Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Vietnam's food trade industry is one of the most dynamic sectors in the country. Fueled by an expanding middle class, rising disposable incomes, and shifting consumer preferences, the increasing demand for high-quality food products is undeniable. From bustling markets in Ho Chi Minh City to modern supermarkets in other major cities, the opportunity for both […]

Thinking of branching in Indonesia? Do you still need a guide to Indonesia Halal Certification? Worry not, we will give you a comprehensive guide of Indonesia Halal Certification below.

Recently, Indonesia’s House of Representatives announced that Halal certification will be mandatory. The requirement for halal certification for food, beverages, and slaughtered goods will take effect on October 18, 2024.

All food, beverage, and slaughter products circulating and traded in Indonesia need to comply with the general Halal certification process and the first phase will be implemented as of October 18, 2024.

To avoid confusion, you can still sell products without a Halal certificate for now. Alas, as a business decision, it would be unwise to go ahead with your products without the Halal label in the largest Muslim country in the world.

Starting off, you must know the concept of Halal itself. This concept serves as a guide for Muslims in all aspects of consumerism and consumption of products and services. Bound by Islamic dietary laws, Muslims ensure the permissibility of all foods and drinks before consumption.

There will usually be a Law that will regulate the processing, materials, and certification of Halal products, to establish partnerships with international Halal agencies.

In Indonesia, The Halal Law assigned the establishment of the Halal Products Certification Agency (BPJPH), a new government agency under the Ministry of Religious Affairs that will issue Halal certificates through a one-stop-shop system.

Key Takeaways

Acquiring Halal Certification determines whether a product complies with Islamic law (halal), or "haram," which contains pork or deviates from it.

Receiving Halal Certification allows companies to ensure that their products comply with the regulations and laws applicable in various markets. As the world's largest halal market, it will be wise to have Halal status on your business processes in Indonesia.

Halal certification also opens doors to markets in Malaysia, the Middle East, and other Muslim-majority countries.

What is Halal Certification in Indonesia?

For the largest Muslim country in the world, this certification is consequential as it is a way for the citizens to adhere to their religion.

According to a study by Hayyun Durrotul Faridah, Halal certification in Indonesia (Vol. 2 No. 2 (2019): Journal of Halal Product and Research (JHPR)), halal certification and halal labeling are two interrelated things.

Halal certification is a process to obtain a halal certificate by going through several stages of inspection to prove that the raw materials, production process, and halal product assurance system in a company are in accordance with the established standards (LPPOM MUI 2008).

Halal labeling is the inclusion of a halal label or logo on the packaging of halal products. This label serves to show consumers that the product is a halal product.

The process establishes if a product adheres to the Islamic law,” halal,” or if they contain pork or deviate from the Islamic law, “haram.”

Get to Know Indonesia’s Halal Body - Badan Penyelenggara Jaminan Produk Halal (BPJPH)

The government of Indonesia established an independent organization to manage Halal Certificates. It is called Badan Penyelenggara Jaminan Produk Halal (BPJPH).

BPJPH has several tasks including (1) Formulating and determining JPH policies (2) Determining norms, standards, procedures, and criteria for JPH (3) Issuing and revoking Halal Certificates and Halal Labels on Products (4) Registering Halal Certificates on foreign products (5) Conducting socialization, education, and publication of Halal Products (6) Accrediting LPH (7) Registering Halal Auditors (8) Supervising JPH (9) Providing guidance to Halal Auditors; and (10) Cooperating with domestic and foreign institutions in the field of JPH implementation (Article 6 of the JPH Law). BPJPH determines the logo or label that applies throughout Indonesia. In addition, it is also authorized to issue or revoke the halal logo.

Importance of Halal Certification for Products

In his book, Halal and Kosher Food (2023), Osman Ahmed Osman mentioned that “Halal food is very important to both Islamic and non-Islamic communities around the world for religious, cultural, ethical, and market reasons”

For Muslims, it is acceptable, and adhering to halal principles is a religious duty that guarantees the maintenance of their religious integrity through dietary decisions.

On the other side, for a business point of view, you can reach a wider customer target, especially if you are considering the demographic of Indonesians.

Halal Certification Compliance Period

Halal certification is not a one-time event but a cyclical process that requires renewal. The validity period of halal certification is only valid for 4 years.

Any product you want to sell with the "Halal" label needs to be certified as Halal in Indonesia. You should verify whether any Halal certificates you have received from other nations comply with Indonesian Halal requirements.

According to the Badan Penyelenggara Jaminan Produk Halal (BPJPH), as outlined in GovernmenFt Regulation No. 39 of 2021, the mandatory Halal Labeling Law will apply to food and beverages, cosmetics, drugs, restaurants, slaughterhouses, and other consumer goods.

The Halal certificate is available to importers, distributors, and producers alike.

Foreign businesses must first obtain Halal certification from an organization in their home countries if they want to export goods to Indonesia and need to obtain Halal certification.

Step-by-step overview of the obtaining halal certification:

Submitting applications by businesses.

Product & product facilitations inspection.

Review by religious organizations for compliance with Islamic law.

Issuance of the halal certificate.

3 Key Agencies Involved in Indonesia’s Halal Certification

BPJPH (Badan Penyelenggara Jaminan Produk Halal): Overview of its role in managing certification.

Majelis Ulama Indonesia (MUI): Its role in religious oversight and issuing fatwas.

Lembaga Pemeriksa Halal (LPH): Their role in conducting the technical audits.

Why is Indonesia Halal Certification Important for Businesses?

Halal standards compliance is a crucial component of compliance in many nations, particularly those with a majority of Muslims. By obtaining this certification, businesses may guarantee that their products adhere to the rules and legislation that are relevant in different markets.

Importance of Indonesian Halal Certification for Businesses

Access to the Indonesian market will become wider. As the world's largest halal market, it will be wise to have Halal label on your business processes.

Consumer trust and brand loyalty: By default, Halal-certified products are preferred by Muslim consumers.

Export opportunities: Not only can you explore the Indonesian market better, Halal certification opens doors to markets in Malaysia, the Middle East, and other Muslim-majority countries.

Legal requirements: Overview of Indonesia’s laws mandating halal certification (e.g., Law No. 33/2014).

What will happen if you don’t comply with Halal Certification?

If you are a business that intends to sell products with halal labels, failure to comply with Indonesia’s mandatory halal certification can lead to significant consequences for businesses. Under Government Regulation No. 39 of 2021, non-compliance results in a range of administrative sanctions. These include:

Written warnings: The first step for minor infractions or delays in certification.

Fines: Financial penalties may be imposed on businesses that fail to meet the requirements within the specified deadlines.

Product recalls: Non-compliant products may be removed from the market, which can severely impact revenue and brand reputation.

Revocation of halal certificates: For businesses that have previously obtained certification but fail to maintain standards, the certificate can be revoked, restricting their ability to market their products as halal.

Halal Certification: What is The Challenge & Solution for Businesses?

Challenges businesses facein the certification process:

Business will need cost and time involved in certification, which can be challenging to some. You will need to await the Ministry of Finance's implementing regulations on fee payment, which the BPJPH says will be dependent on the applicants’ type of products or services, and type of business. Business also needs to adapt production processes to meet halal standards.

So what is the solution and strategy to overcome these challenges? You can try to work with consultants. A consultant can help you to obtain Halal Certification.

Work with Viettonkin to Get Halal Certification Services

Do you need to obtain halal certification for your business?Viettonkin, a business consultant company with over 10 years of experience as a halal certification consultant is ready to assist you! Our team has personally guided numerous businesses through Indonesia's regulatory landscape, ensuring compliance with both local and international halal standards.

In the dynamic business landscape of Vietnam, labor disputes can present significant challenges to organizations of all sizes. The complexities surrounding labor disputes often stem from various factors, including differing interpretations of labor laws, cultural nuances, and evolving employment practices. These disputes can disrupt operations, damage employer-employee relationships, and result in financial losses.

At Viettonkin, we recognize the importance of resolvinglabor disputes swiftly and efficiently. With years of experience in providing dispute resolution services in Vietnam, we have developed a deep understanding of the local labor landscape andlegal framework. In this article, we explore common causes of labor disputes, the legal framework, and our approach to handling labor disputes in Vietnam.

Understanding labor disputes in Vietnam

Under Article 179, Clause 1 of the Labor Code 2019, labor disputes involve

a dispute over rights, obligations and interests among the parties during the establishment, execution or termination of labor relations;

a dispute between the representative organizations of employees;

a dispute over a relationship that is directly relevant to the labor relation.

