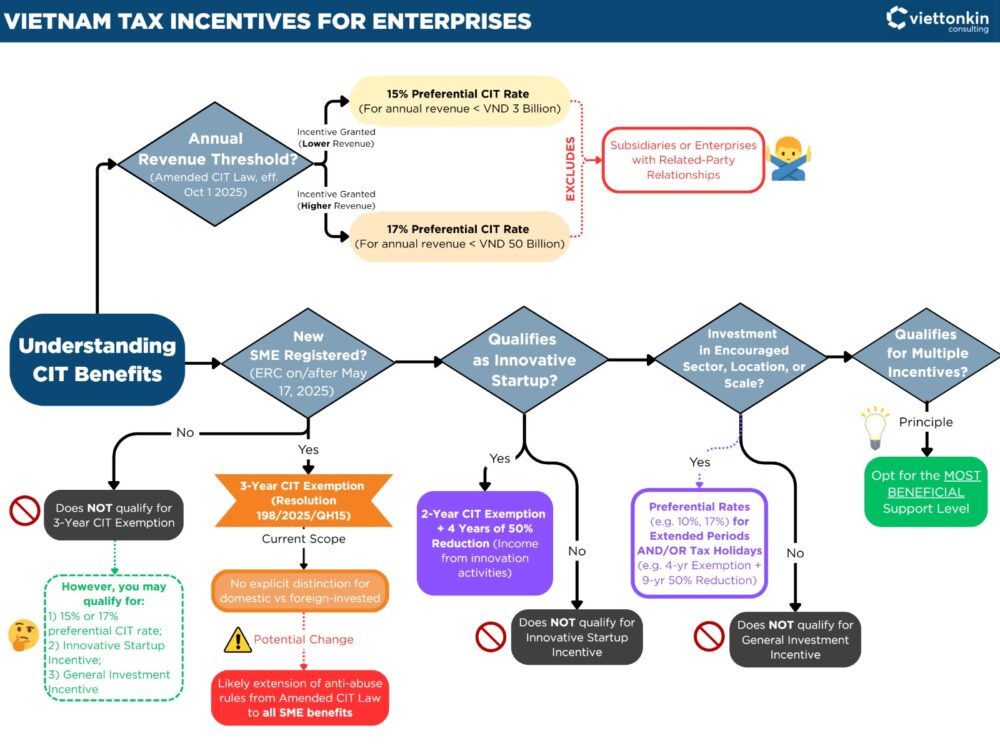

I. Executive Summary: Unlocking Vietnam's 3-Year Corporate Income Tax Exemption for New SMEs

Resolution No. 198/2025/QH15, a landmark legislative act by Vietnam's National Assembly, introduces a significant 3-year Corporate Income Tax (CIT) exemption for newly established Small and Medium-sized Enterprises (SMEs). This pivotal policy is strategically designed to stimulate new business formation and foster robust growth within Vietnam's burgeoning private sector, offering a substantial incentive for both domestic and foreign direct investors eyeing the Vietnamese market.

To qualify for this valuable tax holiday, new enterprises must meet two primary conditions:

Their first Enterprise Registration Certificate (ERC) must be granted on or after May 17, 2025.

They must satisfy the prescribed SME classification criteria as defined by Vietnamese law.

This measure is a direct and impactful component of a broader governmental strategy aimed at bolstering entrepreneurial activity, reducing regulatory burdens, and cultivating a more dynamic and investor-friendly economic landscape in Vietnam. Viettonkin Consulting helps foreign investors navigate these opportunities, ensuring clarity from complex regulations.

II. Vietnam's Private Sector Growth & New SME Support Framework 2025

Context of Resolution No. 198/2025/QH15: Driving Private Sector as Key Economy Driver

On May 17, 2025, the National Assembly of Vietnam officially enacted Resolution No. 198/2025/QH15, a comprehensive legal framework outlining special mechanisms and policies for the advancement of the private sector. This resolution is not an isolated initiative but a concrete and direct implementation of the Politburo's Resolution 68-NQ/TW, which fundamentally redefines the private sector as the primary driver of the national economy. This legislative shift marks a historic departure from previous regulatory approaches, signaling a transition from a restrictive mindset to a proactive, development-oriented strategy aimed at unleashing the private sector's full potential.

Beyond CIT Exemption: Comprehensive SME Support in Vietnam

The 3-year CIT exemption, while substantial, is part of a multi-faceted and comprehensive support system established by Resolution 198/2025/QH15. This broader framework is designed to address various challenges faced by SMEs and to create a more conducive business environment:

Reduced Regulatory Burdens: To alleviate administrative pressure and foster a less intrusive regulatory climate, the resolution limits inspections and audits for business entities to no more than once per year, unless there is clear evidence of legal violations. This measure is intended to curtail regulatory overreach and enhance business autonomy.

Financial and Credit Support: Recognizing the importance of accessible capital, the resolution introduces a 2% annual interest rate subsidy for loans specifically designated for green, circular economy initiatives, or projects adhering to Environmental, Social, and Governance (ESG) standards. This aims to channel investment towards sustainable development.

Land Access Support: To ensure that SMEs, high-tech firms, and innovative startups have adequate physical space for operations, the resolution mandates provincial-level People's Committees to reserve a minimum of 20 hectares or 5% of the total developed land area within industrial parks and cottage industry zones for lease to these entities. Furthermore, these eligible businesses will benefit from at least a 30% reduction in land rental fees for the first five years of their lease contracts.

Support for Research, Development, Innovation, and Digital Transformation: The government encourages innovation by allowing enterprises to allocate up to 20% of their enterprise income taxable income to establish internal funds for science and technology development, innovation, and digital transformation. Additionally, businesses may deduct 200% of their actual research and development (R&D) expenses when calculating corporate income tax. To further support micro and small businesses, the State will provide free digital platforms and shared-use accounting software.

Abolition of Business License Tax: A significant administrative burden is set to be removed with the planned cessation of business license tax collection and payment starting January 1, 2026. This aims to simplify compliance for new and existing businesses.

The extensive nature of the measures outlined in Resolution 198/2025/QH15, encompassing regulatory streamlining, financial assistance, land access, and innovation promotion, indicates that the 3-year CIT exemption is not an isolated policy. This multifaceted approach suggests a foundational element of a comprehensive, strategic overhaul aimed at fostering a more robust, transparent, and competitive business environment for the private sector. This reflects a long-term commitment by the Vietnamese government to reduce systemic barriers and actively nurture entrepreneurial growth, rather than merely providing temporary relief. The emphasis on "removing barriers" and ensuring a business environment that is "open, transparent, clear, consistent, stable in the long term, easy to comply with, and low in cost" reinforces this deeper, systemic intent.

III. Key Eligibility for Vietnam's 3-Year Corporate Income Tax Exemption

The 3-year Corporate Income Tax (CIT) exemption is a significant incentive specifically designed to support newly established Small and Medium-sized Enterprises (SMEs) during their critical startup phase. To qualify for this exemption, enterprises must satisfy two crucial conditions.

Condition 1: First Enterprise Registration Certificate (ERC) Requirements

The primary requirement for the 3-year CIT exemption is that the enterprise must be granted its first Enterprise Registration Certificate (ERC) with an issue date on or after May 17, 2025.

The "Enterprise Registration Certificate" (ERC), often known as a Business Registration Certificate (BRC), is the official document legally authorizing a business to operate in Vietnam, confirming its legal status and functioning as its tax identification number. For Foreign-Invested Enterprises (FIEs), obtaining the ERC is a mandatory step that follows the issuance of the Investment Registration Certificate (IRC).

The explicit wording "first Enterprise Registration Certificate" is a critical aspect, designed as a safeguard against abuse and to ensure the incentive is directed towards truly new market entrants. This implies:

No Re-registration for Existing Entities: An ERC issued due to an amendment or re-registration of an existing entity generally will not be considered a "first" ERC for this exemption.

Mergers & Acquisitions (M&A): A business formed through a merger would typically inherit the rights and obligations of the acquired entity, including existing tax incentives and losses, and would generally not be treated as a "new" entity eligible for this "first ERC" exemption.

Household Business Conversions: While converting household businesses to legal entities is encouraged for broader support, such conversions are also unlikely to qualify for the "first ERC" exemption under the spirit of Resolution 198/2025/QH15, which aims to incentivize genuine new business formation.

This stringent interpretation ensures that the incentive aligns with the broader governmental objective of stimulating fresh economic activity rather than merely allowing existing businesses to restructure for tax relief. For foreign investors setting up new operations in Vietnam, understanding this specific condition is paramount.

Condition 2: Vietnam SME Classification Criteria (Decree 80/2021/NĐ-CP)

The second condition mandates that the enterprise must qualify as a small or medium enterprise (SME) as defined by Article 4 of the Law on Support for Small and Medium-sized Enterprises 2017 (Law No. 04/2017/QH14) and, more specifically, by Article 5 of Decree 80/2021/NĐ-CP.

SME status is determined by specific thresholds related to the average annual number of employees paying social insurance, maximum annual total revenue, or maximum total capital. These thresholds are differentiated by sector (agriculture, forestry, fisheries; industry and construction; trade and services) and by size category (micro, small, medium). It is important to note that these criteria apply uniformly to all enterprises, irrespective of their ownership structure, meaning both domestic and foreign-invested companies can qualify for SME status.

SME Classification Criteria per Article 5 of Decree 80/2021/NĐ-CP

Enterprise Size

Sector

Avg. Number of Employees (Social Insurance)

Maximum Annual Total Revenue (VND)

OR Maximum Total Capital (VND)

Micro

Agriculture, Forestry, Fisheries; Industry and Construction

≤ 10 people

≤ 3 billion

≤ 3 billion

Trade and Services

≤ 10 people

≤ 10 billion

≤ 3 billion

Small

Agriculture, Forestry, Fisheries; Industry and Construction

≤ 100 people

≤ 50 billion

≤ 20 billion

Trade and Services

≤ 50 people

≤ 100 billion

≤ 50 billion

Medium

Agriculture, Forestry, Fisheries; Industry and Construction

≤ 200 people

≤ 200 billion

≤ 100 billion

Trade and Services

≤ 100 people

≤ 300 billion

≤ 100 billion

A notable aspect of this classification system is the self-declaration mechanism. SMEs are required to determine and declare their size (micro, small, or medium) using a prescribed form and submit it to the agencies or organizations providing support for SMEs.Enterprises bear full legal responsibility for the accuracy of their declarations. Should an enterprise discover an inaccuracy in its declared size, it is obligated to modify and re-declare before receiving any support. Intentional untruthful declarations made for the purpose of receiving benefits will result in legal responsibility and the requirement to refund the entire support amount received.