Labor disputes are a common occurrence in Vietnam. In 2022, the whole country had 157 collective work stoppages stemming from labor disputes between enterprises and their employees (an increase of 50 compared to the same period in 2021) with a total number of over 102,540 workers participating.

Some issues that often lead to labor disputes in Vietnam are:

Benefits of the employee (salary, bonus, social insurance): These disputes are typically over unpaid wages, overtime pay, or bonuses.

Unilateral termination of labor contract: These disputes are typically over the unilateral termination of employment, the main point is whether the termination was justified or whether the employee was properly compensated in case the employer illegally terminates the labor contract.

Discrimination: These disputes are typically over discrimination on the basis of race, gender, religion, or other protected characteristics.

There are a number of ways to resolve labor disputes in Vietnam. These methods include:

Direct negotiations: This is the most common way to resolve labor disputes. In direct negotiations, the employer and employee or their representatives meet to try to reach an agreement.

Mediation: Mediation is a process where a neutral third party helps the employer and employee or their representatives reach an agreement.

Arbitration: Arbitration is a process where a neutral third party hears the case and makes a decision that is binding on both parties.

Court: The process of resolving disputes in court in front of a judge or court officials follows the procedures and legal provisions prescribed by law.

If compulsory mediation fails, the involved parties can opt for either a Labour Arbitration Committee or an authorized Court, but not both at the same time, and within 6 to 12 months. The procedure for establishing an Arbitration Committee takes around 7 to 30 days and involves three steps:

Submitting a dispute resolution request to the Labour Arbitration Committee,

Establishing a Labour Arbitration Board,

Making a final judgment to settle the labor disputes.

Labor disputes can have a significant impact on businesses in Vietnam, both financially and operationally. According to the Supreme People’s Court of Vietnam, the fee for settling labor disputes is variable, from only 9 USD to over 2000 USD depending on the dispute value. While a labor dispute case can last 6 months to arrive at a resolution under the method of mediation, it often takes 9 months to a year for a resolution in Court. Some of the most common impacts of labor disputes include:

Lost productivity: When employees are involved in a labor dispute, they are distracted from their work, leading to lost productivity and increased costs.

High legal fees: Businesses may have to pay for legal fees, mediation fees, or arbitration fees to resolve a labor dispute, which can be significant, especially for small businesses.

Damage to reputation: A labor dispute can damage a business's reputation if it is seen as being unfair to its employees. This can lead to lost customers and investors.

Increased turnover: Employees who are involved in a labor dispute may be more likely to leave their jobs, leading to increased turnover for businesses.

Labor disputes are a common occurrence in Vietnam. Source: Internet

Effective approaches for handling labor disputes in Vietnam

Resolving labor disputes requires a strategic and proactive approach. In Vietnam's dynamic business environment, understanding the most effective methods for handling labor disputes is essential.

Under Viettonkin’s perspectives, effective approaches involve clear communication, negotiation, and mediation. Open dialogue can often lead to mutually beneficial solutions, preserving employer-employee relationships. Mediation, facilitated by experienced professionals, provides a neutral platform for parties to discuss and find resolutions.

However, the latest Labor Code has specified six labor dispute cases that do not require mediation, unlike the Labor Code 2012:

Dismissal or unilateral termination of the labor contract;

Compensation for damage and allowance upon termination of the labor contract;

Disputes between domestic workers and their employers;

Disputes related to social insurance, health insurance, unemployment insurance, and insurance against occupational accidents and diseases as per the respective applicable laws of Vietnam;

Compensation for damage between employees being sent to work abroad under contracts and their company; and

Disputes between the outsourced employee and the outsourced employer.

Moreover, understanding the local culture and labor laws governing labor relations in Vietnam is crucial for employers. Compliance with regulations ensures a solid foundation for dispute resolution.

In collaboration with experienced legal professionals, Viettonkin offers guidance on adhering to the legal framework. Our expertise in labor dispute resolution services ensures that businesses meet the necessary legal requirements when addressing labor disputes in Vietnam. Through mediation, negotiation, and compliance with Vietnamese labor laws, we help businesses navigate complex situations and maintain a harmonious work environment.

Resolving labor disputes requires a strategic and proactive approach. Source: Internet

Practical advices in minimizing dispute resolution from Viettonkin

In prevalent practice, labor disputes result from various factors or reasons. When conflicts occur, first and foremost, the employer needs to double-check all personnel records and documentation pertaining to the employee in question and attempt to identify the root cause of the issues. Then a dialogue should be set up between the company and the employee in such a way that the issue is acknowledged, negotiations are made and both parties might reach an amicable agreement.

In case the direct negotiation between both parties fails, conciliation by labor conciliator or arbitration might be the next step. With over a decade of hands-on experience in the HR industry, Viettonkin has gathered some best practices that might be helpful to enterprises and investors doing business in Vietnam.

Consider the role of trade unions

If the company and its employees have agreed to establish a grassroots trade union, it is important to consider the role of the union when labor disputes arise. Employees may seek the opinion of the trade union prior to negotiating with the company regarding any disputes. By working effectively with trade unions, companies can build trust with their employees and promote a positive work environment.

Understand the role of trade unions before the establishment

Before establishing a trade union, companies should clearly understand the role of one. This can ensure that relevant agreements or documents are made between the trade union and the company. Understanding the role of a trade union can also help companies comply with the labor laws and regulations in Vietnam, which can ultimately enhance their reputation and legal compliance.

Consult with a labor lawyer or counsel

Consulting with a labor lawyer or counsel is essential for companies to prevent and resolve labor disputes. The labor laws and regulations in Vietnam are complex, and seeking legal guidance can help companies understand their legal rights and obligations. By developing effective strategies, companies can avoid disputes and potential legal or reputational damage.

Our clients benefit significantly from Viettonkin's labor dispute resolution services. Here are some key advantages:

Time and Cost Savings: Our efficient conflict resolution methods often lead to quicker resolutions, reducing legal expenses and minimizing operational disruptions.

Compliance with Regulations: Our in-depth knowledge of labor laws and HR regulations in Vietnam ensures that all resolutions align with legal requirements, mitigating future risks.

Tailored Solutions: We customize our approach to suit each client's unique needs, addressing the specific challenges they face.

Peace of Mind: Clients can focus on their core business activities while we handle the intricacies of labor dispute resolution.

These benefits demonstrate the value that Viettonkin brings to businesses handling labor disputes in Vietnam. Our client-centric approach set us apart in the field of conflict resolution.

In the dynamic business landscape of Vietnam, resolving labor disputes swiftly and effectively is paramount. Viettonkin stands as a trusted partner, offering specialized labor dispute resolution services tailored to your needs.

Our proven expertise and methods underscore our commitment to safeguarding your business interests. We understand the challenges you face, and our expertise in handling labor disputes in Vietnam ensures that you can navigate these challenges with confidence.Don't let labor disputes disrupt your operations or jeopardize your business. Contact Viettonkin today for expert assistance in resolvinglabor disputes in Vietnam, and experience the peace of mind that comes with having a dedicated and experienced partner by your side.

The Vietnamese government has recently approved and issued some policies about extension and reduction of the taxes for 2023, including continuing to apply the policy of 2% reduction in the value-added tax (VAT) on goods and services. The reduction to 8% VAT aims to stimulate economic growth and provide support to businesses.

In a recent development, the value-added tax (VAT) reduction policy has been implemented as per the Resolution No.101/2023/QH15 of the National Assembly and Decree No 44/2023/NĐ-CP, effective from July 1, 2023. This article aims to provide you with an important update on the eligibility criteria and proper implementation of the tax reduction within your business operations.

Summary of the Decree

The Decree No. 44/2023/NĐ-CP regulates the policy of value-added tax reduction in accordance with Resolution No. 101/2023/QH15 of the National Assembly. The value-added tax reduction applies to goods and services that currently have a tax rate of 10%, with some exceptions. The exceptions include industries such as telecommunications, financial activities, banking, securities, insurance, real estate, metals and prefabricated products, mining products (excluding coal mining), coke, oil refined mines, chemical products, and goods subject to excise tax. Information technology goods subject to the law on information technology are also eligible for the tax reduction.

The reduction in value-added tax is applied uniformly at all stages of import, production, processing, business, and trade. Coal products that are mined and sold are eligible for value-added tax reduction, but specific coal products listed in the decree are not eligible for tax reduction at stages other than mining and selling. Corporations and economic groups that implement a closed process before selling coal will also benefit from the tax reduction.

The Decree specifies the value-added tax reduction rates for businesses that calculate taxes by the deduction method and for businesses that calculate taxes based on a percentage of revenue. The implementation procedures are also outlined, including the requirements for issuing invoices and declaring taxes.

The Decree is effective from July 1st, 2023, until December 31st, 2023. Relevant ministries and agencies are responsible for propagating, guiding, inspecting, and supervising the implementation of the tax reduction. In case of difficulties, the Ministry of Finance will provide guidance and resolutions. Additionally, we at Viettonkin Consulting are ready to assist your company in this transition. Contact us now!

Eligibility and VAT Rate

Eligibility on goods and services made before July 1st:

The Decree specifies the value-added tax reduction policy for goods and services that are currently subject to a tax rate of 10%. However, the eligibility for tax reduction varies depending on the industry and the specific goods and services. The industries eligible for tax reduction include telecommunications, financial activities, banking, securities, insurance, real estate, metals and prefabricated products, mining products (excluding coal mining), coke, oil refined mines, and chemical products. Goods subject to excise tax and information technology goods subject to the law on information technology are also eligible.

The specific goods and services eligible for tax reduction are listed in appendices issued with the Decree. It is important to refer to the appendices (Appendix I, Appendix II, and Appendix III) for a detailed list of eligible goods and services.

Goods and services listed in the appendices that are not subject to value-added tax or are subject to a 5% tax rate as per the Value-added Tax Law will not be eligible for the tax reduction. The provisions of the Value-added Tax Law will apply in such cases.

For businesses calculating value-added tax by the deduction method, the tax rate to be applied for eligible goods and services is 8%. The Decree No 44/2023/NĐ-CP specifies that CNSVN and CNTVN are subject to the VAT rate of 8% from July 1, 2023, to December 31, 2023. It is essential to ensure that invoices for selling goods or providing services belonging to eligible categories are issued on time and within the effective period of Resolution No.101/2023/QH15.

The infographic below will help you better understand the processes and regulations of the Decree.

Important Considerations

While the tax reduction policy aims to simplify the VAT calculation process, it is important to note that certain situations may arise that require additional attention. To assist you in understanding these situations, we have provided the following hypothetical scenarios and their corresponding VAT rates:

1. Service provided in June 2023 but accepted, handed over to clients in June 2023 and issued sales invoices in July 2023:

VAT Rate: 10%

Explanation: According to regulations, the time of invoice issuance for service provision is the time when the service is completed, regardless of whether money has been collected or not. Issuing invoices in July for services provided in June would be considered incorrect, leading to potential fines. Please refer to the relevant legal basis mentioned in the email for detailed information.

2. The service is provided in June 2023 but handed over to the customer in July 2023 and a sales invoice is issued in July 2023:

VAT Rate: 8%

Explanation: Since the service is completed in July, the VAT rate of 8% will be applied in this scenario.

3. The contract was signed before July 1, 2023, with the VAT rate of 10%. Handing over services to customers when completed after July 1, 2023:

VAT Rate: 8%

Explanation: If the service is completed and the invoice is issued in July, the reduced VAT rate of 8% will be applicable, regardless of the VAT rate stated in the contract signed before July 1, 2023.

Guidance and Updates

As the Decree 44 has recently been issued, specific guiding documents and official dispatches from tax authorities for various cases have not been released yet. It is important to stay updated with the latest guidance on VAT reduction in 2023. The responsible authorities will provide additional instructions during the application process, ensuring clarity and compliance with the tax reduction policy.

Conclusion

Understanding the eligibility criteria and proper implementation of the VAT reduction policy is crucial for businesses. By following the guidelines outlined in the Resolution No.101/2023/QH15, Decree No 44/2023/NĐ-CP, and the relevant legal basis, you can ensure the correct application of VAT rates for eligible goods and services. Stay informed about any updates and seek clarification from the authorities if needed to streamline the implementation process effectively. Contact us now for further assistance on taxations and subscribe to our newsletter to stay up-to-date on the VAT reduction.

Company dissolution in Vietnam is a multifaceted process that demands careful attention to legal requirements and meticulous planning. In Vietnam, understanding the process and legal requirements for dissolving a company is crucial to ensure a smooth and legally compliant exit strategy. This blog article aims to shed light on the intricacies of company dissolution in Vietnam, providing entrepreneurs, business owners, and investors with valuable insights and guidance throughout this complex procedure.

Cases of Company Dissolution in Vietnam

Company dissolution in Vietnam is a procedure that marks the culmination of a business entity, ensuring the settlement of debts and financial obligations. Governed by the Law on Enterprises (LOE), this process encompasses voluntary and compulsory dissolution scenarios, each with distinct parameters and consequences.

Voluntary Dissolution

Voluntary dissolution, as the name suggests, occurs when company owners make a conscious decision to terminate operations. Voluntary dissolution is possible in the following cases:

The stated operating period in the company's charter expires, and the owners choose not to extend it further.

The owners discontinued their business endeavors due to the recognition of the company's inefficiency.

Compulsory Dissolution

On the other hand, compulsory dissolution arises when competent state agencies intervene due to non-compliance with legal provisions. This may transpire when a company violates established regulations, leading to the mandated cessation of all business activities. Furthermore, compulsory dissolution can be enforced if the company fails to meet the minimum requirement for company members or shareholders and cannot rectify the shortfall by adding additional members within a period of time.

How to Dissolve a Company in Vietnam

In response to prevailing challenges, such as the global economic downturn, the impact of the epidemic or political upheaval, foreign investors may choose to embark on business restructuring plans, which entail the cessation and closure of their invested entities in Vietnam. However, it is crucial to recognize that the liquidation process for a Vietnamese company can be a complex and resource-intensive endeavor, accompanied by substantial implications of tax and regulatory. To navigate this intricate landscape successfully, foreign investors must possess a comprehensive understanding of the conditions and procedures mandated by Vietnamese law before embarking on the journey of dissolving their company.

Conditions for Dissolution of a Company

Pursuant to the provisions of Article 207 of the Enterprise Law 2020, a company in Vietnam can only be dissolved when one of the below circumstances occurs:

Conditions for company dissolution

(1) Completion of Operation Term

When the specified operational duration, as stated in the company's charter, comes to an end without a decision to extend it.

(2) Resolutions and Decisions

Dissolution may occur based on resolutions and decisions made by the business owner, Members' Council (for partnerships and limited liability companies), or the General Meeting of Shareholders (for joint-stock companies).

(3) Insufficient Membership

If the company fails to meet the minimum number of members prescribed by the Law within six consecutive months and neglects to undergo the necessary procedures for transforming its enterprise type, dissolution becomes a legal recourse.

(4) Revocation of Enterprise Registration

In cases where the certificate of enterprise registration is revoked, unless otherwise specified by the Law on Tax Administration, dissolution becomes an inevitable consequence.

However, it's important to note that dissolution can only proceed once the company ensures the complete settlement of debts and other property obligations. Business owners cannot dissolve their companies during ongoing dispute settlement processes at court or arbitration. In the event of an enterprise registration certificate revocation, both the concerned manager and the enterprise bear joint responsibility for the outstanding debts.