This provision for self-declaration of SME status is a clear governmental effort to streamline the process for accessing incentives, thereby reducing bureaucratic hurdles and empowering businesses to quickly benefit from support. This aligns with the broader governmental agenda of administrative reform and reducing compliance costs. However, the simultaneous imposition of "legal responsibility" for accurate declarations and the threat of requiring refunds for untruthful declarations places a significant onus on enterprises. This indicates a shift in the regulatory burden from extensive pre-approval checks by authorities to rigorous post-audit verification. Consequently, businesses must invest in robust internal accounting and human resource systems to accurately track employee numbers (specifically those contributing to social insurance), revenue, and capital, and to maintain comprehensive supporting documentation. This mechanism, while fostering a more efficient system, demands a higher degree of internal diligence and accountability from enterprises.

IV. Applying for & Complying with Vietnam's SME CIT Exemption

The process for claiming the 3-year CIT exemption for SMEs under Resolution 198/2025/QH15 is designed to be largely automatic, based on the information provided during business registration.

Automatic Application Process for CIT Exemption

The CIT exemption for eligible SMEs is applied automatically based on the business registration data submitted by the company. This means that, unlike some other tax incentives, no separate, formal application specifically for this 3-year exemption is explicitly required.

Importance of Accurate Declaration at Registration

Given the automatic nature of the exemption, the accuracy of the information declared at the time of initial business registration is paramount. Companies are required to declare key data points such as their employee count (specifically those participating in social insurance), projected annual revenue, and charter capital. These figures are subsequently utilized by the business registration authorities and tax authorities to determine the enterprise's eligibility for SME status and, consequently, for the CIT exemption.

Required Documentation for Verification and Potential Audits

While a formal application for the exemption itself is not mandated, businesses are under a strict obligation to retain comprehensive supporting documentation. This includes, but is not limited to, financial statements, detailed payroll records (especially those pertaining to social insurance contributions), and records of total capital. Such documentation is crucial for substantiating the enterprise's SME classification and eligibility in the event of an inspection or audit by tax authorities. Tax authorities explicitly reserve the right to audit this information for verification purposes.

Annual CIT Filing Procedures for Exempt Entities

Even though an enterprise may be exempt from CIT for the first three years, it is still required to comply with annual CIT filing procedures. During the annual CIT finalization process, companies must declare their tax-exempt status based on their SME classification. General CIT filing obligations in Vietnam include preparing financial statements, accurately determining taxable income (even if it is zero due to the exemption), making quarterly provisional CIT payments (if applicable, though the exemption would likely negate this for the exempt period), and submitting the annual finalization return. Adherence to these procedural requirements for reporting income and formally claiming the exemption is essential for maintaining compliance.

The policy of automatic application of the CIT exemption, based on self-declared registration data, represents a strategic move by the Vietnamese government to reduce administrative friction and expedite the process for new businesses to access incentives. This approach marks a clear departure from more cumbersome pre-approval processes that often characterized previous incentive schemes. However, the accompanying emphasis on the enterprise's legal responsibility for accurate declarations and the explicit mention of potential audits, along with the necessity to retain supporting documentation, reveals a fundamental shift in the regulatory enforcement paradigm. Instead of rigorous upfront vetting, the system relies on post-compliance verification. This implies that while initial access to the exemption is straightforward, businesses must maintain impeccable records and be prepared to justify their SME status and eligibility at any time. This effectively transforms the administrative burden from a complex application process to one of ongoing, diligent compliance management.

V. Understanding Exclusions & Overlapping Vietnam Tax Incentives

Understanding the specific scope of the 3-year CIT exemption under Resolution 198/2025/QH15 requires distinguishing it from other tax incentives and recognizing potential limitations.

Distinguishing from Other Vietnam CIT Rates & Anti-Abuse Rules

Resolution 198/2025/QH15 specifically grants a 3-year CIT exemption for newly registered SMEs. This is distinct from other preferential CIT rates introduced by the Amended Law on Corporate Income Tax, which was passed on June 14, 2025, and is scheduled to take effect on October 1, 2025. This amended law introduces preferential rates of 15% and 17% for enterprises with annual revenues not exceeding VND 3 billion and VND 50 billion, respectively.

A crucial distinction lies in the anti-abuse safeguards. The preferential rates (15% and 17%) explicitly exclude subsidiaries or enterprises with related-party relationships to larger entities. This exclusion is a direct anti-abuse safeguard, designed to prevent the artificial fragmentation of businesses solely for the purpose of accessing SME-focused tax relief.

Regarding the 3-year CIT exemption under Resolution 198/2025/QH15, the available information indicates that the resolution "does not distinguish between domestic and foreign-invested businesses when applying the CIT exemption". This statement, when considered in isolation, might suggest that related-party exclusions do not apply to this specific 3-year exemption. However, the subsequent Amended CIT Law, which comes into effect later in 2025, introduces clear anti-abuse provisions by excluding subsidiaries and related parties from other preferential CIT rates. Given the government's stated intent to enhance the "integrity and effectiveness of tax incentives while supporting key developmental sectors" and to prevent "artificial fragmentation", it is highly probable that future implementing regulations will clarify or extend these anti-abuse provisions to encompass all SME-related CIT benefits, including the 3-year exemption. Businesses with complex ownership structures or those involved in related-party transactions should proactively monitor these forthcoming developments and seek professional advice to mitigate potential future compliance risks.

Distinction from Other Tax Incentives

Vietnam's tax incentive landscape is multifaceted, and the 3-year SME exemption should be understood in relation to other available benefits:

Innovative Startups: Innovative startups and organizations supporting innovation are eligible for a distinct incentive package. This includes a 2-year CIT exemption followed by a 50% reduction for the subsequent 4 years, specifically applicable to income derived from innovative startup activities. While an innovative startup may also qualify as an SME, these are separate incentive schemes with different eligibility criteria and durations.