Dissolution Procedure

Below is a step-by-step breakdown of the dissolution procedure:

Company dissolution procedure

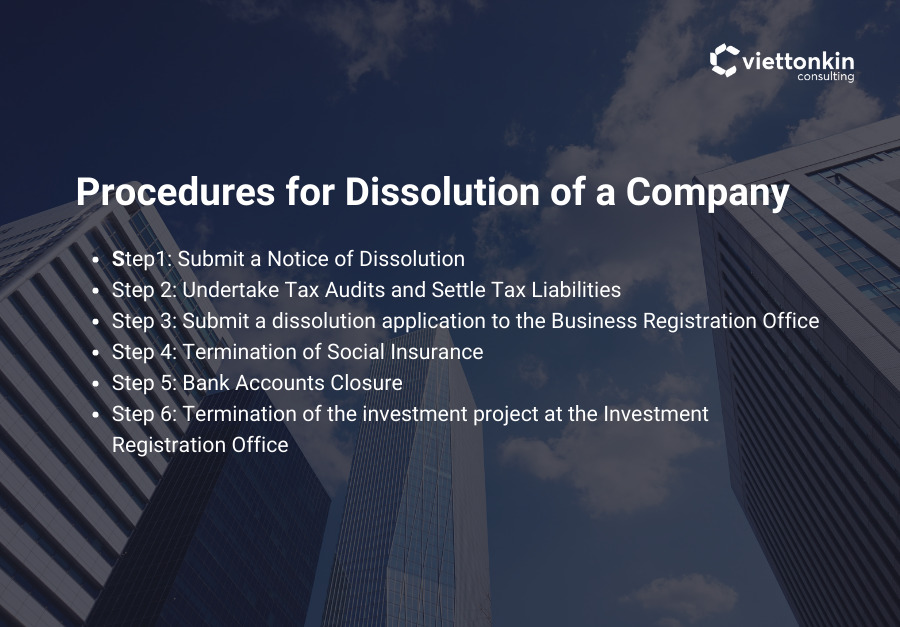

Step 1: Submit a Notice of Dissolution

The initial step requires the company to submit a formal notification of dissolution together with the decision on the enterprise to the business registration office in the city or province where it is headquartered. Once the notice is submitted, the enterprise's legal status on the National Business Registration Portal will be changed to " undergo dissolution procedures." The information regarding the enterprise's dissolution is also relayed to the tax authority by the Business Registration Office.

Step 2: Undertake Tax Audits and Settle Tax Liabilities

In this critical phase, the company must undergo tax audits and fulfill any outstanding tax obligations with the tax authorities. Important documents include a written request to invalidate the tax code, a decision on the dissolution of the enterprise, and documents related to the tax obligations of the enterprise as required by the tax authorities. The duration of this process depends on the complexity and level of compliance, typically ranging from 3 to 12 months.

Step 3: Submit a dissolution application to the Business Registration Office

Within five working days of receiving the application for registration of dissolution, the Business Registration Office updates the legal status of the enterprise in the National Enterprise Registration Database to the “dissolved”. Simultaneously, the office also issues an official notice of the enterprise's dissolution. During this step, it is crucial to comply with any requirements and not encounter objections from relevant parties to proceed smoothly.

Step 4: Termination of Social Insurance

Closing the social insurance books is a vital procedure to conclude the payment of social insurance premiums for employees. Employers must follow the prescribed steps, including issuing a labor reduction notice and providing the necessary documents such as the social insurance book and the decision to terminate the labor contract, as outlined in Decision 595/QD-BHXH.

Step 5: Bank Accounts Closure

After receiving the notification of the enterprise's dissolution status update on the National Enterprise Registration database, the company can proceed to close its bank accounts. For more information, enterprises are required to work together with the bank to carry out the required procedures. In case there is not any bank account opened, a letter of commitment confirming the absence of debts with any banks may be required.

Step 6: Termination of the investment project at the Investment Registration Office

As the final step, once all debts and dissolution costs are settled, the FDI company must file an application dossier to terminate the investment project with the licensing authority, typically the Department of Planning and Investment. If no objections or concerns from relevant parties are raised, the licensing authority will confirm the termination of the investment project.

Conclusion

Navigating the intricacies of company dissolution in Vietnam is no easy feat. As this blog article has highlighted, understanding the legal framework, complying with regulatory requirements, and addressing various aspects such as assets, liabilities, employees, and taxation are crucial for a successful dissolution process. However, the complexities involved may still present challenges to even the most experienced entrepreneurs and investors.

To ensure a seamless and efficient dissolution process, it is highly recommended to seek professional guidance and assistance. Whether you are an entrepreneur closing down a business, an investor restructuring your portfolio, or a company facing bankruptcy, Viettonkin's consulting service can help you navigate the dissolution process with efficiency, ensuring legal compliance and minimizing potential risks.

Don't leave the dissolution of your company to chance. Call upon the expertise of Viettonkin's consulting service and embark on a successful investment journey in Vietnam. Contact us today to discuss your specific needs and take the first step toward a smooth and legally compliant company dissolution process.

In response to the outbreak of the Covid-19 pandemic, the Vietnamese government acted swiftly to implement a range of favorable measures, such as tax reductions and extensions to support businesses impacted by the crisis and stimulate the recovery of the domestic economy. As Vietnam moves into the mid-year of 2023, the government has already approved a comprehensive tax reduction and extension policy, reflecting their commitment to sustaining economic stability and facilitating the growth of businesses in the country.

Tax Reduction Policy

On May 17, 2023, the National Assembly Standing Committee issued Notice No. 2298/TB-TTKQH, providing important information regarding the VAT reduction policy in Vietnam. According to the notice, the VAT reduction policy will be implemented from July 1st, 2023 to December 31, 2023, based on Resolution No. 43/2022/QH15.

However, it is important to understand the eligibility criteria for this VAT reduction. The notice clarifies that certain goods and services will be exempt from the VAT reduction. These include telecommunications, financial activities, banking, securities, insurance, real estate trading, metals, and prefabricated metal products, mining products (excluding coal mining), coke, refined petroleum, chemical products, products, and services subject to excise tax, and information technology in accordance with the law on information technology.

Additionally, a 20% reduction in the VAT calculation percentage will be implemented for business establishments, including business households and individuals, when issuing invoices for goods and services subject to a 10% VAT liability.

The objective of this plan is to strategically boost consumption demand in alignment with the current economic landscape, thereby revitalizing and fostering the prompt recovery and development of production and business activities, ultimately benefiting our nation's economy

Ho Duc Phuc, Minister of Finance.

The government anticipates a reduction in state budget revenue of approximately 5.8 trillion VND per month. If implemented during the final six months of the year, this reduction would amount to around 35 trillion VND. However, the policy's impact will extend beyond revenue reduction. By lowering the cost of goods and services, it will stimulate production and business activities, generating more job opportunities and contributing to both macroeconomic stability and regional economic recovery in 2023.

Financial experts widely recognize the significance of this VAT reduction policy for businesses and individuals, especially given the challenging business landscape experienced in the first quarter of 2023.

VAT is embedded in the price structure, and a 2% reduction in VAT will not only decrease the selling price of goods and services but also stimulate consumption, thereby assisting businesses in increasing their sales volume. Furthermore, for manufacturing enterprises reliant on input materials, VAT reduction will effectively reduce input costs, thereby igniting production

A representative of the Vietnam Tax Consultants Association.

2023 Tax Extension Regulations

Together with the tax reduction policy, the implementation of tax extension is crucial in boosting business activities and triggering purchasing demand within the domestic market.

Who Qualifies for the New Tax Extensions?

In accordance with Article 3, Decree 12/2023/NĐ-CP, there are 4 major categories of taxpayers that are eligible under the new tax extension regulation, including manufacturing enterprises, enterprises in specific economic sectors, industry product manufacturers and key mechanical product producers, small and micro-enterprises.

Manufacturing Enterprises: This category encompasses a wide range of industries, including agriculture, forestry, fishery, production, construction, and crude oil extraction (excluding corporate income tax on crude oil, condensate, and natural gas collected under agreements or contracts). Manufacturing enterprises within these sectors can take advantage of the tax extension policy to alleviate financial burdens and enhance their competitiveness.

Enterprises in Specific Economic Sectors: Businesses operating in sectors such as transport, warehousing, labor, and employment services can also reap the rewards of the tax extension policy. These sectors play a crucial role in supporting the overall economy, and by extending their tax obligations, the policy enables them to allocate resources more efficiently and fuel their growth.

Supporting Industry Product Manufacturers and Key Mechanical Product Producers: Supporting Industry Product Manufacturers and Key Mechanical Product Producers: Enterprises, organizations, households, business households, and individuals involved in the production of supporting industry products prioritized for development and key mechanical products are given special consideration.

Small and Micro-Enterprises: Small and micro-enterprises operating in the commerce and services sectors, employing no more than 10 laborers with an average annual contribution and having a total revenue not exceeding 10 billion VND or total capital not exceeding 3 billion VND, fall under this category. The tax extension policy aims to support these businesses, which form the backbone of the economy, by reducing their tax burden and fostering a favorable environment for their growth and prosperity.

As Vietnam strides confidently towards a brighter future, these tax extensions serve as catalysts of progress. Through the government's visionary approach, a tapestry of industries now thrives, each endowed with its unique potential. The journey ahead beckons with promise and possibility, as enterprises embark on a transformative path, fostering economic prosperity and igniting the nation's spirit of innovation.