General Investment Incentives: Beyond SME-specific benefits, Vietnam offers various other CIT incentives tied to encouraged sectors (e.g. high-tech industries, renewable energy, software development), encouraged locations (e.g. economically disadvantaged areas, high-tech zones), and project scale. These typically involve preferential tax rates (e.g. 10%, 17%) applied for extended periods, and/or tax holidays (e.g. 4 years of exemption followed by 9 years of 50% reduction). The 3-year SME exemption is a specific, broad-based incentive for new SMEs and should be considered alongside, but distinct from, these other targeted incentives. In instances where an SME qualifies for multiple incentives, the prevailing principle generally allows the enterprise to opt for the most beneficial support level.

VI. Strategic Advice for Foreign Investors: Maximizing Vietnam Tax Incentives

To effectively leverage the 3-year Corporate Income Tax (CIT) exemption under Resolution No. 198/2025/QH15 and navigate Vietnam's evolving tax landscape, businesses should adopt a strategic and proactive approach.

Maximizing Benefits and Ensuring Long-Term Compliance

Accurate Initial Registration: Given that the exemption is automatically applied based on business registration data, it is paramount to ensure that the initial Enterprise Registration Certificate (ERC) accurately reflects the enterprise's SME status in accordance with the detailed criteria outlined in Decree 80/2021/NĐ-CP. Any discrepancies at this stage could jeopardize eligibility.

Robust Record-Keeping: While a formal application for the exemption is not required, businesses must maintain meticulous financial statements, comprehensive payroll records (especially those detailing social insurance contributions), and accurate capital records. These documents are essential for substantiating the SME classification and eligibility in the event of an audit by tax authorities.

Monitoring SME Status: Enterprises should continuously monitor their employee count, revenue, and capital against the SME criteria. Although the initial 3-year exemption is fixed from the registration date, changes in business size in subsequent years could impact eligibility for other ongoing SME support policies.

Understanding Overlapping Incentives: If an enterprise also qualifies as an innovative startup or for other sector-specific or location-based incentives, a careful analysis should be conducted. The principle of allowing the enterprise to choose the "most beneficial" support level means that a strategic decision may be required to maximize overall tax advantages.

Importance of Expert Legal & Financial Consulting in Vietnam

Engaging with experienced legal and tax advisors early in the business setup process is crucial. This ensures full compliance with all conditions for the exemption and allows for strategic positioning of the enterprise to maximize available incentives. This guidance is particularly vital for foreign-invested enterprises navigating the complexities of Vietnamese regulations.

Businesses should develop a comprehensive long-term financial plan that extends beyond the initial 3-year tax break. The exemption provides significant short-term relief, but it is a limited-period incentive, and sustainable growth requires a strategy that accounts for future tax obligations.

Outlook on Future Policy Developments

The Vietnamese tax and business regulatory landscape is dynamic and subject to ongoing adjustments. Businesses should actively monitor the promulgation of detailed implementing regulations, especially concerning the interplay between Resolution 198/2025/QH15 and the recently Amended CIT Law. This is particularly relevant for potential clarifications regarding the application of related-party exclusions to the 3-year exemption. The broader trend indicates a governmental commitment to continuous reforms aimed at improving the business environment and attracting further investment. Staying informed about these developments will be key to long-term compliance and strategic advantage.

VII. Conclusion: Seizing Vietnam's SME Tax Opportunity

Resolution No. 198/2025/QH15 represents a significant and strategic initiative by the Vietnamese government to foster private sector growth through the provision of a 3-year Corporate Income Tax exemption for new Small and Medium-sized Enterprises. This policy, effective for enterprises granted their first Enterprise Registration Certificate on or after May 17, 2025, and meeting specific SME classification criteria, offers substantial financial relief during the critical startup phase.

Successful utilization of this incentive hinges on a clear understanding of the stringent "first Enterprise Registration Certificate" condition, which serves to target genuinely new business formations and prevent abuse through re-registrations or mergers. Equally important is a precise grasp of the detailed SME classification criteria outlined in Decree 80/2021/NĐ-CP, which vary by sector and size. While the exemption is automatically applied based on registration data, the emphasis on self-declaration places a significant responsibility on enterprises to maintain diligent compliance and robust record-keeping for potential post-registration audits.

The resolution underscores Vietnam's commitment to creating a more favorable and supportive ecosystem for new businesses, both domestic and foreign. It is part of a broader, multi-faceted governmental strategy that includes regulatory streamlining, financial support, land access, and innovation promotion. Navigating the intricacies of Vietnamese tax law and ensuring full compliance requires expert insight.

Contact Viettonkin Consulting today for a personalized consultation on how your new enterprise can maximize the 3-year Corporate Income Tax exemption and other strategic investment incentives in Vietnam.

On June 17, 2025, with the support of 94.56% of voting members, the National Assembly officially adopted a resolution to reduce the standard Value‑Added Tax (VAT) rate from 10% to 8%. This strategic adjustment aims to stimulate production and consumption, support businesses and households, and sustain Vietnam’s growth momentum through the second half of 2025 and into 2026. This guide unpacks the key points of the policy, outlines your compliance obligations, and answers frequently asked questions to ensure you’re fully prepared.

Key Highlights

VAT Rate Cut: 10% → 8%

Applicable Goods & Services: Those listed in Clause 3, Article 9 of VAT Law 48/2024/QH15 (e.g. manufacturing, retail, logistics, IT services).

Exceptions: Telecommunications; financial‑banking; securities; insurance; real estate; metal & mining products (except coal); special‑consumption goods/services (except gasoline).

Effective Period: July 1, 2025 – December 31, 2026.

Budget Impact: Estimated revenue loss of VND 39.54 trillion in H2 2025 and VND 82.2 trillion in 2026 (total VND 121.74 trillion).

1. Legal Basis

Resolution of the National Assembly: Adoption on June 17, 2025, to temporarily reduce the VAT rate.

VAT Law 48/2024/QH15: Specifies subjects and rates; Clause 3, Article 9 lists the goods/services now enjoying the reduced rate.

Previous Decree 180/2024/NĐ‑CP: Provided a similar 2% cut for January 1 – June 30, 2025.

2. Scope of Reduction

The recent resolution carefully delineates which goods and services see their VAT rate fall from 10% to 8%. In practice, this means most manufacturing, wholesale and retail activities—the very engines of everyday commerce—will benefit from the lighter burden. Transportation and logistics services, newly included in the list of eligible sectors, can now pass on cost savings to shippers and end‑users alike. Likewise, IT and software services join the reduction cohort, acknowledging the strategic role of Vietnam’s burgeoning tech industry. On the other hand, certain industries remain outside this preferential scope: telecommunications, financial‑banking services (including securities, insurance and related activities), real estate transactions, metal and mining products (with the sole exception of coal), plus a handful of special‑consumption goods and services. Notably, gasoline—a perennial fiscal lever—continues to enjoy the reduced rate, ensuring broad consumer impact.

Category

Previous Rate

New Rate

Notes

Manufacturing & Wholesale/Retail

10%

8%

Standard goods and services

Transportation & Logistics

10%

8%

Newly included in this resolution

IT & Software Services

10%

8%

Newly included

Telecommunications; Finance & Banks

10%

N/A

Not eligible for reduction

Real Estate

10%

N/A

Not eligible

Special‑Consumption Products

10%

8%

Exception: gasoline retains reduction

3. Implementation Timeline

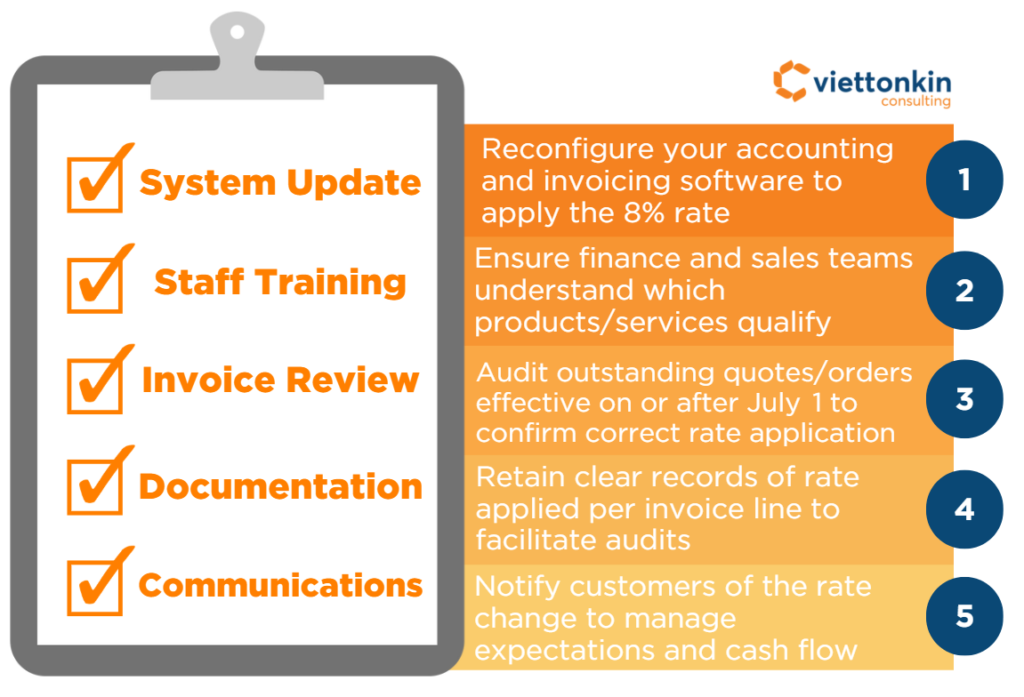

While policy changes often come with tight deadlines, this time, businesses are granted a welcome window to prepare. The new 8% VAT rate officially takes effect on July 1, 2025, and will apply through December 31, 2026. This gives companies several weeks—not just to react, but to prepare thoughtfully and thoroughly.

Between now and the effective date, businesses should begin by updating their accounting and invoicing systems to reflect the new rate. Equally important is ensuring that internal teams—especially finance and sales—understand how the changes apply in practice: which goods and services are eligible, and which remain at 10%.

It’s also wise to review any open quotes, contracts, or purchase orders that extend beyond July 1. If they still reflect the 10% rate where the 8% rate should apply, adjustments should be made in advance to avoid confusion—or worse, non-compliance.

We recommend treating this as an opportunity to get ahead, not just a deadline to meet. Taking early action can help your business avoid last-minute system issues, reduce operational disruption, and ensure that your compliance is smooth and stress-free when the new rate kicks in at midnight on June 30.

Action

Deadline/Date

National Assembly resolution takes effect

July 1, 2025

Period of reduced VAT rate

July 1, 2025 – Dec 31, 2026

Businesses must update billing and accounting systems

Before July 1, 2025

4. Impacts on Government Budget

Naturally, a reduction in VAT comes with fiscal implications. The government is projected to absorb an estimated revenue shortfall of VND 39.54 trillion in the second half of 2025, followed by an additional VND 82.2 trillion throughout 2026. In total, the cumulative impact on state revenue is expected to reach VND 121.74 trillion over the full course of the policy period.