Terms and Conditions

The new tax extension policy introduces specific rules to facilitate the payment of value-added tax (VAT) and corporate income tax (CIT). Here are the key rules that taxpayers should be aware of:

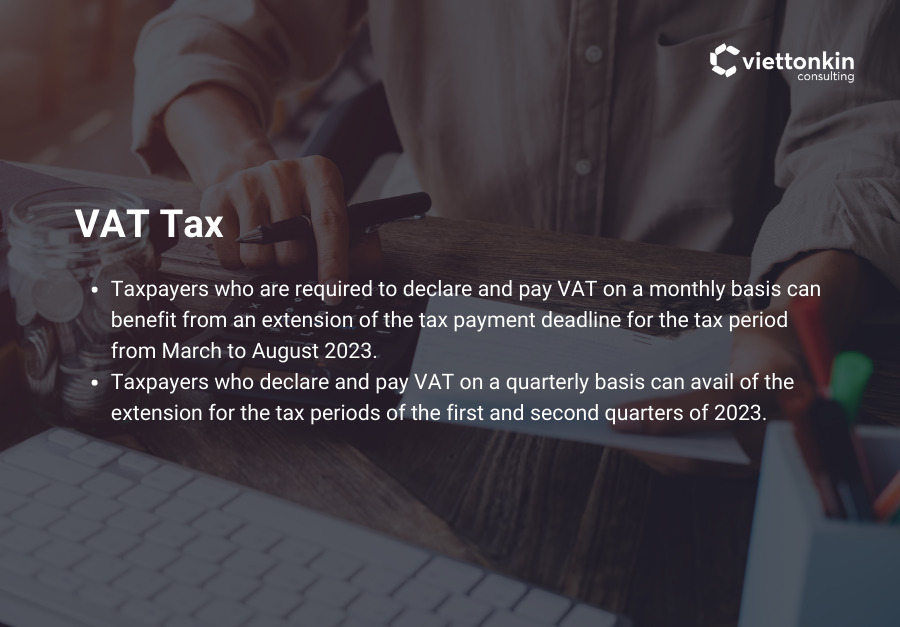

VAT Tax:

Taxpayers who are required to declare and pay VAT on a monthly basis can benefit from an extension of the tax payment deadline for the tax period from March to August 2023.

Taxpayers who declare and pay VAT on a quarterly basis can avail of the extension for the tax periods of the first and second quarters of 2023.

Conditions of VAT extension

Extension Period for VAT:

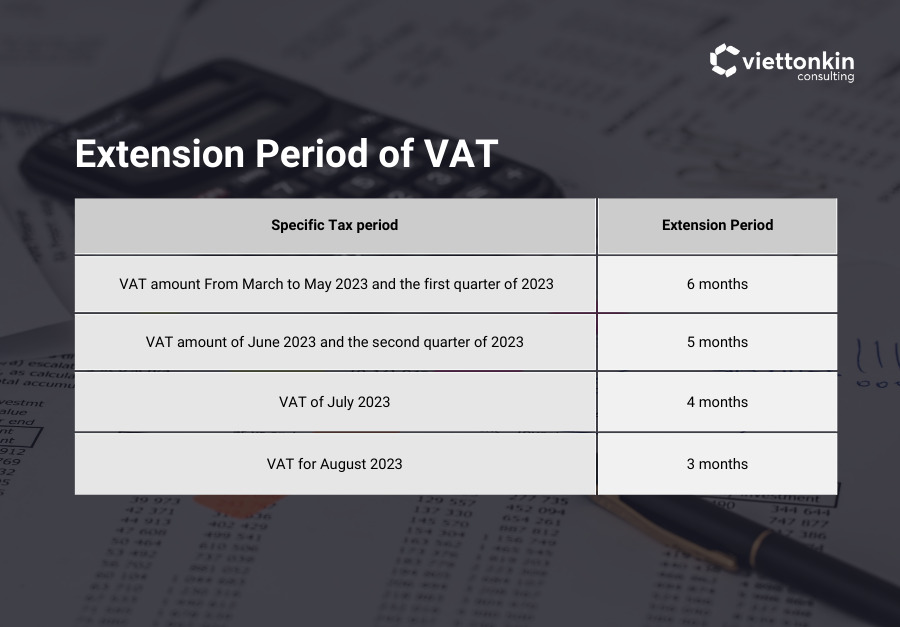

The extension period for VAT payments varies depending on the specific tax period:

For the value-added tax amounts from March to May 2023 and the first quarter of 2023, the extension period is 6 months.

For the value-added tax amount of June 2023 and the second quarter of 2023, the extension period is 5 months.

For the value-added tax amount of July 2023, the extension period is 4 months, and for August 2023, the extension period is 3 months.

VAT Extension Period

CIT:

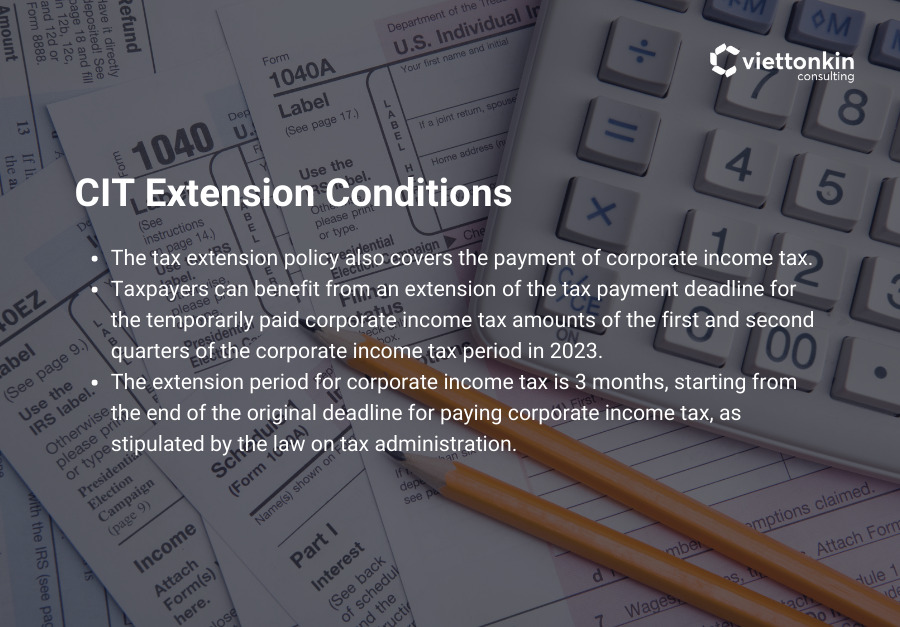

The tax extension policy also covers the payment of corporate income tax.

Taxpayers can benefit from an extension of the tax payment deadline for the temporarily paid corporate income tax amounts of the first and second quarters of the corporate income tax period in 2023.

The extension period for corporate income tax is 3 months, starting from the end of the original deadline for paying corporate income tax, as stipulated by the law on tax administration.

CIT Extension Conditions

How to File for a Tax Extension

During the process of filing for a tax extension, taxpayers must be aware of important notes to ensure compliance and avoid any potential issues. Here are the key points to keep in mind:

Submission of Extension Application: Taxpayers must complete and submit an application form for extension to the managing tax authority. This application should cover the entire tax amount incurred during the tax-extended period. The application form should be submitted concurrently with the monthly or quarterly tax returns, following the regulations stipulated in the tax administration law.

Deadline for Application Submission: If the extension application is not submitted simultaneously with the monthly or quarterly tax returns, taxpayers have until September 30, 2023, to submit the application. It is important to adhere to this deadline to ensure eligibility for the tax payment extension.

Responsibility of Taxpayers: Taxpayers are responsible for determining and ensuring that their extension requests fulfill the criteria specified in the decree. If the taxpayer submits the extension request to the tax authority after September 30, 2023, the tax payment extension will not be granted.

Notification of Acceptance: Tax authorities are not obligated to notify taxpayers regarding the acceptance of their tax payment extension request. It is the responsibility of the taxpayers to make the extension request and keep track of its status.

Notification of Ineligibility: If, during the extension period, the tax authority determines that a taxpayer is not eligible for the extension, they will send a written notice to the taxpayer, explaining the decision.

Post-Extension Verification: Following the expiration of the extension period, if a competent state agency conducts an inspection and determines that the taxpayer was not eligible for the extension as outlined in the decree, the taxpayer must settle the outstanding tax amount, along with fines and late payment interest, to the state budget.