However, this short-term budget impact is part of a broader economic strategy. By easing the tax burden on businesses and consumers, the government aims to stimulate production, consumption, and market demand, with the expectation that increased economic activity will help offset the losses through growth in other tax channels.

To support this approach, complementary measures are being implemented—most notably, tightened fiscal discipline, accelerated digitalization of tax administration (including the widespread use of e-invoices and certified cash registers), and strategic deployment of reserve funds to cover urgent and essential expenditures. These steps reflect a commitment to ensuring that the VAT reduction serves as both a stimulus and a sustainable component of broader fiscal planning.

Offset Measures:

Strengthening tax administration and digitization (e‑invoices via cash registers)

Tightening budget expenditure and leveraging reserves for urgent needs

Pursuing GDP growth of ≥ 8% in 2025 to generate offsetting revenue

5. Compliance Checklist

With the VAT reduction set to take effect on July 1, 2025, businesses have a valuable opportunity—not only to ensure compliance but also to align operations for maximum benefit. So, what should your next steps look like?

Start by updating your accounting and invoicing systems to apply the new 8% rate accurately. This technical update may seem straightforward, but implementing it early can help prevent costly errors down the line.

Next, we recommend conducting a focused training session with your finance and sales teams. Make sure your staff understands which goods and services are eligible for the reduced rate—and just as importantly, which are not. A clear internal understanding now can save time and mitigate risk later.

In parallel, carry out a quick review of all active contracts, quotations, and purchase orders. Any documents that stretch across July 1 and still reference the old 10% VAT should be updated promptly to reflect the new rate. These small administrative steps are key to avoiding regulatory issues or disputes with clients.

Don’t overlook documentation. Keep detailed records of how VAT was applied across your transactions, as this will be essential in the event of an audit. Proper recordkeeping remains one of the most effective safeguards against compliance concerns.

Finally, it’s important to communicate the change proactively to your customers and stakeholders. Clear, timely updates about pricing, invoicing, or billing changes will help manage expectations—and reinforce your professionalism in handling the transition.

Taken together, these actions will not only help your business meet regulatory requirements with confidence, but also position you to benefit fully from the cost efficiencies that the VAT reduction is intended to unlock.

6. Frequently Asked Questions

Q1: Do exempt activities (e.g. education, healthcare) need any adjustment? A1: No—services already exempt (0% rate) under VAT Law remain unchanged.

Q2: What if I mistakenly issue a 10% invoice after July 1? A2: You should issue a corrective invoice immediately, applying the 8% rate, to avoid penalties.

Q3: Are imports covered by this reduction? A3: Yes—imports subject to the standard 10% VAT rate now enjoy the 8% rate, barring exceptions.

Conclusion

The VAT rate reduction from 10% to 8% represents a timely “fiscal stimulus” designed to lower costs for businesses and consumers alike. While it entails a measurable impact on state revenues, the government’s accompanying measures aim to preserve budgetary balance and propel the economy toward robust growth. For businesses, the window from now until July 1 is crucial: update your systems, train your teams, and communicate changes clearly to ensure seamless compliance and maximize the benefits of this policy shift.

For tailored advice on how this VAT reduction affects your specific operations, contact the Viettonkin Legal Team today!

Vietnam is entering a new era of legal modernization. With the issuance of Resolution 66-NQ/TW by the Politburo on April 30, 2025, the country has laid out an ambitious roadmap to transform its legal system into one of the most transparent, efficient, and investor-friendly in Southeast Asia. For foreign direct investors (FDIs), this resolution signals a significant shift toward a more predictable and innovation-driven business environment.

A Vision for 2045: Legal Certainty in a High-Income Vietnam

Resolution 66 sets two major milestones:

By 2030: Vietnam aims to establish a synchronous, transparent, and enforceable legal system, removing regulatory bottlenecks and aligning laws with the three-tier government model.

By 2045: The country envisions a modern legal framework that meets international standards, supporting its goal of becoming a high-income, developed nation.

This long-term vision is not just aspirational—it is backed by concrete reforms that will directly impact how foreign businesses operate in Vietnam.

Key Reforms That Matter to Investors

1. A Transparent, Low-Compliance Legal Environment

Resolution 66 emphasizes the development of a socialist-oriented market economy with a legal system that is:

Open and transparent

Safe and predictable

Low in compliance costs

This means fewer bureaucratic hurdles, simplified administrative procedures, and a stronger legal foundation for property rights, freedom of contract, and equal treatment across all economic sectors.

2. Empowering the Private Sector

The resolution recognizes the private economy as the primary engine of growth. It calls for:

Legal mechanisms to ensure equal access to capital, land, and talent

Support for SMEs and startups

Promotion of regional and global private economic groups

For FDIs, this translates into a more level playing field and greater opportunities to partner with or invest in Vietnamese private enterprises.

3. Legal Frameworks for Emerging Sectors

Vietnam is preparing for the future by building legal corridors for:

Artificial Intelligence

Digital and green transformation

Data resource exploitation

Crypto assets

These frameworks will enable FDIs to explore new industries and innovative business models with legal clarity and protection.

4. International Integration and Legal Harmonization

Resolution 66 calls for improved international legal cooperation and alignment with global standards. This includes:

Enhanced legal predictability for cross-border transactions

Stronger enforcement of international agreements

Better dispute resolution mechanisms

This is especially relevant for investors seeking long-term stability and legal recourse in Vietnam.