Being aware of these important notes, taxpayers can ensure compliance throughout the tax extension process. It is crucial to adhere to the deadlines, maintain accurate records, and take responsibility for submitting the extension request on time. This will help prevent any potential complications and allow for a smooth and compliant tax filing experience.

Tax Reduction & Extension Policy Impact on Vietnam’s Economy

In 2022, with the introduction of tax reduction and extension policy, Vietnam’s economy has witnessed an impressive recovery. This strategic intervention, implemented with precision and directed towards the right sectors focused on the right sectors, led to an astounding 15% increase in enterprise investment capital compared to the previous year. The ripple effect was felt across the board, with a staggering 20% surge in total retail sales of consumer goods and services, and an impressive 9.5% growth in people's incomes.

On April 17, 2023, the esteemed state-owned publication agency, Investment Newspaper, expressed its unequivocal stance on the matter: the impact of tax extension, exemption, and reduction policies has been too significant to overlook. Hence, it is crucial to continue implementing these policies without delay. The urgency stems from the fact that difficulties have surfaced and become increasingly apparent since the fourth quarter of 2022. According to a recent statistical survey conducted by the General Statistics Office, a staggering 52.4% of businesses are grappling with challenges stemming from sluggish domestic demand. Among them, over 30% face financial hurdles, while 37% struggle due to borrowing capital from banks burdened with exorbitant interest rates.

Given this complex landscape, the proactive implementation of business support policies, particularly through tax reduction and extension, starting from the beginning of 2023, serves as a timely and critical intervention. By doing so, Vietnam can effectively contain the spread of these challenges and propel the recovery of the domestic economy within the post-Covid-19 context. Not only will this mitigate the global recessionary impact, but it will also lay the foundation for sustained economic growth, providing a favorable environment for businesses to thrive.

Final Thoughts

By reducing the VAT rate and extending tax benefits to specific sectors, the government aims to promote consumption, boost production, and create more job opportunities. However, navigating the intricacies of tax regulations and ensuring compliance can be challenging for businesses and investors. That's where Viettonkin's legal consulting services come into play. Our team of experienced professionals can provide expert guidance and support, helping businesses understand the nuances of the tax extension policy and assisting them in avoiding any legal violations.

Don't let the complexities of tax regulations hinder your business growth. With us by your side, you can navigate the tax landscape with confidence and focus on what matters most—growing your business in the dynamic market of Vietnam.

Contact Viettonkin today and embrace the full potential of your business.

Viet Nam has emerged as a rising star in the region and an attractive destination for foreign investment. However, besides the achievements that FDI projects bring to the country, there are persisting problems such as price transfer, tax evasion, environmental pollution, technology transfer and so on.

Therefore, the Vietnamese government is increasingly paying attention to the due diligence process and screening whether the foreign projects can meet its requirements. With that being said, this process can be the hindrance to any investors attempting to make a market entry to Vietnam. Any gap or misunderstanding in knowledge of Vietnam’s FDI screening framework can threaten a successful entrance to the country.

To narrow this gap, Viettonkin Consulting’s strategic due diligence offers foreign investors the most exhaustive insight into Vietnam’s FDI screening procedure to secure a favorable project.

Vietnam’s FDI projects selection tendency

Before deciding whether to approve or reject the investment application, the host government must critically examine the core components of an FDI project to assess its reasonableness, level of effectiveness, and practicality. Investors and investment projects are evaluated based on their legal status, financial capacity, level of relevance to overall planning, technological and technical relevance, and anticipated economic and social repercussions.

However, to guarantee the project’s success as well as to optimize the host country’s benefits, the Vietnam government has set out its priority to certain criteria of the FDI selection process. A new FDI plan for 2018–2023 is being developed by Vietnam's Ministry of Planning and Investment with the help of the World Bank, with an emphasis on priority industries and high-quality rather than quantity of investments. Instead of labor-intensive industries, the new draft wants to promote foreign investment in high-tech businesses.

The draft prioritizes FDI investments on a short-term and medium-term basis. The draft gives short- and medium-term FDI investments priority. Industries with few chances for competition will be given priority in the near future, including:

Manufacturing/Production – Automotive and transport equipment OEMs and suppliers;

Environmental-friendly technology – Water conservation, Solar, Wind investments.

In the long-term, the emphasis is on industries that prioritize skill development, such as:

Manufacturing – Manufacturing of pharmaceuticals and medical equipment;

Services – Services include education and health services, financial services, and financial technology (Fintech);

Information technology and intellectual services.

In addition to priority sectors, the country also rejects FDI proposals in industries including oil refineries, cement, and steel-and-iron manufacturing in order for Vietnam to achieve its goals for green growth.

Due diligence process for foreign investment projects

The general process involves basic components such as the following:

Eligibility assessment: The first FISI component lays forth key requirements that any investor thinking about conducting business in Vietnam must meet and support during the project appraisal process. According to Vietnam's investment law, the requirements were created. The eligibility assessment covers a range of issues from basic information such as location, business line, Central Product Classification (CPC) code to other mandatory questions such as:

Is the investor independent from a foreign government (not a government-owned or government-controlled entity)?

Is the proposed investment project appropriate with land use plans already approved by the local government?

Is the plan for site clearance and resettlement appropriate with the laws, regulations and local land use planning?

Risk assessment: The second part evaluates risks associated with the investment project and determines whether mitigation solutions are appropriate. To give local authorities a thorough understanding of the investor and the project, the risk evaluation of investment projects is required. The risk assessment generally includes economic risks, social risks and environmental risks such as the following questions are to ask:

Does the history or current portfolio of the investor demonstrate that this investor has experience in the proposed business activity or project?

Is the investor able to show proof of healthy business financial capacity?

Has the investor ever been reported for non-compliance with labor regulations, health and safety regulations, land and property regulations, consumer regulations, privacy regulations, anti-corruption and anti-bribery regulations or any other laws that regulate social impacts in Vietnam or other countries?

Has the investor ever been reported for non-compliance with environmental regulations.

Alignment assessment: The third element looks at the project's compatibility with both worldwide norms for responsible investment and local government priorities for attracting investment. Investors are not required to meet these standards, however, investors are urged to adhere to these requirements to guarantee that their investment in Vietnam supports sustainable development and avoids or lessens negative effects on people and the environment. If these criteria are met, it shows that the investor is making a responsible investment. The project may be eligible for local government incentives and support for FDI initiatives due to its potential to significantly advance local sustainable development. The alignment assessment also looks into 3 main criteria: economic dimension, social dimension and environmental dimension, some of the questions can be:

Is there a specific plan in place for the project to prioritize recruiting residents from the commune/ward in which it is located?

Will any technology in a form of sharing production specifications and quality control methodology be transferred to local suppliers?

Will the investor respect international labor standards on working hours, rest times, sick leave and paid leave?

Will the investor have processes to effectively monitor, prevent, mitigate and remediate air, water, land and soil pollution?

This structure is about recognizing and mitigating current and potential negative effects that may be brought on by specific foreign investment projects without decreasing Vietnam's openness to foreign investment or limiting the operations of foreign investors in Vietnam. Knowing this, investors can have exhaustive insights into what should be prepared and hence overcome the due diligence process efficiently. The full set of questions and criteria and be found here.

Viettonkin can help you benefit from strong due diligence capabilities

Fast and precise

Due diligence can be a time-consuming and arduous process. Viettonkin Consulting provides foreign investors with an optimized due diligence process which is both speedy and relevant.

Our consulting is efficient with the use of diligence management tools and softwares, allowing data to be stored securely while also effectively managed and shared. By utilizing an organized due diligence checklist, Viettonkin can find out about a project’s resources, liabilities, contracts, benefits and potential issues within no time.

With an understanding that each acquisition is unique, our toolkit is flexible and can be changed to fit different situations. Moreover, our team always addresses possible risks and bottlenecks as soon as they are identified during diligence.

Save time and money

Due diligence is a lengthy, costly and intimidating process that involves multiple parties and phases. It may seem difficult to project how long the process lasts for it to be enough and exhaustive. Even if it is thorough, the due diligence procedure should only take 30 to 60 days, which is achievable if delegated to an efficient and dynamic team. The Viettonkin team is composed of experts with experience performing due diligence and knowledge of the measures to be taken.

Conclusion

Vietnam has made excellent progress in luring foreign direct investment, but in order to increase efficiency, it needs to alter its strategy and orientation. It is the responsibility of local governments to determine if a foreign investment project endangers the human rights of local residents, violates human rights laws, or jeopardizes public safety.