Institutional and Technological Overhaul

To ensure effective implementation, the resolution introduces several institutional innovations:

A Central Steering Committee on Legal Reform, led by the General Secretary

A special financial mechanism to fund law-making and enforcement

Digital transformation of legal processes, including the use of AI and big data

These measures aim to streamline governance, reduce corruption, and accelerate policy responsiveness—all of which are critical for investor confidence.

Timelines and What to Expect

Year

Milestone

2025

Eliminate major legal bottlenecks

2027

Complete legal updates for the 3-level government model

2028

Finalize legal system for investment and business

2030

Achieve a transparent, enforceable legal system

2045

Reach international legal standards in a high-income Vietnam

Opportunities for Foreign Investors

With Resolution 66, Vietnam is not just reforming laws—it is redefining its investment climate. Key opportunities include:

Early entry into emerging sectors with supportive legal frameworks

Strategic partnerships with Vietnamese private firms

Participation in legal and institutional modernization projects

Increased protection for intellectual property and digital assets

Conclusion: A Legal Leap Forward

Resolution 66-NQ/TW is a bold declaration of Vietnam’s intent to become a top-tier investment destination in ASEAN. For foreign investors, it offers a rare combination of legal certainty, market dynamism, and forward-looking governance.

At Viettonkin Consulting, we are closely monitoring the implementation of these reforms and are ready to help you navigate the evolving legal landscape. Whether you're entering Vietnam for the first time or expanding your footprint, now is the time to align your strategy with Vietnam’s legal transformation.

Vietnam continues to demonstrate its commitment to legal modernization and transparency—key pillars for attracting and retaining foreign direct investment (FDI). The latest milestone in this journey is Resolution No. 59/2024/UBTVQH15, issued by the National Assembly Standing Committee on December 11, 2024. This resolution adjusts the 2025 Law- and Ordinance-Making Program, introducing new legislative priorities that directly impact the business and investment environment.

For foreign investors, understanding these legislative updates is essential to navigating Vietnam’s evolving regulatory landscape and identifying new opportunities.

What Is Resolution 59/2024/UBTVQH15?

Resolution 59 is a formal adjustment to Vietnam’s legislative agenda for 2025. It outlines the addition of several key draft laws and resolutions to be discussed and passed by the National Assembly. These additions reflect Vietnam’s strategic focus on legal clarity, digital governance, and economic modernization.

Key Legislative Additions for 2025

1. Extension of Agricultural Land Use Tax Exemption

What it is: A draft resolution to extend the duration of tax exemptions on agricultural land use, continuing the provisions of Resolution No. 55/2010/QH12.

Why it matters: This move supports Vietnam’s agricultural sector, which remains a critical part of the economy. For investors in agribusiness, food processing, and rural development, this signals continued government support and potential tax advantages.

2. Revised Law on Promulgation of Legal Documents

What it is: A revision of the Law on Promulgation of Legal Documents, aiming to streamline the legislative process, reduce legal inconsistencies, and improve transparency.

Why it matters: This reform aims to streamline the legislative process, reduce legal inconsistencies, and improve transparency. For FDIs, this means greater predictability and fewer regulatory surprises.

3. Draft Law on Personal Data Protection

What it is: A comprehensive legal framework to regulate the collection, processing, and storage of personal data.

Why it matters: This law is crucial for tech companies, e-commerce platforms, and any business handling customer data. It aligns Vietnam with global data protection standards (e.g., GDPR), enhancing trust and compliance for international investors.

4. Revised Press Law

What it is: An update to the existing Press Law to reflect the digital media landscape, providing clearer guidelines for media, advertising, and digital content businesses.

Why it matters: This could impact media, advertising, and digital content businesses, offering clearer guidelines and potentially more freedom for responsible communication and branding.

5. Revised Law on Bankruptcy

What it is: A modernization of Vietnam’s bankruptcy framework, aiming to enhance efficiency, fairness, and investor protection in business restructuring and insolvency proceedings.

Why it matters: A more efficient and fair bankruptcy process is essential for risk management, investor protection, and business restructuring. This reform will enhance Vietnam’s reputation as a safe and mature investment destination.

Implications for Foreign Direct Investors

✅ Improved Legal Certainty

The inclusion of these laws in the 2025 legislative agenda reflects Vietnam’s intent to harmonize its legal system with international standards. This reduces legal ambiguity and enhances investor confidence.

✅ Stronger Data Governance

The upcoming Personal Data Protection Law will provide a clear legal basis for data-driven businesses, helping foreign companies operate with confidence in Vietnam’s digital economy.

✅ Support for Innovation and Digital Economy

The revised Press Law and legal reforms around digital governance indicate a pro-business stance toward innovation, media, and technology sectors.

✅ Enhanced Risk Mitigation

With a modernized bankruptcy law, investors can expect better legal recourse and asset protection in the event of business failure or restructuring.

Timeline and Legislative Process

All the newly added laws and resolutions are scheduled for:

Discussion at the 9th session of the National Assembly (May 2025)

Passage at the 10th session (October 2025)

This timeline gives investors a clear window to prepare for compliance, engage with policymakers, or adjust business strategies accordingly.

Strategic Takeaways for Investors

Monitor Legal Developments: Stay updated on the progress of these draft laws to anticipate regulatory changes.

Engage Local Advisors: Work with legal and consulting firms like Viettonkin to interpret and implement new compliance requirements.

Leverage Incentives: Explore opportunities in agriculture, tech, and media where legal reforms may unlock new incentives or reduce barriers.