Given its vital significance, the due diligence process can be challenging and buyers often find themselves stuck with numerous difficulties in the way. To help investors make sure the process is smooth and optimized, Viettonkin and its experienced team can offer corporates strong due diligence with well-structured procedure and thorough evaluation. We can support you in enhancing eligibility, achieving portfolio operational excellence, and improving valuation results

The taxation system in Vietnam is characterized by its marked sophistication, which can pose numerous challenges for foreign investors entering the market for the first time. Yet, to overcome the market entry barriers, investors are advised to consult the leading local experts. Thus, the support from trusted local advisors will help them in navigating through and complying with Vietnam tax regulations, focusing on their key business operations.

In general, most business activities in Vietnam are subject to five common types of taxes: Corporate Income Tax (CIT), Personal Income Tax (PIT), Value-Added Tax (VAT), Foreign Contractor Tax (FCT). This article will provide you with a quick note on the important tax regulations for doing business well in Vietnam.

Corporate Income Tax (CIT)

As with most other nations, CIT in Vietnam is a direct tax levied on the profits made by companies or organizations. Regardless of the origin of the organization, whether it is a foreign enterprise with a Vietnam-based subsidiary or whether a permanent establishment, all income earned in Vietnam is subject to CIT.

General information about CIT

In prevalent practice, the tax financial year in Vietnam starts from January 1 and ends on December 31. Yet, enterprises can adopt an alternative tax financial year in certain circumstances. Meanwhile, Vietnam tax law regulates provisional CIT to be calculated and remitted on a quarterly basis, no later than the last day of the following month from quarter end.

The standard CIT rate is 20%. However, a 17% CIT rate shall be applied to corporations with total revenue of less than VND 20 billion. Additionally, there are a few cases of exemption. In particular, oil and gas specialized companies are subject to CIT rates from 32% to 50% depending on the location and specific project conditions. Meanwhile, companies engaging in prospecting, exploration and exploitation of certain mineral resources are under CIT rates of 40% or 50% based on the project’s location.

Foreign enterprises can continuously carry their tax losses forward for a maximum of five (05) consecutive years after the loss-making year. Yet, the carryback of losses is not permitted, and there is no concept of group loss sharing or consolidated tax relief in the Vietnam tax system.

CIT calculation

CIT is calculated under Circular 96/2015/TT-BTC of the Ministry of Finance, following which:

CIT Payable Amount = [Assessable Income - Deduction for establishing a Science and Technology Fund] x CIT Rate

in which,

Assessable Income = Total Revenue - Deductible Expenses + Other Income - Carried Forward Losses - Tax-Exempted Income.

To be deductible, expenses must:

Be related to the generation of revenue

Be incurred in relation to business activities as permitted by the company’s business license

Be supported by appropriate invoices or relevant documents

Be settled by non-cash payment, where expenses are VND 20 million and above, (i.e. bank transfer)

CIT incentives

Vietnam tax incentives in CIT can take various forms, depending on encouraged sectors, locations and project scales, and are granted to new investment projects. For example, for foreign investors venturing in Vietnam, they can enjoy the preferential tax rate of 10% for 15 years with the implementation of investment projects in high-tech zones or in the field of scientific research and technological development, among others.

Value-Added Tax (VAT)

A tax on goods and services known as a value-added type tax (VAT) is one that businesses collect gradually but ultimately bill in full to customers.

Goods and services (including goods and services purchased from foreign sources) used for production, trading and consumption in Vietnam are subject to Value Added Tax (VAT). Regardless of whether they have Vietnamese-based resident establishments or not, organizations and individuals producing and trading VAT taxable goods and services in Vietnam have to pay VAT.

Enterprises declare and remit monthly VAT on the 20th of the following month. Meanwhile, for taxpayers whose turnover did not exceed 500 billion VND in the previous year, they can declare and pay quarterly VAT by the last day of the month following the end of the quarter.

VAT calculations

Currently, Vietnam is applying two VAT calculation methods: Credit method and Direct method. Each business can choose one of these two methods to apply in their accounting system with consistency. However, the first method (the Credit Method) is more commonly used because of its convenience.

Payable VAT amount = Added value of sold goods or services * VAT rate

Where: Added value of sold goods or services = Selling price – Purchasing price of goods or services.

VAT Invoices and E-invoices

Tax law requires VAT invoices to be issued by enterprises in Vietnam for all of their sales transactions. Without receipt of a eligible VAT invoice in either paper or e-invoice), VAT credits will not be available and no CIT deduction will be applicable for taxpayers.

Under the current regulations, from 1st July 2022, 100% of enterprises in Vietnam will be required to apply e-invoicing, thus removing the old paper-based VAT invoicing system permanently. This digital conversion of the tax management method brings about significant benefits as it helps foreign enterprises reduce their administration costs and risks. In addition, the new e-invoicing system can contribute to creating a healthy, transparent, and bureaucracy-free business environment for international companies.

VAT refund

Investors could apply for a VAT refund in case they use the credit method to declare VAT and are manufacturing/ selling the outputs which are subject to VAT. In addition, if the project is currently under the investment phase and has started operating, investors could be eligible for a VAT refund. Furthermore, a VAT refund could be applied on the provision that accumulated creditable input VAT on goods and services purchased for investment purposes is equal to or above VND 300 million.

Personal Income Tax (PIT)

Personal Income Tax or PIT applies to tax residents and non-tax residents; an individual must pay the personal income tax, on all of their annual income, including wages, salaries, dividends, interest, and other types of income. Generally, the foreign investors are deemed as a local tax resident if they resided in Vietnam for no less than 183 days in 12 consecutive months, or have a permanent establishment here.

Tax residents are subject to PIT on their worldwide income on a progressive sliding scale from 5% – 35%, whereas non-tax residents are only charged on their Vietnam-sourced income at a flat rate of 20% on employment income, and different rates on other types of income, depending on the specific regulations.

Taxable employment income items include salary and all types of remuneration and benefits, with the exception of payments for business trips, telephone charges, and stationary costs, office clothes, overtime premiums, among others. On the other hand, taxable non-employment income includes: business income, investment income, gain on sale of shares, gain on sale of real estate, among others.

Non-taxable income includes:

Interest earned on deposits with credit institutions/banks and on life insurance policies;

Compensation paid under life/non-life insurance policies;

Retirement pensions paid under the Social Insurance law (or the foreign equivalent);

Income from transfer of properties between various direct family members;

Inheritances/gifts between various direct family members;

Monthly retirement pensions paid under voluntary insurance schemes;

Income of Vietnamese vessel crew members working for foreign shipping companies or Vietnam international transportation companies; and

Income from winnings at casinos.

The Vietnamese tax year is the calendar year. However, where in the calendar year of first arrival foreign investors are present in Vietnam for less than 183 days, their first tax year is the 12-month period from the date of arrival.

FCT applies to foreign organizations or individuals who run a business or earn income in Vietnam based on a contract or an agreement with a Vietnamese party (as a main foreign contractor), or another foreign contractor to implement a part of the contractual scope of works (a foreign subcontractor).

The components of FCT

FCT comprises both CIT and VAT, but in some cases, may also include PIT.

FCT is levied on services provided or consumed inside Vietnam, and supply of goods accompanied by services, or in which the delivery point is inside Vietnam. Additionally, foreign enterprises bear FCT with construction and installation, interest, royalties, trademarks, penalty/compensation, income from transportation activities, and securities transfer.

Although, due to a few exceptions provided by Vietnamese legislation, not all foreign contractors are subject to the FCT.

FCT declaration

There are 3 methods used in declaring FCT: direct method, declaration method (also known as the deduction method, and the hybrid method)

Direct method

The Vietnamese party declares and pays FCT when the direct approach is applied. The Vietnamese party is in charge of filing the contracts with the appropriate tax authorities, withholding, and paying the necessary FCT to the regional tax authority. The foreign contractor cannot be paid until this is completed.

Declaration method:

Under this method, the foreign contractor is similarly taxed as the Vietnamese contractor or corporation. This suggests that, foreign contractors will be required to disclose and pay CIT at the applicable rate of 20% on their net profit from the project/contract. This is calculated by subtracting the total deductible expenses from total revenue. When adopting the declaration method, the foreign contractor is required to pay VAT on the difference.

By doing so, foreign contractors are required to comply with particular accounting and tax filing regulations as Vietnamese enterprises

Hybrid method:

With the hybrid method, foreign contractors can register and pay for VAT using the deduction technique while still being able to pay CIT based on gross revenue using the direct method. If the foreign contractor is operating in Vietnam under a contract with a term of at least 182 days and keeps accounting records that adhere to the pertinent accounting norms and guidelines set forth by the Ministry of Finance, this method is acceptable.

Using this method, the foreign contractor must register the technique with the local tax office and declare and pay tax directly to the tax authority.

Other taxes

Import-Export tax

If cargo and goods are imported, exported through the Vietnamese border, or in case domestic goods are brought into a non-tariff barrier and goods from non-tariff into the domestic market, investors are subject to the taxation:

On the other hand, investors are exempted from import and export tax if

Goods are transited through Vietnamese border, goods in transit by Vietnamese government regulations,

Aiding goods and grant aid goods,

Goods from non-tariff barrier to other country, goods are imported into non-tariff area and use only in this area, goods are used from non-tariff area to another non-tariff area,

Goods when export are oil and gas relating to natural resources consumption tax.

The rate of the import and export tax varies, depending on whether goods and services are under preferential tariff or not.

Natural Resources Tax (NRT)

With industries exploiting Vietnam’s natural resources, investors are subject to NRT. In case natural water is used for agriculture, forestry, fisheries, salt industries, and sea water is used for cooling purposes, qualified investors may be exempt from NRT.

The tax rates depend on the types of natural resources, ranging from 1% to 40%. Meanwhile, crude oil, natural gas, and coal gas are taxed at progressive tax rates depending on the daily average production output.

Environmental protection tax (EPT)

EPT is an indirect tax which is applied on the production and importation of certain goods with effect on the environment. The calculation of the tax is equal to the absolute amount on the quantity of the goods. From 1st January, 2019, the tax rate is applied from VND 500/kg for restricted use chemicals to VND 50.000/ kg for plastic bags. In 2020, the National Assembly approved a new law on environmental protection, yet no change is specified to the tax rates.

Excise Tax

Excise tax is applied to several luxury goods and non-essential items. Generally, SCT-subjected goods and services are also subject to VAT. SCT is levied on each item only once, and SCT refunds are available for exported goods upon request by the taxpayers in certain cases.

How can foreign investors avoid tax non-compliance in Vietnam?

Unfamiliar and stranged with the business environment in Vietnam, foreign investors will make undesirable mistakes regarding tax regulations. However, the errors can be minimized with the support from top domestic consulting firms as they get Vietnam legal system and market characteristics in the palm of their hand. Viettonkin Audit is such a firm! We are made up from a team of top-notch experts in the industry with decades of experience. Thanks to our deep-insight knowledge and timely information updates, we provide our clients with the best and helpful advice. In this way, our clients can focus on their business and harvest successful results. Let us be your big supporter!

All foreign investors in Vietnam must become familiar with and adhere to the country's unique foreign contractor tax (FCT) taxation system. This article serves as a brief guide for business owners to determine the appropriate FCT for their company and which payment method they should choose.

What is Foreign Contractor Tax?

One of our articles has already covered fundamental knowledge about foreign contractors and FCT in Vietnam (Feel free to take a look at it here). In short, FCT typically comprises a combination of value added tax (VAT) and corporate income tax (CIT) for foreign organizations, or personal income tax (PIT) for the income of foreign individuals.

FCT Payment Methods

A foreign contractor can pay tax in one of three ways: Declaration Method, Direct Method or the “Hybrid” Method.

The Declaration Method applies to a foreign contractor if (i) it has a permanent establishment (“PE”) in Vietnam; (ii) the contract has a term of 183 days or more from the effective date of the contract; and (iii) it adopts the Vietnam Accounting System (“VAS”), files its tax registration application with the tax authorities, and obtains a tax code.

The Direct Method applies to a foreign contractor if it fails to meet any one of the conditions above. A foreign contractor may choose to apply the Hybrid Method if it meets all three of the following conditions: (i) it has a PE in Vietnam; (ii) the contract has a term of at least 183 days from the effective date of the contract; and (iii) it maintains accounting records in accordance with the accounting regulations and guidance of the Ministry of Finance of Vietnam.

Declaration Method

The method of FCT calculation, which uses the Declaration Method and the resulting tax, are virtually the same as the method of calculation and tax paid by a Vietnamese entity registered to do business in Vietnam. The VAT it pays is the same, and the CIT it pays, which is calculated on net profit, is the same.

VAT under the Declaration Method

VAT payable is calculated and deducted under the following formula:

VAT payable = Output VAT – Creditable Input VAT

Output VAT is the total VAT that a foreign contractor collects based on the invoices it issues. More specifically, output VAT is the total VAT imposed on the goods or services that it sells. It is computed by multiplying the taxable price of the goods sold or services rendered by the foreign contractor to a Vietnamese counter-party by the applicable VAT rate. With respect to imported goods, VAT is computed on the import duty price plus import duty plus exercise tax (if applicable), and the environmental protection tax (if applicable).

Creditable Input VAT is the total VAT that a foreign contractor pays based on invoices it receives. Creditable Input VAT equals the taxable price of goods sold or services rendered by a selling party to a foreign contractor multiplied by the applicable VAT rate. For domestic purchases, input VAT is based on VAT invoices. For imported goods, input VAT is based on the VAT payment documents (which are presented to the Customs Office).

VAT rates differ depending on the types of goods sold and the services provided by the foreign contractor. There are three levels of VAT: 0%, 5% and 10%.

CIT under the Declaration Method

CIT is payable in addition to VAT, and it is determined under the following formula:

CIT payable = Assessable Income x CIT rate

Assessable Income = Taxable Income – [Tax Exempt Income + Losses Carried Forward]

Tax Exempt Income is income that is exempt from tax and that is listed as ‘tax exempt income’ in the LCIT. Tax Exempt Income is usually income from business sectors or investment activities that are encouraged, for example, income from cultivation, husbandry, or income from the performance of contracts for scientific research and technological development, or income from investment in favored geographical areas.

Loss Carried Forward is the loss an enterprise suffers after it has completed its tax finalization for any fiscal year. The losses may be carried forward to the next fiscal year and set off against taxable income in that year. Losses cannot be carried forward for more than five years.

Taxable Income means income earned from production or business activities and from other income generated from capital gains, transfer of a right to contribute capital, or transfer of a right to participate in an investment project, transfer of a concession to explore, exploit and process natural resources or real property transfer, etc.

Taxable Income is calculated under the following formula:

Taxable Income = [Turnover – Deductible Expenses] + other income

Turnover is total revenue, excluding value added tax.

Deductible Expenses are actual expenses related to production or business except for 'non-deductible expenses' as defined in the LCIT. To qualify, deductible expenses must conform with LCIT rules, payment must be made via bank transfer (in case of payment in excess of VND20,000,000), and supporting documents are required.

The standard CIT rate is 20%. The rate that applies to encouraged sectors or locations is lower. For example, companies operating in education and training, health, and environmental matters enjoy a CIT rate of only 10%.

Direct Method

In contrast to the Declaration Method, the Direct Method bases its calculation of the FCT on turnover.

When the Direct Method is employed, the law imposes an obligation on the Vietnamese counterparty to withhold the FCT. That is, before making a payment to a foreign contractor, the Vietnamese counterparty must deduct the taxes from the payment, which it then pays to the tax authorities on behalf of the foreign contractor.

VAT under the Direct Method

VAT payable = VAT Assessable Turnover x VAT rate as percentage of tax assessable income

VAT Assessable Turnover is the total turnover without deducting any taxes payable. It includes expenses paid by the Vietnamese counter-party on behalf of the foreign contractor;

VAT Assessable Turnover excludes any payment made by the foreign contractor to a Vietnamese sub-contractor or a foreign contractor who applies the Declaration Method or the Hybrid Method;

Subject to goods and services provided by the foreign contractor, the VAT rate as a percentage of tax assessable income may be 2%, 3% or 5%.

CIT under the Direct Method

CIT payable = CIT Assessable Turnover x CIT rate as a percentage of taxable turnover

CIT Assessable Turnover is the total turnover, excluding VAT, without deducting any payable taxes. The CIT Assessable Turnover includes all expenses paid by the Vietnamese counter-party on behalf of the foreign contractor, but it excludes the payment made by the foreign contractor to a Vietnamese sub-contractor or a foreign contractor that applies the Declaration Method or the Hybrid Method.