Plan for Data Compliance: Begin aligning your data practices with expected requirements under the new Personal Data Protection Law.

Conclusion: A More Predictable and Investor-Friendly Vietnam

Resolution 59/2024/UBTVQH15 is more than a procedural update—it’s a signal of Vietnam’s maturing legal infrastructure and its commitment to creating a transparent, innovation-friendly, and globally integrated business environment.

At Viettonkin Consulting, we are here to help you navigate these changes and seize the opportunities they bring. Whether you're entering Vietnam for the first time or expanding your operations, understanding the legal landscape is key to long-term success.

Vietnam is accelerating its transformation into a regional innovation powerhouse. With the issuance of Resolution No. 57-NQ/TW in December 2024, the country has committed to a bold, strategic overhaul of its science, technology, and innovation (STI) ecosystem. For foreign direct investors (FDIs), this resolution is more than a policy document—it’s a roadmap to a more dynamic, tech-driven, and globally integrated Vietnamese economy.

A National Strategy for Innovation and Digital Transformation

Resolution 57-NQ/TW outlines Vietnam’s vision to become a science- and technology-led nation by 2030, with a longer-term goal of achieving global competitiveness by 2045. The resolution is part of a broader national effort to:

Modernize the economy

Enhance productivity

Foster sustainable development

Strengthen national digital sovereignty

This strategic pivot is designed to attract high-quality investment, especially in sectors that align with Vietnam’s innovation priorities.

Key Goals and Timelines

Target Year

Strategic Milestone

By 2030

Vietnam becomes a developing country with modern industry and upper-middle income, driven by STI • R&D investment to reach 2% of GDP • Digital economy to contribute 30% of GDP • Top 3 in ASEAN for AI research and development • 100% of public services at level 4 available online • At least 70% of enterprises using digital platforms

By 2045

Vietnam becomes a developed, high-income country with a globally competitive innovation ecosystem • Top 30 globally in Global Innovation Index (GII) • At least 5 Vietnamese tech firms with regional/global influence • Digital economy contributes over 50% of GDP • Science and technology workforce accounts for 1.5% of total labor force

What Resolution 57-NQ/TW Means for Investors

1. A Favorable Legal and Policy Environment

The resolution mandates the removal of institutional bottlenecks and the creation of a synchronized legal framework for science, technology, and innovation. This includes:

Simplified procedures for technology transfer and licensing

Stronger intellectual property protection

Incentives for R&D investment and innovation hubs

For FDIs, this means lower compliance risks, greater legal clarity, and enhanced protection of proprietary technologies.

2. Strategic Investment in High-Tech Sectors

Vietnam is prioritizing investment in:

Semiconductors and microelectronics

Artificial intelligence and robotics

Biotechnology and pharmaceuticals

Green energy and environmental technologies

Digital platforms and cybersecurity

Foreign investors in these sectors can expect preferential policies, tax incentives, and access to national innovation programs.

3. Public-Private Partnerships and Global Integration

Resolution 57 encourages international cooperation and public-private partnerships (PPPs) to:

This opens the door for FDIs to collaborate with Vietnamese institutions, co-invest in innovation ecosystems, and scale regionally from a Vietnamese base.

4. Digital Transformation as a National Priority

Vietnam is embedding digital transformation across all sectors. The resolution supports:

Smart manufacturing and Industry 4.0

E-government and digital public services

Digital skills development and workforce upskilling

Investors in digital infrastructure, cloud services, fintech, and edtech will find a rapidly expanding market with strong government backing.

Institutional Reforms and Governance

To ensure effective implementation, the resolution proposes:

A centralized governance model for STI policy

Enhanced inter-ministerial coordination

A national innovation fund to support startups and R&D

These reforms aim to streamline decision-making, reduce bureaucratic delays, and ensure accountability—key concerns for foreign investors.

Opportunities for Foreign Direct Investors

FDIs can benefit from Resolution 57 in several ways:

Early-mover advantage in emerging sectors

Access to government-backed innovation zones

Participation in national digital transformation projects

Collaboration with Vietnamese universities and research institutes

Vietnam’s growing middle class, digital-savvy population, and strategic location in ASEAN further enhance its attractiveness as an innovation hub.

Challenges to Watch

While the resolution is ambitious, investors should be mindful of:

Implementation gaps at the local level

Talent shortages in high-tech fields

Regulatory adaptation to fast-evolving technologies

However, the government’s commitment to institutional reform, international cooperation, and human capital development suggests these challenges are being actively addressed.

Conclusion: A New Era for Investment in Vietnam

Resolution 57-NQ/TW marks a turning point in Vietnam’s development strategy. It signals a clear shift toward a knowledge-based economy, where science, technology, and innovation are central to national growth.

For foreign investors, this is a unique opportunity to align with Vietnam’s long-term vision, tap into a vibrant innovation ecosystem, and contribute to shaping the future of one of Asia’s most promising economies.

At Viettonkin Consulting, we are ready to help you navigate this evolving landscape—whether you're entering Vietnam for the first time or expanding your innovation footprint.

You may also like: Vietnam’s Resolution 66-NQ/TW: Legal Reform that Foreign Investors Can’t Ignore

Introduction

Vietnam is entering a pivotal phase in its economic transformation, guided by two landmark policy frameworks:Resolution No. 68-NQ/TWon private sector development and Resolution No. 57-NQ/TW on science, technology, innovation, and digital transformation.

This publication outlines the strategic goals, policy directions, and investment opportunities emerging from Resolution 68—offering foreign investors a clear roadmap to engage with Vietnam’s dynamic and evolving private economy.

I. Strategic Goals for 2030